Page Contents

Section 2 (40) of the companies Act 2013 states that the financial statement includes the subsequent items:

As per the provisions of Section 134 of Companies Act, 2013 financial statement would be signed by the following:

Note: Chairperson of the corporate can sign the financial statements after authorized by the Board of directors regardless of whether he chaired the meeting or not.

The signed financial statement submitted to the auditor then the auditor shall prepare an Auditors’ report and also the same shall be attached to the financial statement.

Financial Statement must be adopted by the firm at the Annual General Meeting. The company’s Annual General Meeting may well be convened within six months of the financial year’s end, on September 30th.

The financial statement, including any consolidated financial statements, shall be circulated after signing, along with a duplicate of each of—

• the auditor’s report; and

• any notes or annexure

• the Board’s report

• CSR Policy & initiatives

• Address of Website of the corporate.

• Statement of the Company’s affairs.

• Details in respect of the Contracts or arrangements which have been entered into with the Related party, and the same be provided in Form No. AOC-2.

• Director’s Responsibility statement.

• Details in respect of activity undertaken for the conservation or renewal of energy, technology and information on the foreign exchange.

• Policy on Remuneration & Director’s Appointment.

• Any sought of adverse remarks, being received from the Secretarial Auditor in the Report or by the internal auditor, along with their respective comment with regard to the remarks which have been made by the Board of Directors of the entity.

• Details of fraud Reported by auditor.

• Statement of Annual Evaluation

• Declaration by Independent Directors.

• No of Board Meetings.

• Details of guarantees, loans or Investments.

•Amount carrying reserves or paid by Dividend.

• CSR Policy and initiatives.

The financial statement of the corporate is required to sign by two directors out of which one shall be managing director or by one director if the corporate has just one director.

Financial statement of One Person Company shall be signed by only one director.

The financial statement of the businesses can also be signed electronically with the Digital Signature of the directors, Chief Executive Officer/ Company Secretary/ Chief financial officer and also the Statutory Auditors of the corporate.

The date of signing of financial Statement including balance sheet, Profit & Loss, cash flow Statement and other supporting Documents shall be the date which may either be before the date of signing of Audit report or can be the actual date of signing of audit report by the auditor.

As per the provisions of Section 134(1) financial statement of the corporate shall be approved by the board of Directors in its meeting and signed on behalf of the board.

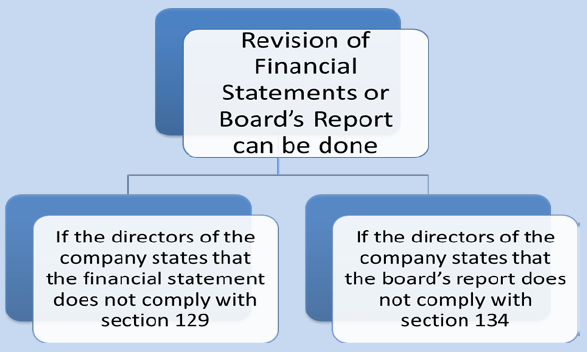

Company is only allowed to file a revised Financial Statement once every FY. After receiving an order from the Tribunal, the Company can file a revised Financial Statement with ROC, together with a copy of the ruling, provided that the Company can update the financial statements for any of the previous 3 Financial Years.

There is two kind of Financial Statement Can be revised like Compulsory Revision & Voluntary Revision

| Basis of Difference | Voluntary revision of Financial Statement | Compulsory revision of Financial Statement

|

| Application Grounds | Company can apply if the Financial Statement are not made or prepared as per the law. | An application under this section can only be made if accounts are found to be fraudulent, misleading, or incorrect. |

| Provision Governing | It is governed under the provision of U/s 131 of companies act | It is regulated u/s 130 of companies act |

| Filing of Petition | The Company through its representative such as practicing professionals can apply to the Tribunal for the revision of its statement. | The central government, Income tax authority, SEBI, and such authorities can apply for revising the Financial Statements. |

| Permissible revision | Books cannot be revised for more than 3 preceding FY. | Books of Director can be revised of up to 8 previous FY . |

Conclusion

Popular Articles :

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}