Page Contents

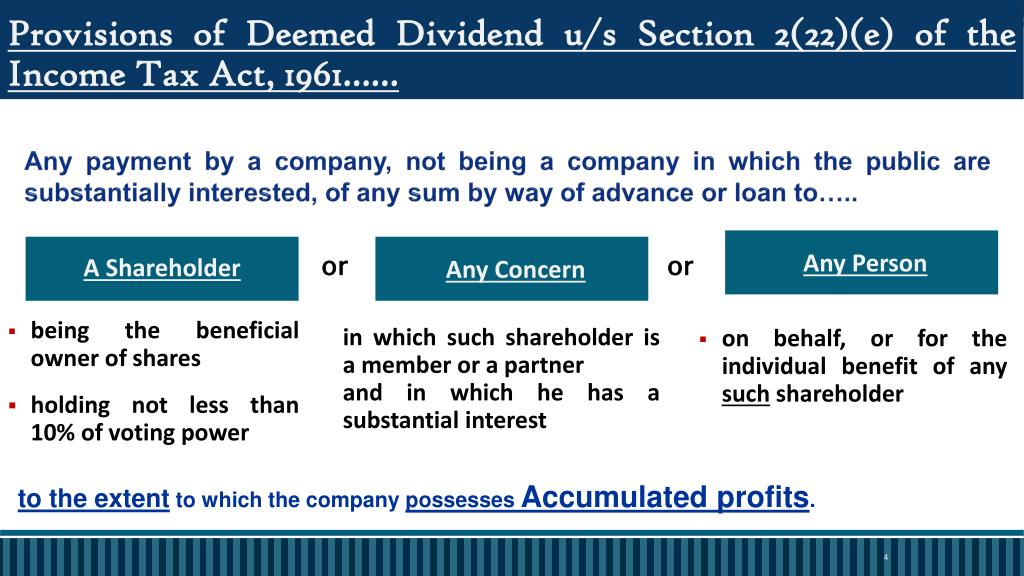

As per Section 2(22)e, where a closely held company gives a loan or extends an advance payment to the respective staff:

FACTS

One ‘H’ was a shareholder of ‘P’ Ltd. which held shares in Assessee Company. ‘H’ had borrowed amounts from the assessee company.

The Assessing Officer sought to bring the assessee company to tax under section 2(22)(e) holding that ‘H’ had more than 10 percent stake in the assessee company and conditions spelled out in section 2(22)(e) were satisfied.

A assessee contended that said ‘H’ could not be considered as a shareholder in the assessee company. The other contention was that said ‘H’ could not be considered even as a beneficial shareholder of the assessee company.

Appeal, the Commissioner (Appeals), as well as the Tribunal, held that section 2(22)(e) would not be applicable.

On appeal, it was held that:

The individual ‘H’ was not a shareholder of the present assessee but rather the shareholder of another concern that held shares in Assessee Company.

With respect to section 2(22)(e), the mandatory need to fulfill both pre-conditions which are conjunctive and not dis-conjunctive i.e. the shareholder must be

(a) Registered shareholder; and

(b) A Beneficial shareholder.

In the absence of any finding that ‘H’ owned the shares or was the beneficial owner in terms of such provision – on both counts – the findings being adverse to the revenue, no question of law arises.

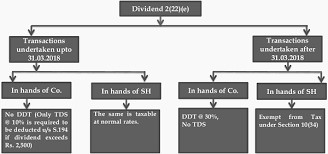

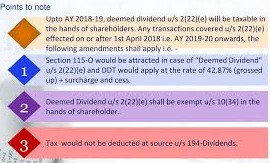

Finance Act 2018 levied Dividend Distribution Tax @ 30% under section 115-O, on deemed dividend under section 2(22)(e), in the hands of payer company.

It sought to levy this tax on closely-held companies as they usually hide dividends by making them look like loans or advances.

At the same time, however, an exemption under section 10(34) is granted to the beneficiary in respect of the said dividend deemed to have been paid.

There are few requirements that come into play at the time of the determination of the tax on the dividend. Here they are:

But, there are exceptions, which payments are not considered as deemed dividend. Like below :

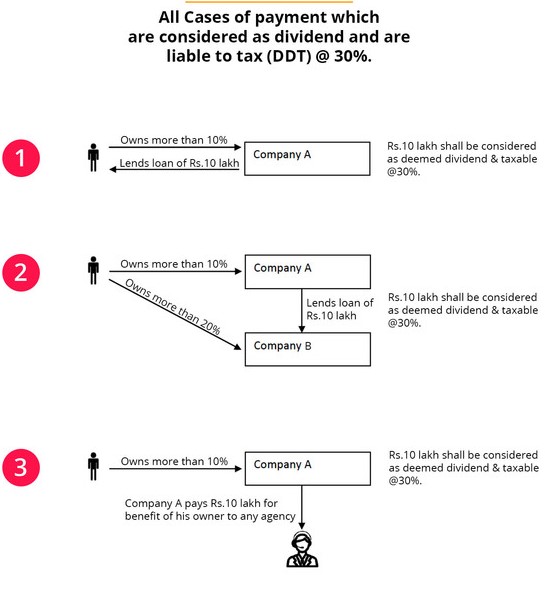

When the company generates profits, payments like these are deemed as dividend u/s 2(22)(e). But loans handed out by a subsidiary company to its parent company are also subjected to this section.

DDT Tax is levied on dividend income in either the declaration or the payment or distribution of it in the year. As per the provision, recipients are not taxed for dividends as it receives Tax exemption.

But deemed dividends do not receive that exemption. Shareholders do have to pay a nominal income tax at the rate applicable.

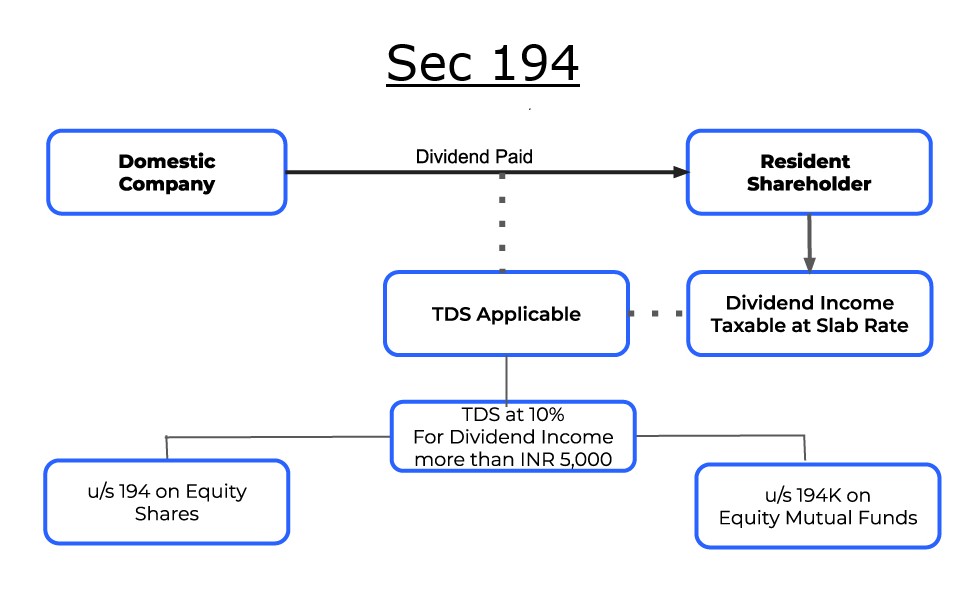

The TDS deduction is @10% on the No of dividends, only if a resident shareholder’s total dividend in a FY Cross Rs Five thousand,

In Summary:

Also, read ;

Taxation on Income from Equity and Debt Mutual Fund

Basic of Bitcoin Taxation in India

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}