Page Contents

A director is a person who leads to a certain area of the company, program, or project companies.

the director usually reports directly to the vice president or corporate officer in the organization. They are appointed by a shareholder to manage the affairs of the company.

board of directors leads and controls a company nan effective board is fundamental to the success of the company.

A company may remove a director if it is not appointed by national company law tribunal bypassing-

For removal of 2nd term of independent director special resolution is passed by the company.

The opportunity of being heard is given to the director before removal by the company.

For removal of executive director and non-executive director ordinary resolution is passed by the company.

The opportunity of being heard is given to the director before removal by the national company law tribunal.

A director is appointed by the national company law tribunal then the company can not remove that director

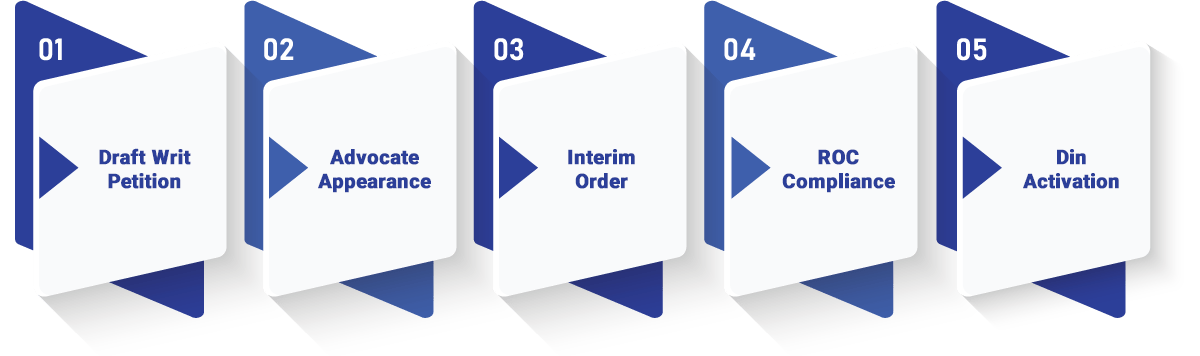

Filling of Appeal with NCLT under section 252 for restoration for struck off companies:

More read:

8. Company shall file FORM DIR -12 with the registrar of the company for cessation of office of director and appointment of director within 30 days of general meeting along with the following attachments-

9. If the national company law tribunal is satisfied by giving application by any members that giving the opportunity of representation by the concerned director is wastage of time or useless then national company law tribunal can withdraw the opportunity of representation from the concerned director.

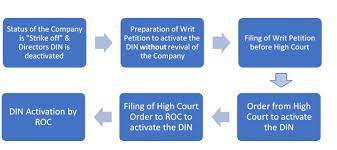

Finally, Activation of Director identification number:

After the regulatory bodies of the National Company Law Tribunal and Hon’ble High Court passes the orders for the revival of struck-off company & DIN re-activation.

the appellant requires the filing of Statutory documents with Registrar of Companies, India for restoration of disqualified Director identification number.

Also, file the ROC Annual Returns of the past 3 Years with the Income-Tax Department.

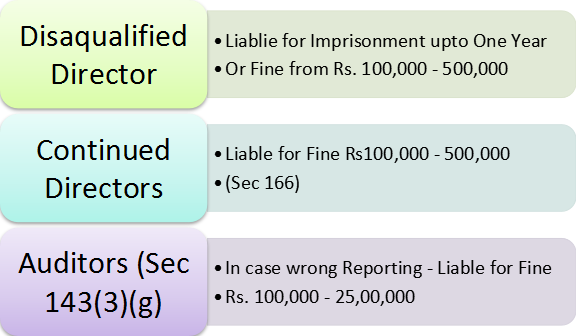

If such Person continues as director even after vacation such person shall be liable for Imprisonment or fine. Disqualified Director can’t continue as Director in Companies.

He shall be considered as ceased with immediate effect.

If a person, functions as a director even when he knows that the office of director held by him has become vacant on account of any of the disqualifications specified in subsection (1), he shall be punishable with imprisonment for a term which may extend to 1 YR or with fine which shall not be less than 1,00,000/- Rupees but which may extend to 5,00,000/- Rupees, or with both.

List of Default of Section in case of Continuation of Disqualified Director

CHECK YOUR DIN STATUS HEREhttps://www.mca.gov.in/mcafoportal/showEnquireDIN.do

Q1- can an independent director who is appointed for the first term can be removed by ordinary resolution?

Ans. Yes, an independent director who is appointed for his first term can be removed by the ordinary resolution. a special resolution is needed where the independent director is removed for his second term.

Q2- can the company remove a director who is appointed by the national company law tribunal?

Ans.- no, the company can not remove that director who is appointed by the national company law tribunal.

Q3- can removing director make his representation on special notice which is given by members of the company for removal of the concerned director?

Ans.-yes, removing director can give his representation on special notice which is given by members of the company for removal of a concerned director.

Q4- which resolution is passed for the removal of the executive director?

Ans.-executive resolution can be removed bypassing

Q5 : Can documents which had earlier been filed with some wrong information be revised under this Scheme?

Answer: Reason being, Scheme clearly specifies that only overdue documents due for filing upto 30.06.2017 should be filed under this Scheme and therefore revision of previously filed annual filing e-forms shall not be taken on record.

Q6. : Disqualification of directors of Companies which have been struck off can be removed?

Answer: In the event of defaulting companies whose names have been removed from the register of companies under section 248 of the Act and which have filed applications for revival under section 252 of the Act up to the date of this scheme, the Director’s DIN shall be re-activated only NCLT order of revival subject to the company having filing of all overdue documents.

Q 7 : Are foreign companies eligible to seek condonation under this Scheme?

Answer: Foreign company has been defined in Section 2(42) as “Foreign Company” means any company or body corporate incorporated outside India which,—

Q8: Implication of Non-Compliance of this scheme?

Answer: The DINs of the Directors associated with the defaulting companies that have not filed their overdue documents and the reform CODS, and these are not taken on record in the MCA21 registry and are still found to be disqualified on the conclusion of the scheme in terms of section 164(2)(a) r/w 167(1)(a) of the Act shall be liable to be deactivated on expiry of the scheme period.

Q9 : what shall be the filing fees for registering under this scheme?

Answer: The filing fee for availing benefits under this Scheme is Rs.30,000/- which is the fee required to be paid at the time of filing the e-Form CODS 2018.

However, before filing e-Form CODS 2018, the defaulting companies shall be required to upload all their overdue documents with an additional fee for the delayed period for each one of them, as may be levied as per section 403 of the Act read with Companies (Registration Offices and fee) Rules, 2014.

Q 10 : Can documents that had earlier been filed with some wrong information be revised under this Scheme?

Answer: The reason being, the Scheme clearly specifies that only overdue documents due for filing up to 30.06.2017 should be filed under this Scheme and therefore revision of previously filed annual filing e-forms shall not be taken on record.

Q11: Can an active company (non-defaulting) apply for CODS 2018 to file its overdue documents?

Answer: As per the introduction given in the Scheme, it is clear that the Scheme has been rolled out for defaulting companies only which are yet to file their annual filing documents which are due to be filed up to 30.06.2017.

Q12: Will this scheme apply to Companies whose status is shown “Strike OFF” on the MCA portal?

Answer: NO, this scheme will not apply to defaulting companies whose names have been removed from the register of companies under section 248 of the Act.

Company Law Committee – Representation:

A Report of Companies Law Committee has been submitted to Govt of India.

Committee has recommended or opined that that for rectifying defect in filing ROC Annual return is required to be restricted to defaulting company only & not with respect to other companies.

So, if any Director was disqualified on account of one of a company defaulting on filing of annual returns, the Director would still be allowed to file the necessary returns in other companies in which ROC compliance has been maintained.

Summary: A lot of directors of Co. approached the Honorable High Court/NCLT to revive their DIN’s & Companies under Article 226 of the under section 252 of Companies Act, 2013 and Constitution of India.

Rajput Jain and Associates, Chartered Accountants offers a various kind of services & integrated completed solutions in the areas of Delhi/ NCR in India corporate regulations, accounting, and taxation, compliance for Start-ups, Corporates & SMEs right from Formation of new companies, secretarial compliance, bookkeeping and accounting, statutory registrations, , audit & assurance, tax consulting & filing, & other associated Experts Services to start, maintain and grow your own business.

In case you need help with filing ROC Annual return for your company or removal of Director Disqualification, contact an Rajput Jain and Associates Experts at singh@carajput.com . 9555 555 480

Calculation while computing GST Interest & Late fee The Goods and Services Tax Interest & Late Fee Calculator helps taxpayers… Read More

Form 16A (Earlier Reflected in Form 26AS) Now Shows Deductor PAN: A Small Change with a Big Impact on TDS Reconciliation… Read More

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}