Liquidation is basically a process, being initiated by a corporation, in order to shut their operations. The corporate entity may plan to wind up because of various reasons like unwillingness to continue with the operations, insolvency and so on. As the term suggests, liquidation of a corporation refers to liquidating the assets of the corporate entity. By initiating the liquidation process, the corporate entity may sell its assets to satisfy obligations and repay liabilities.

Where an organization is liquidated due the reason of bankruptcy, the liquidator is required to sell their assets, in order to repay all pending liabilities. In case, any amount remains, after repayment to the creditors, the same gets distributed among the shareholders of the corporate entity.

WINDING UP

Winding-up involves complete shutdown of all business operations, transactions and thereby involves selling off of the company’s assets to other individuals or entities, in order to satisfy company’s debt.

Once the debts are cleared off, the remaining assets of the corporate entity will be shared among shareholders concerning the capital invested by them

TYPES OF WINDING UP

The winding-up of the corporate entity can be executed in two different ways

Compulsory Winding Up: Compulsory winding up of an organization takes place through an order of a tribunal or a court, or by passing of special resolution by the directors, which proposes a court intervention. Similarly, it can execute by filing a petition with a court or a tribunal, and the same be made by the official person of the corporate entity. In case the corporate entity has indulged in any fraudulent/unlawful activities, it is often winded up

Voluntarily Winding Up: The company requires a resolution from the directors, to dump all assets of the corporate entity or to transfer the stakes to a different entity.

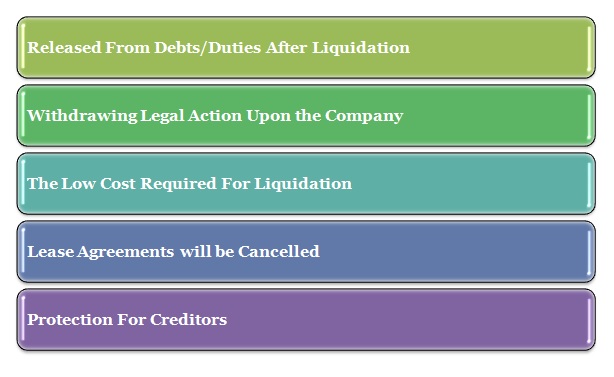

ADVANTAGES OF WINDING UP

ADVANTAGES OF WINDING UP

Free from debts after liquidation: Once the liquidation process is over, the directors and all the company officials are free from all creditor liabilities and pressure.

Avoiding legal action against the company: If the resolution is passed voluntarily by directors, they’re going to neglect legal proceeding taken by the court or the tribunal, and provide a platform to company directors to target other business opportunities.

Comparingly low cost charged for liquidation: the cost or expenses involved within the liquidation process is comparatively low, as charges are applicable on the sale of assets.

All lease agreements are cancelled: If any company or entity has entered into a lease for a prescribed time, during the liquidation process, it’ll terminate all the terms and conditions of the lease. If any penalty must be paid, it’ll be deducted from the sale of assets.

Advantages for creditors: After a prolonged struggle, creditors will be benefited from the liquidation process as they’ll be eligible for a default payment, with relation to the proposition of credits given by all creditors.

CHECKLIST RULES FOR WINDING UP

Board meetings should be convened for the approval of winding up an organization.

A notice should be produced in written form, in order to convene a general meeting, for passing of a resolution on the winding up procedure.

Once order is passed, an official liquidator or insolvency professional be appointed.

The income tax department should be acknowledged with reference to the resolution passed at the meeting for voluntary winding up of the corporate entity.

Simultaneously, a No Objection Certificate (NOC) be obtained from the Income Tax Department.

If the creditors are in majority, then the creditors meeting should be conducted to approve the resolution passed within the general meeting; provided that creditors are owed 2/3rd of the corporate entity debts.

Before the initiation of the winding-up process, an intimation be provided to the Insolvency and Bankruptcy Board of India (IBBI), and the same be made within 7 days from the date of passing of resolution.

Also, an announcement be made to the general public, within 14 days from the date of passing of the resolution, and the said announcement be made in official gazette, one English newspaper, and one local newspaper, where the registered company is located.

The whole process of winding up is required to be completed within 12 months from the initiation of liquidation.

WINDING UP OF PRIVATE LIMITED COMPANY

Winding up of a private company can be done in 2 alternative ways. These are

Selling company shares: By selling the majority of the company shares to a different person or entity, the shareholders will avoid the burden of debts. Hence, voting powers, rights, and responsibilities are going to be laid on the acquired person or the entity.

Voluntary wind up: Voluntary wind up may be commenced either by special resolution or a resolution taken during a general body meeting. By violating any of the terms and conditions of the memorandum of association (MOA), the winding will be executed. Similarly, because of insufficient financial funds or inability to clear the debts, an organization are often winded up.

VOLUNTARY WINDING UP OF COMPANY

Members’ Voluntary winding up

Where a corporation is termed as solvent, i.e., they are able to pay their debts, at the time of closure and its directors make a voluntary declaration for the same, it is known as the Members’ Voluntary winding up. Such declaration should bear the following characteristics –

It must be produced and presented on an affidavit.

It must be made within 5 weeks preceding the date of the resolution gone the corporate entity to wind up. The same be submitted to the registrar within the prescribed due date.

A copy of the latest and audited profit & loss statement of the corporate entity (as on a practicable date before the declaration of solvency) should accompany the declaration.

The latest Balance Sheet and Statement of Assets & Liabilities of the company, shall be enclosed with the declaration.

PROCESS OF MEMBERS’ VOLUNTARY WINDING UP OF COMPANY

Solvency declaration, made by the directors.

The statutory declaration to the Registrar

Appointment of liquidator

Collection of the assets belonging to the corporate entity, payment of its liabilities and distribution of the balance of the proceeds among the contributors.

Creditors’ Voluntary winding up

If the solvency declaration isn’t made by the directors and submitted to the registrar, the corporate entity is presumed to be insolvent. In such a case, the creditors must meet (usually after the corporate entity general meeting) to pass the resolution for winding up and liquidation of the corporate entity.

PROCESS OF CREDITORS’ VOLUNTARY WINDING UP OF COMPANY

The general meeting of the corporate entity passes a resolution to wind up the corporate entity operations

A meeting of the creditors must happen

The members and creditors are required to appoint a liquidator or a group of liquidators.

They must incorporate a committee of inspection as well

The process of winding shall be initiated, in accordance with the provisions of law.

STEP-BY-STEP PROCEDURE FOR VOLUNTARY WINDING UP OF COMPANY

With reference to the companies’ act, 1961, the resolution of the committee meeting is crucial to start out the completing process.

In a special resolution, a majority of 3/4th of the corporate entity shareholders should register their vote on the side of winding up the corporate entity.

Similarly, the company’s creditors are required to approve the resolution made for winding up, and that too without any complications.

A “Declaration of Solvency” along with the details of outstanding debts, be enclosed together with the auditor report, regarding total assets of the corporate entity and it should be forwarded to the RoC (Registrar of Companies).

Now the official liquidator is appointed to perform the winding up process from the date of passing the resolution.

After the resolution has been passed, the liquidator should open a bank account within a period of 1 month.

The liquidator is required to open a bank account in any of the scheduled bank, and the same shall be in the name with, the prefix “the name of the company” followed by “voluntary liquidation”.

The liquidator will collect all the reliable documents and prepare a report consisting of final accounts and present this in a very general meeting for approval. Here, the bulk of members should pass this resolution.

After compiling all the mandatory documents, the ultimate report is sent to the tribunal for reference.

After examining the credibility of the report, the tribunal will pass a decree for the dissolution of the corporate entity.

A copy of that decree is forwarded to RoC by the liquidator within 30 days of the order dated.

Now the RoC will mandate the finishing up of the corporate entity and take away the name of that company from the registry.

Simultaneously, the RoC will publish this order within the official gazette of India.

COMPULSORY WINDING UP OF COMPANY

Where any company, registered in India, is compulsorily winded up by the order of the tribunal or court, the same is expected to have indulged in any fraudulent/ unlawful activities. In such a case, the petition may be filed by

The company itself

The Registrar of companies (RoC)

The creditors of the corporate entity

The central/state governments

The contributors

PROCEDURE FOR COMPULSORY WINDING UP OF COMPANY

The petition to the tribunal should be filed together with the statement of affairs, of the disputed company. Once the scrutinization of the credibility of the petition filed is done, the tribunal may accept or reject the aforesaid petition.

Here, the liquidator is appointed by the tribunal itself.

The liquidator will execute all assets of the corporate entity, examine the book of accounts, and compile into a draft/report.

These reports are to be forwarded to the tribunal after the carrying out committee had accepted the same.

Rajput Jain and Associates ’s Procedure for winding up a private limited company

Declaration To ROC

The statement of accounts must be submitted within a month before the submission of the applying to wind up the corporate entity. This is often a declaration to the Registrar of Companies that the contents of the application are only to be considered, providing that the corporate entity has no other assets or liabilities.

Submit Documents

Within a month of submitting the statement of accounts, the applying must be submitted together with the documents mentioned above. Our representatives will guide you through the complete procedure.

Final Closure

It takes a minimum of two to 3 months to complete the closure of your company, but it could take much longer, as per the findings of the liquidator appointed.

DOCUMENTATION FOR THE CLOSURE OF THE COMPANY

The documents required for the closure of the corporate entity are;

PAN card of the corporate entity

Certificate of closure of the company’s bank account.

An indemnity bond be made, and the same be notarized by the directors.

Latest statement of company accounts.

Statement of accounts associated with all assets and liabilities of the corporate entity, audited by chartered accountant (CA).

A copy of the resolution passed by the board members.

Application for removing the name of the corporate entity.

Rajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}