Page Contents

Indian dynamism, entrepreneurship, and enthusiasm is seeking new horizons across the world. Of course, anyone entering a far-off land must be sure of the laws, rules, and regulations of the host country.

Each country is different and keeping up with the laws of various countries can indeed be a challenge.

In India, the Reserve Bank of India is responsible for controlling and regulating investment in foreign entities by persons who are residents of India. someone could also be a citizen of India and a resident outside India.

A citizen who isn’t a resident of India won’t be governed by banking concerns of India regulations. An Indian resident is absolved to invest in foreign assets out of the income received when he/she was resident outside India.

So, if someone resident in India desires to enter into the overseas market, he can enter either by establishing a branch office or liaison office outside India or he can form an independent Company outside India.

The corporate formed outside India could also be within the variety of wholly-owned subsidiaries or venture companies.

It is important to notice that under section 2 of the FEMA Act, the intention to remain outside or inside India for an uncertain period is vital. this is often different from the provisions under section 6 of tax Act.

To be a resident under the revenue enhancement Act, a person needs to only stay in India for a specified number of days. So, a private is also a non-resident under the revenue enhancement Act during a year and should be resident as per the FEMA Act, during the identical year.

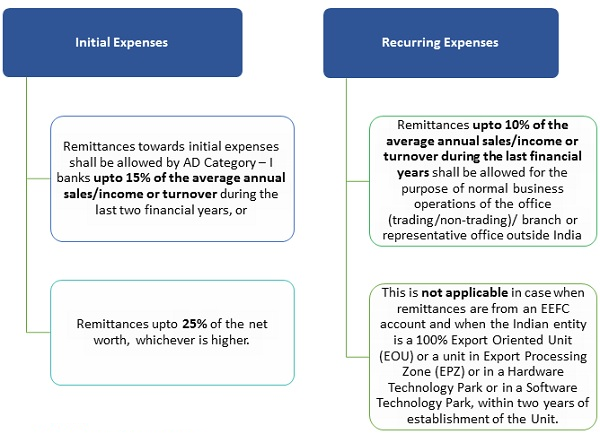

A person resident in India being a Firm or Company or Body Corporate registered in India is eligible to determine a branch outside India. General permission is out there for the opening of a checking account for the aim of meeting the Branch Expenses abroad subject to the following limits/conditions:

Branch/office/representative can acquire office equipment and other assets required for running their normal business operations. Funds required for this could be remitted by the Indian entity from India as an accounting transaction.

However, transfer or acquisition of immovable property outside India, apart from by way of lease not exceeding five years, by the overseas branch/ office/ representative are going to be subject to RBI regulations.

Notably, the above facility cannot be utilized by e-commerce companies who are, for instance, within the business of providing an e-commerce platform to foreign sellers and buyers and want to determine a group account during a foreign country without establishing a branch office or representative in this country.

The Indian firm/companies should submit applications to their bankers (authorized dealers) in form OBR together with the particulars of their turnover duly certified by their auditors and also a declaration to the effect that they need not approach/would not approach the other authorized dealer for the power being applied for.

The appliance form OBR must be filled in with necessary details together with supporting documents. After which the exchange is released by the authorized dealer (bank).

A recurring (expenditure) remittance facilities are allowed initially for a period of two years only, after obtaining confirmation from the applicant that they need to complete all legal and other formalities in India and abroad in reference to the opening of trading/non-trading office or for posting a representative abroad.

The overseas office/branch of software exporter company/firm may repatriate to India 100 percent of the contract value of every ‘off-site’ contract.

In the case of companies usurping ‘on site’ contracts, they ought to repatriate the profits of such ‘on site’ contracts after the completion of the said contracts.

An audited yearly statement showing receipts under ‘off-site’ and ‘on-site’ contracts undertaken by the overseas office, expenses, and repatriation thereon could also be sent to the AD Category – I banks.

Wholly Owned Subsidiaries make it possible for the parent company to manage and diversify. Generally, it is seen that the Wholly Owned Subsidiaries retains legal control over operations, products, and processes. a number of the samples of WOS include Reliance Industrial Investments and Holdings Limited owned by Reliance Group of Companies, Concorde Motors India Ltd, owned by TATA Motors.

There are few requirements for a foreign corporation to open its branch in India. A subsidiary should be established for different reasons and the establishment of a head office in India’s requirements and needs.

For the following reasons, international firms, including US corporations, are allowed to set up branch offices in India:

A Branch office is not allowed to conduct production operations of its own but is authorized to subcontract them to an Indian company. Branch offices founded with RBI approval may remit branch income outside India, net of relevant Indian taxes, and subject to RBI guidelines subjected to the condition of RBI grants permission to set up branch offices.

A branch office is ideal for international firms looking to set up a temporary office in India and not involved or intending to make long-term plans for Indian operations; except for the above-listed finance, shipping and airlines, etc.

Presently, the application for the branch office and BRANCH office is sent through the AD according to the Reserve Bank of India’s conditions. The approved dealer implies obtaining banking licenses for a different entity.

To start a branch office in India the following filings are required:

The RBI accepts the application for BRANCH office licenses but the Approved Dealers (AD) route the applications for the BRANCH office as per the recent changes. Despite that, the timeframe for creating the BRANCH office has significantly expanded. Even the paperwork needed for the same has significantly increased.

Know about- Foreign Company Open a Branch Office in India

That RBI-licensed branch office shall be licensed with the Ministry of Corporate Affairs, it is a branch office registration as a foreign business establishment in India. On such registration, the business registrar allocates a CIN i.e. Corporate Identification Code. The following forms must be filled out with the Companies Registrar:

The below few more criteria for a branch office are also required after Incorporation:

Regarding company management standards in India see also Annual Corporate Filings in India.

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}