Where the limit to pass orders for rejecting any refund claim fully or partly falls between 15th April 2021 and 30th May 2021, it’s extended. The extended cut-off date shall be later of two dates:

15 days after reply to note

31st May 2021

Update as on 27th June 2020

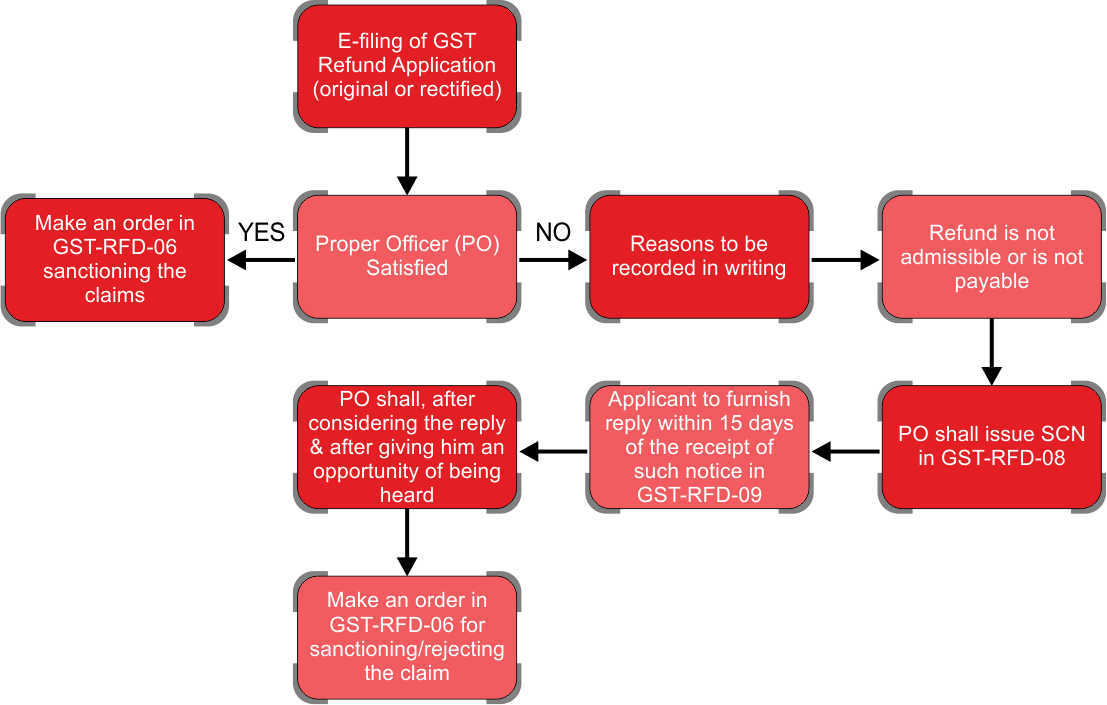

A full or a part of the number applied for refund may are rejected via a notice issued by the authority. Once the following proceedings are done, a final order be passed and issued within 60 days from the date of receipt of application for refund.

In case this point limit is expiring between 20th March to 30th August 2020, the last date to issue order shall be extended to the later of following dates:

15 days from the date of receipt of reply in respect of the notice, from the applicant or

31st August 2020

Update as on 3rd April 2020

The closing date for completion or compliance has been extended to 30th June 2020, where the time limit/time limit/ date of expiry falls between the amount from 20th March 2020 to 29th June 2020. It includes cases where the closing date to use for GST refund in RFD-01 expires between 20th March 2020 and 29th June 2020.

Update as in Sept 2019

Form RFD-01 was implemented with effect from 26th September 2019.

The refund process under GST remains the identical for both normal further as exceptional scenarios.

There is not any ambiguity that for each taxpayer provision associated with refunds are always most favourite under any Act and GST Act is no different. In fact, every organization designs their business process in such a fashion so on make optimum utilization of the refund provisions

With the assistance of this text, we shall provide the readers the reckoner and also the details that ought to be kept in mind while filing refund applications after incorporating all the prescribed Sections, Rules as well as Circulars upto 31 March 2020.

For the sake of easy understanding, we shall be discussing the refund provisions within the following manner:

All the requisite points to be considered at the time of filing of refund applications

Procedure of filing refund application

kinds of refund

IMPORTANT POINTS

Refund can only be filed electronically. Manual Application may beallowed to be filed by the authorities only in exceptional circumstances

The refund could also befiled for a tax period or by clubbing successive tax period, which can spread across different financial years also

again and againthe ITC on inward supplies is spread in multiple months whereas the Zero Rated supplies or inverted duty supplies are worn out few months, in these cases the amount of refund should be selected the most to confirm higher amount of refunds

Refund may beobtained for tax and interest, if any, before the expiry of two years from the relevant date.

Refund shall not be paid to the applicant if the numberis a smaller amount than Rs. 1,000. This amount shall be applied for every tax head separately and not cumulatively

The refund allowed could also beadjusted with any tax or other outstanding from the applicant

If the date of credit of refund within thechecking account of the applicant exceeds 60 days from the date of generation of ARN, then the applicant shall be eligible for interest @6% for the amount of days beyond such 60 days till the particular date of credit of refund within the bank

within the cases where refund of Input decrease is involved, i.e. type (a), (c) and (e) given below

Refunds will befiled chronologically, i.e. where the refund is submitted for any tax period, any subsequent refund application in respect of the previous period shall be disallowed.

Refund amount shall relate to the amount of ITC allowed, as appearing in Form GSTR-2A of the applicant.

Transitional Credit can’t betreated as a part of Net ITC and hence no refund allowed

within therefund of tax falling under type (i) to (l) given below, the refund shall be allowed to the applicant within the same proportion within which original payment was made, i.e. where the tax to be refunded has been paid by Credit yet as Cash ledger, the refund to be paid in credit ledger and cash (i.e. Bank Account) shall be within the same proportion during which they were debited during the relevant period

the wholerefund is processed for all heads of tax, i.e. IGST, CGST, SGST and cess by the identical jurisdictional officer to whom the refund application is forwarded by the portal

within thecase of refund on account of export of products with payment of tax, the shipping bill filed by an exporter is deemed to be an application for refund together with details filled in GSTR-1 and GSTR-3B, hence the identical isn’t discussed below

FORM RFD-01

There is lots of mistakes when filling in GST challan for creating GST payment. you will also find yourself paying excess GST thanks to this. This excess amount is shown as a balance within the Electronic Cash Ledger.

The balance in Electronic Cash Ledger are often claimed as a refund by submitting a refund form RFD-01. this could be done online on the GST Portal/GSTN the surplus GST paid is claimed as a refund within two years from the date of payment. this implies that if excess GST is paid within the month of November 2017, GST refund application may be submitted until November 2019.

DOCUMENTS TO BE SUBMITTED FOR GST REFUND

The GST RFD 01 shall be in the course of the subsequent documentary evidences, as applicable, in Annexure 1:-

The reference number of the order and a duplicate of the order gone the right officer or an appellate authority or appellate tribunal or court leading to such refund or reference number of the payment of the quantity claimed as refund, or

A statement containing the amount and date of shipping bill or bills of export and also the number and therefore the date of relevant export invoices, in a very case where the refund is on account of export of products, or

A statement containing the quantity and date of invoices and also the relevant bank realisation certificates or foreign inward remittance certificates, because such a case is also seen, where the refund relates to export of services, or

A statement containing the quantity and date of invoices together with the evidence regarding the endorsement within the case of supply of products made to a SEZ unit or a SEZ developer.

A statement containing the quantity and date of invoices, the evidence regarding the endorsement specified and also the details of payment, together with the proofs thereof, during a case where the refund relates to the supply of services made to a SEZ unit or developer.

A declaration to the effect that the SEZ unit or the SEZ developer has not availed the input reduction of the tax paid by the supplier of products or services or both, in a very case where the refund is on account of supply of products or services made to a SEZ or a SEZ developer.

A statement containing the amount and date of invoices together with such other evidence as is also notified during this behalf, during a case where the refund is on account of deemed exports, or

A statement containing the quantity and also the date of the invoices received and issued during a tax period in an exceedingly case where the claim pertains to refund of any unutilised input reduction where the credit has accumulated on account of the speed of tax on the inputs being on top of the speed of tax on output supplies, apart from nil rated or fully exempt supplies, or

The reference number of the ultimate assessment order and a replica of the said order during a case where the refund arises on account of finalisation of provisional assessment, or

A statement showing the main points of transaction considered as intra-state supply but which is subsequently considered as inter-state supply, or

A statement showing the main points of the number of claim on account of excess payment of tax

CERTIFICATE FROM CHARTERED ACCOUNTANT

In case the GST Refund claimed exceeds Rs. 2 Lakhs – A certificate in Annexure 2 of Form GST RFD 01 issued by a comptroller or a price accountant to the effect that the incidence of tax, interest or the other amount claimed as refund has not been passed on to the other person, in a very case where the quantity of refund exceeds Rs. 2 Lakhs shall even be submitted. For the aim of this rule, where the quantity of tax has been recovered from the recipient, it shall be deemed that the incidence of tax has been passed on to the last word consumer.

In case the GST Refund claimed doesn’t exceed Rs. 2 Lakhs – a declaration to the effect that the incidence of tax, interest or the other amount claimed as refund has not been passed on to the other person shall even be furnished.

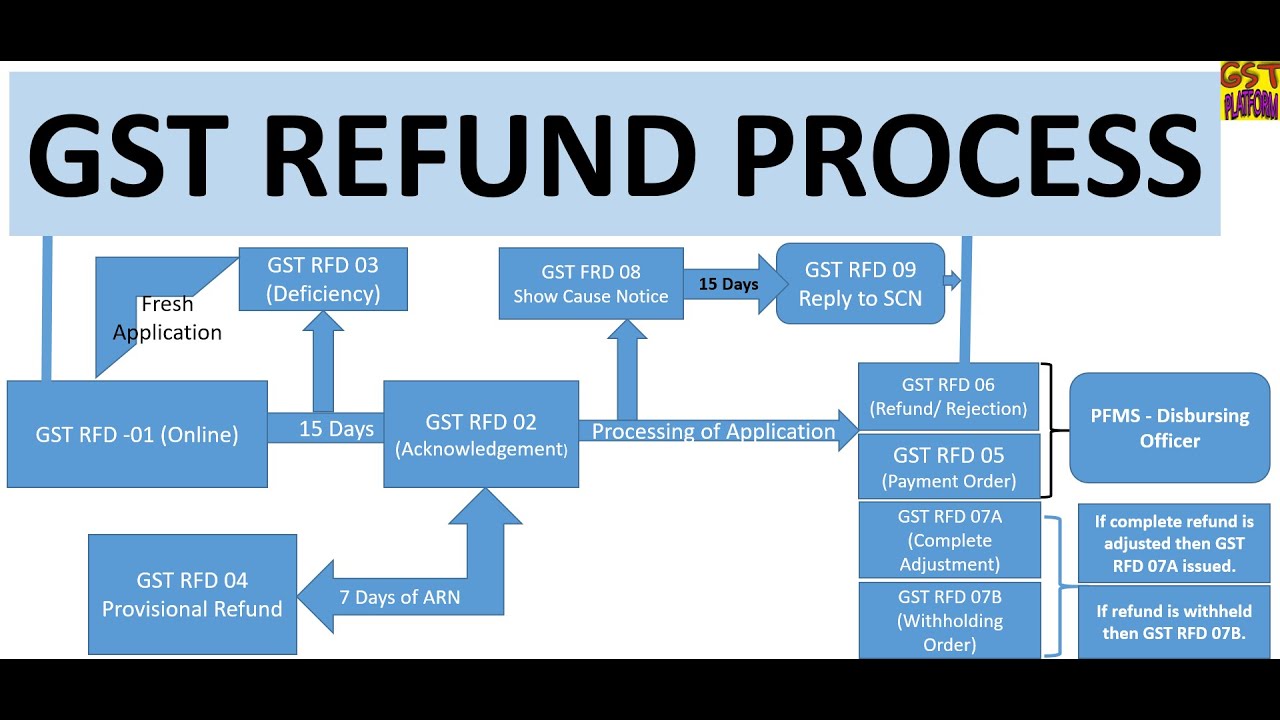

GST REFUND PROCESS

GST REFUND

A person claiming refund of tax or interest or the other amount paid must file an application for refund in Form GST RFD-1 before the expiry of two years from the ‘relevant date’. The relevant date in respect of different supplies is as follows –

Goods exported by sea or air – Date on which the ship or aircraft during whichthe products are loaded, leaves India

Goods exported by land – Date on which the productspass the frontier

Goods exported by post – Date of dispatch of productsby the concerned post office

Services exported, where the availabilityof service has been completed before the receipt of payment – Date of receipt of payment

Services exported, where the payment has been received prior to, beforethe date of issue of invoice – Date of issue of invoice

Unutilized input diminution– End of the twelvemonth within which the claim for tax refund arises

DOCUMENTS REQUIRED FOR THE REFUND

If the number claimed as tax refund is a smaller amount than INR 5 Lakhs – The person has to file a declaration, supported the documents or other evidence available with him, certifying that the incidence of tax or interest being claimed as refund has not been passed on to a different

If the quantity claimed as a refund is less than INR 5 Lakhs – the application shall be supported with the following documents –

Documentary evidence to determinethat the refund is because of the person.

Documentary or other evidence to ascertainthat the number was paid by him/her which the incidence of the tax or interest has not been passed on to a different

ONLINE FORM GST RFD-01

The application for refund shall be supported by various documents depending upon the category of refund. the net portal provides facility to upload 10 files of 5MB each. the application is transferred to the jurisdiction officer for the aim of further processing

DEFICIENCY MEMO FORM GST RFD-03

If any deficiency is noticed within the application submitted by the taxpayer, the jurisdictional officer shall issue deficiency memo in Form RFD-03 within 15 days of submission of application, requiring the taxpayer to provide for a fresh refund application after undertaking the required rectification. Any amount of Input diminution / Cash debited from Ledgers shall be re-credited automatically within the ledgers of the taxpayer. Important point to be noted is that the applying filed after Deficiency memo is treated as a fresh application and also the limitation period of two years shall also apply to the new application.

ACKNOWLEDGEMENT FORM GST RFD-02

If the refund application is complete all told aspects, acknowledgement in Form RFD-02 shall be issued within 15 days of submission of application. Once an acknowledgement has been issued no deficiency memo on whatsoever grounds is issued by the officer.

PROVISIONAL / REFUND GST ORDER

The officer upon being satisfied that clearthe refund is due towards the applicant may sanction 90% of the refund amount on a provisional basis within seven days of the refund application in Form RFD-04 within the case of any claim for refund on account of zero-rated supplies

However, the officer may upon being fully satisfied about the eligibility of the refund and is of opinion that no further scrutiny is required, directly issue refund formRFD-06, that is most commonly seen in almost all the cases.

Along with issue of the above forms, payment formRFD-05 shall be issued for the number sanctioned and therefore the same shall be electronically credited to the applicants checking account.

Form RFD-07 is prescribed in Rules for adjustment of refund with any outstanding demand from the applicant, but this is oftenalso now incorporated in Form RFD-06

If officer is of the view that certain refund amount is non-admissible, then notice is Form RFD-08 shall be issued asking reasons why the refund mustn’tbe rejected, and the applicant shall submit a reply against such notice in Form RFD-09.

TYPES OF GST REFUND

Refund of unutilized input decrease(ITC) on account of exports without payment of tax

A. The amount of refund shall be the smallest amount of:

Zero Rated Turnover/Adjusted Total Turnover * Net of ITC

Balance standing in the Electronic Credit Ledger at the time of refund filing.

Balance in Electronic Credit Ledger at the topof period that refund is filed

B. The relevant date within thecase of products shall be:

Where it is exported by sea or air, the date on which the ship or aircraft leaves India

Where it is exported by land, the date on which such goods passes frontier

Where it is exported through Post, the date on which the despatch of productsby Post Office

C. The relevant date within thecase of services shall be the date of:

Receipt of convertible exchange or Indian rupees wherever permitted by the RBI, where services are completed before receipt of payment

Issue of invoice, where payment had been received before issue of invoice

D. In case of export of products, the shipping bill details as uploaded within there fund application in statement 3 shall be checked by the officer with ICEGATE. within the case of services BRC/ FIRC details shall be uploaded as an indication of receipt of payment

E. ITC paid on Capital Goods shall not be included in Net ITC for the aimof computing refund

F. Receipt of convertible exchange, or Indian rupees wherever permitted by RBI could be a precondition just in case …..of refund against export of services only and not within the case of products

G. The refund can not be denied whether or not LUT has not been furnished by the applicant on a timely basis and such delay are often condoned by the officer. Also if the applicant fails to export the products within a period of three months from the date of invoice, the jurisdictional commissioner may consider granting extension of your time limit for export

H. If there’s difference within the value of invoice and shipping bill, then lower of the 2 should be considered for the aim of refund

I. A taxpayer who has received goods at GST 0.05% and 0.10% under Notification 40/2017 and 41/2017 – Central rateand Integrated charge per unit respectively can export the products only against LUT then file refund under this category

2. Refund of tax paid in respect of export of services

Unlike the case of export of productswith tax (refer last paragraph of points to be considered for goods), refund within the case of export of services with payment of tax has to be filed separately

The details of the invoices and corresponding BRC/ FIRC shall be uploaded in statement 2

The relevant date remains the identicalas mentioned in above point

3. Refund in respect of unutilized ITC in relation to supplies made to SEZ Unit/SEZ Developer without payment of tax

A. The amount of refund shall be the smallest amount of:

Zero Rated Turnover/Adjusted Total Turnover * Net of ITC

Balance standing in the Electronic Credit Ledger at the time of refund filing.

Balance standing in the Electronic Credit Ledger at the topof period that refund is filed

B. The refund shall be filed once the availabilityis admitted fully in SEZ for authorised operations as endorsed by the desired officer of the zone

C. The details of supply to SEZ shall be uploaded in statement 5

4. Refund of tax paid in respect of supplies made to SEZ Unit/SEZ Developer with payment of tax

A. The refund shall be filed once the provisionis admitted fully in SEZ for authorised operations as endorsed by the required officer of the zone

B. The details of supply to SEZ shall be uploaded in statement 4

5. Refund of unutilized ITC on account of accumulation thanks toinverted tax structure

A. The amount of refund shall be the smallest amountof:

tax payable on such inverted rated supply

Balance standing in the Electronic Credit Ledger at the time of refund filing

Balance standing in the Electronic Credit Ledger at the topof period that refund is filed

B. The supplier supplying goods to exporter at GST 0.05% and 0.10% as detailed above shall even beeligible to file refund during this category

C. ITC paid on Capital Goods and Input Services shall not be included in Net ITC for the aimof computing refund

E. If rate of tax has been reduced from upper rate to lower rate on any goods, the identicalshall not be eligible for refund during this case

F. The relevant date is that theday of the month of furnishing of the return under Section 39 for the amount during which such claim for refund arises

G. The details of inward and outward supplies together withcorresponding tax values shall be uploaded in statement 1A

6. Refund to supplier of tax paid in respect of deemed export supplies

A. For the aimof filing refund, duly signed copy of invoice by the recipient EOU or acknowledgement by jurisdictional tax officer about receipt of said deemed export supplies by the authorisation holder shall be needed

B. An undertaking that the recipient shall not claim ITC nor refund of tax charged in respect of such supplies

C. The details of outward supplies shall be uploaded in statement 5B

D. The relevant date is that thedate on which the return regarding such deemed exports is furnished.

7. Refund to recipient of tax paid in respect of the deemed export supplies

A. The amount of refund shall be the smallest amountof:

Net Input ITC of Deemed Exports

Balance standing in the Electronic Credit Ledger at the time of refund filing

Balance standing in the Electronic Credit Ledger at the topof period that refund is filed

B. A declaration that supplier has not availed refund with relation tosaid supplies

C. The details of inward supplies shall be uploaded in statement 5B

8. Refund of excess balance as available in the Electronic Cash Ledger

Balance lying in Electronic Cash ledger, which mightair account of excess challan payment or thanks to excess TDS deduction is claimed as refund under this category

9. Refund of excess payment of tax

Supporting documents to determine excessive payment of tax shall be uploaded with the refund application

10. Refund of tax paid on intra-State supply which is subsequently held to be inter-State supply and the other way around

The details of supplies wherein the Place of Supply has changed shall be uploaded within there fund application in statement 6 stating the initial Place of Supply considered together with tax paid and therefore the re-assessed Place of Supply with taxes

11. Refund in respect of assessment/provisional assessment/appeal/any other order

Reference number and replica of the assessment / appeal / any order together with proof of payment of pre-deposit that refund is being claimed shall be uploaded

Refund based on of any other ground or reason

Any other refund case which isn’t included in any of the cases may be claimed during this category mentioning the specification and amount of refund at the portal

ORDER FOR GST REFUND CLAIMS

If the refund is on account of the export of products and/or services, the authorised officer will refund 90% of the full amount claimed as a refund on a provisional basis in Form GST RFD-4. Thereafter, after due verification of the documents furnished, the officer will issue an order for the ultimate settlement of the refund claim.

Provisional refund are granted subject to the subsequent conditions:

The person claiming a refund has not been prosecuted for nonpaymentof an amount exceeding Rs. 250 Lakhs during the preceding 5 years.

The person’s GST compliance rating isn’tbut 5 on a scale of 10.

No pending appeal, review or revision exists on the numberof refund.

If the officer is satisfied that the full or a part of the quantity claimed as a refund within the application is refundable, he will issue an order for the refund in Form GST RFD-5. this can be done within 60 days from the date of receipt of the application. If the refund isn’t sanctioned within 60 days, interest on the refund amount are going to be got the amount after 60 days, till the date of actual refund of tax.

Note: No refund shall be made if the quantity claimed as refund is a smaller amount than Rs. 1,000.

EXCEPTIONAL SCENARIOS OF GST REFUND CLAIMS

Some of the exceptional GST refund rules are as follows –

Tax on supply of productsthought to be deemed exports. E.g.: Supply of products or services to an SEZ (Special Economic Zone) or EOU (Export Oriented Unit).

Tax refunded based on a judgement, decree, order or on the direction of an Appellate Authority, Appellate Tribunal or any court.

Tax paid in respect of a supply, not been provided, either wholly or partially, and thatan invoice has not been issued.

Tax wrongly collected and deposited with the Central or regime. If someonehas paid CGST and SGST on an interstate supply or IGST on an intrastate supply, the person is eligible for a refund of the quantity once the tax has been remitted correctly.

IGST paid on the provisionof products to tourists travelling out of India, if the products are taken out of India.

The relevant date under different scenarios is as follows –

Goods thought to bedeemed exports – Date on which the return referring to the deemed exports is filed

Tax refundable as a consequence of a judgement, decree, order or on the direction of an Appellate Authority, Appellate Tribunal or any court – Date of communication of the judgement, decree, order or direction

Tax provisionally paid – Date of adjustment of tax after the ultimate assessment

In the case of an individual, aside from the supplier -Date of receipt of products or services by the person

Any other case – Date of payment of tax If you always think of blessings, you attract more blessings. If you always think of problems, you attract more problems.

FOR FURTHER QUERIES CONTACT US: W: www.carajput.com E: singh@carajput.com T: 9-555-555-480

Rajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}