Top Govt Scheme Launched for the Public & National benefits

Pradhan Mantri Matru Vandana Yojana

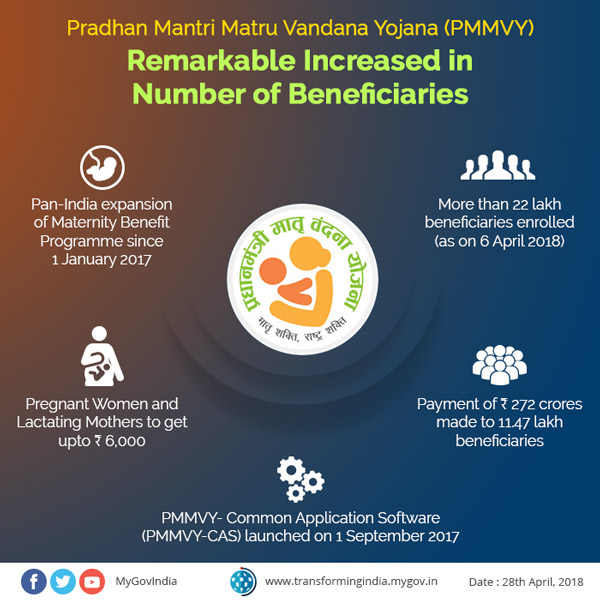

- The Pradhan Mantri Matru Vandana Yojana – PMMVY is a maternity support scheme provided by the Indian government, in which pregnant women and lactating women receive a cash reward of Rs. 5,000.

- Opportunity is given for the family’s first living child to meet the unique maternal and newborn health conditions.

Targets of Parthan Mantri Matru Vandana Yojana

The Government-run policy seeks to meet the following goals:

- To offer benefits for the income loss in cash benefits, so that the mother can take sufficient rest before and after the first living child is born.

- It is a partial payout and is part of a deal to give the woman on average a cumulative amount of Rs. 6,000. After institutional distribution, the remaining cash reward (of Rs . 1,000) comes under Janani Suraksha Yojana (JSY).

- Enhancing wellbeing promoting activity in pregnant women and mothers who are lactating.

The benefit of PMMVY especially giving to :

- For pregnant women and lactating mothers except those who are in routine jobs with the Central / State or Public Sector Undertakings (PSUs) or those who under some statute enjoy similar benefits.

- In case Qualifying pregnant women and lactating mothers getting their pregnancy with the first child in the family on or after January 01, 2017.

The date and point of a beneficiary’s conception are counted for the date of her Last Menstrual Period (LMP), as shown in the Mother and Child Security (MCP) card.

How to enrol for a Pradhan Mantri Matru Vandana Yojana?

- A recipient may only register for the programme within 730 days of their Last Menstrual Period (MP).

- Under the system the LMP reported in the MCP card is regarded as the Date of Pregnancy.

Process for getting benefit under PMMVY

A. Offline Process

Step-1: Qualifying women wishing to take advantage of maternity benefits under the scheme must register for the scheme at an Anganwadi Centre (AWC) or an authorised (government) health facility, whichever is the implementation department for that specific State / Union Territory. You must file within 150 days of LMP.

Necessary Documents:

-

- Copy of the Bank / Post Office Passbook

- An agreement/consent properly granted between the claimant and her spouse,

- Copy of Proof of Identity

- Duly filled out Form 1A

- MCP-card copy

Application form can be accessed free of charge from the AWC / approved health centre, or downloaded from the Ministry of Women and Child Development website.

For future documentation, the claimant should get an approval of registration from the implementing authority.

Step-2: After 6 months of pregnancy, the recipient may demand the second instalment of the benefit by submitting the properly filled Form 1B at the AWC / approved health care facility, along with a copy of the MCP card showing at least one Antenatal Check-up (ANC) and a copy of the Form 1A recognition slip.

Step-3: In order to assert the third instalment, the recipient must request a properly filled out Form 1C along with a copy of the childbirth certificate, ID evidence and MCP card indicating that the infant has earned the first cycle of CG, OPV, DPT and Hepatitis B immunisation.

B. Online Process

Step-1: Visit https:/pmmvy-case.nic.in and log in to the PMMVY software using authentication information from the facilitator of the scheme (AWC / approved health facility).

Step-2: To enrol under the program, click on the ‘Current Beneficiary’ tab by filling in the information as per the Beneficiary Registration Form (also called Application Form 1A). You should follow the instructions for filling out the form given in PMMVY CAS User Manual.

Step-3: After 6 months of pregnancy, log in to the PMMVY CAS app again and click on the ‘Second Update’ tab and fill out Form 1B according to the guidance in the user manual.

Step-4: After the child’s birth and completion of his/her first CG, OPV, DPT and Hepatitis B immunisation period, log in to the PMMVY CAS app and click on the ‘Third Update’ tab and fill out Form 1C according to the instructions given in the user manual.

See the ‘Offline Protocol for Availing Maternity Benefits under PMMVY’ segment above to know the documentation needed at each of the points.

Situations

A. In the case of Miscarriage or still Birth

- A recipient will be entitled to claim the remaining instalment(s) for a potential pregnancy in the event of a miscarriage or stillborn.

- For example, whether the recipient had a miscarriage after earning the first cash reward payment, she will then be able to collect the second and third instalments for a subsequent birth.

B. In the case of Infant Mortality

- In the case of child mortality, a recipient will not be entitled under the programme to seek compensation if she had already received all the maternity benefit instalments under PMMVY.

KISAN VIKAS PATRA

Introduction

- Kisan Vikas Patra (KVP) is an investment scheme in the form of certificates available at Indian Post Offices. It’s a small fixed rate investing plan intended to double the contribution over a specified period of time (124 months in the issue currently available).

- The scheme is established to enhance consumption and savings among the population over the long term. It is ideal for investors who are hesitant to take chances, have excess capital and are searching for guaranteed returns.

- KVP certificates may be obtained from select public sector banks as well as from India Post Offices, in compliance with the existing laws.

Varieties of KVP

- Single Holder certification: Provided to an individual adult or on behalf of a minor

- In case Joint A: Provided collectively to two adults. This is liable to the individuals or the person who survives until maturity

- Joint B: Provided jointly with two adults and charged to either the owner of the survivor before maturity

Characteristics of KVP

Kisan Vikas Patra is a Government-scheme who provide fixed return and that produces secured dividends. The main characteristics of the Scheme are as follows:

- Certificates are currently available in the Rs 1,000, Rs, 5,000, Rs 10,000 and Rs 50,000 variants.

- The certificates are readily accessible at all Indian Post Offices and KVP Application forms can be found online as well as at Indian Post Offices and at some select banks.

- Maturity period can vary on the basis of rate changes made by the ministry of finance. The maturity value is pre-printed on the issued certificate.

- Kisan Vikas Patra Account may be initiated with a minimum initial Rs.1000 deposit (in Rs.100 multiples);

- There is currently no upper limit on contributions under the KVP.

- Kisan Vikas Patra can be moved quickly from one post office to another and from person to person.

- According to terms and conditions, premature encashment permitted after two and a half years.

Eligible criteria for KVP

Eligibility conditions for investment in the KVP scheme are as follows:

- In Kisan Vikas Patra, the Hindu Undivided Families (HUFs) and the Non-Resident Indians (NRIs) can not contribute.

- The applicant must be an adult Indian citizen.

- The parent/guardian can invest on the minor’s behalf

Advantages of KVP

KVP is not designed to target tax-savvy buyers. There are no tax deductions on the principal sum and the interest. But it also gives customers a few primary advantages.

Some of the advantages are Explain here:

- Kisan Vikas Patra can be used as collateral for receiving loans from banks at desired rates.

- Long-term development of wealth as Kisan Vikas Patra helps you to remain invested for nearly 10 years and doubles your cash.

- Transferable from person to person and from the post office to post office.

- Ensured returns as a KVP certificate is a tool backed up by the government.

- The customizable investing instrument, as KVP, does not have an upper limit.

Maturity Period of KVP

- As per the latest amendment of the scheme, the maturity period is 10 years and 4 months (124 months). The sum invested will return after the term of the scheme has been finished.

- For example: If an individual has spent Rs.10,000, at maturity he/she will get Rs.20,000 at the end of the maturity.

Documents needed to receive Kisan Vikas Patra

To get a KVP certificate, the Applicant must supply copies of the following documents:

- Proof of identity for KYC process (Aadhaar card / PAN / Voter ID card / Passport / Driving licence)

- Application Form for KVP

- Proof of Address

- Certificate of Date of Birth

Download form to apply for KVP

- To request for a Kisan Vikas Patra certificate, you must submit the application form online or get that from the Post Office directly.

- You need to fill out and submit this form at the Post Office.

Points to be remembered;

- The purchase amount must be specifically shown in the form below. Prevent cutting and rewriting

- Please state the check no. on the form if you make the payment by check

- Specify whether KVP is acquired on the basis of single or joint ‘A’ or joint ‘B’ subscription. Where bought jointly, state the names both of beneficiaries

- The full name, date of birth and the nominee’s address (if any) must be specified on the form

- On submission of the form, the KVP certificate shall contain the name of the applicant, the date of maturity and the sum of the maturity

- The document should be forwarded to the Post Office’s corresponding Postmaster General, where it is submitted

- Payments can be made via Cheque or Cash against the KVP form

- If the beneficiary is a minor, Specify the date of his / her birth (DOB), the name of the parent, the name of the guardian

Transfer of Kisan Vikas Patra

1.Post office to another post Office

- The Department of Post, India has provided consent to the move of a certificate from one post office to another for the comfort of subscribers.

- To facilitate the transfer from the registered post office to some other post office, the account holder must fill out the KVP Transfer Form-B and send it to the registered post office along with all the documentation required:

Records required for transfer of KVP Post Office:

- Form B, properly filled and approved

- Identity of proof (Aadhaar Card / PAN Card / Voter ID)

- Address proof (Passport / Electricity bill / Water Bill / Bank statement)

- Original certificate of KVP

- Transfer confirmation certificate, signed by the account holder

2. One person to another person

The recipient must request a written application at the registered Post Office for the move of KVP Certificate from one person to another. In the following situations, the transfer is necessary-

- Passing of a Deceased ‘s Certificate to his / her successor

- From cooperative owners to sole proprietors

- In case From sole proprietors to mutual owners

- From beholder to statute magistrate

Calculation of maturity amount of Kisan Vikas Patra (KVP)

- A detailed description of the measurement of the maturity and interest rates under Kisan Vikas Patra is given below.

- Note: Minimum contribution expected to be Rs.1000

| Duration → | 15th Jan 2000-28th Feb 2001 | 1st March 2001-28th Feb 2002 | 3rd March 2002-28th Feb 2003 | After 1st March 2003 |

| Year↓ | Amount Accrued ↓ |

| 1 | NA | NA | NA | NA |

| 2 | NA | NA | NA | NA |

| 2 Years 6 Months | Rs.1246 | Rs. 1209 | Rs. 1195 | Rs. 1170.51 |

| 3 Years | Rs. 1302 | Rs. 1274 | Rs. 1256 | Rs. 1207.95 |

| 3 Years 6 Months | Rs. 1407 | Rs. 1327 | Rs. 1305 | Rs. 1267.19 |

| 4 Years | Rs. 1478 | Rs. 1409 | Rs. 1382 | Rs. 1310.8 |

| 4 Years 6 Months | Rs. 1585 | Rs. 1470 | Rs. 1439 | Rs. 1355.9 |

| 5 Years | Rs. 1668 | Rs. 1572 | Rs. 1534 | Rs. 1435.63 |

| 5 Years 6 Months | Rs. 1779 | Rs. 1644 | Rs. 1602 | Rs. 1488.49 |

| 6 Years | Rs. 1874 | Rs. 1770 | Rs. 1672 | Rs. 1543.3 |

| 6 Years 6 Months | Rs. 2000 | Rs. 1857 | Rs. 1800 | Rs.1649.13 |

| 7 Years | NA | NA | Rs. 1883 | 1713.82 |

| 7 Years 3 Months | NA | Rs. 2000 | NA | NA |

| 7 Years 6 Months | NA | NA | NA | 1781.06 |

| 7 Years 8 Months | NA | NA | Rs. 2000 | NA |

| 8 Years & 8 Years 7 Months | NA | NA | NA | Rs. 1850.93 |

| 8 Years 7 Months | NA | NA | NA | Rs. 2000 |

| More than 8 years 7 Months | NA | NA | NA | NA |

Rate of interest offered under the scheme i.e. Kisan Vikas Patra

- The interest rate applicable to Kisan Vikas Patra (KVP) can adjust periodically depending on the Ministry of Finance’s announcements.

- Average interest rate for KVP is 6.9 per cent per annum, which double the savings in 124 months.

Historical interest rates paid under the Kisan Vikas Patra scheme * are:

| Time Period | Interest Rate of KVP |

| Q1 FY 2020-21 | 6.9% |

| Q4 FY 2019-20 | 7.6% |

| Q2 FY 2019–20 | 7.6% |

| Q1 FY 2019–20 | 7.7% |

| Q4 FY 2018-19 | 7.7% |

| Q3 FY 2018-19 | 7.7% |

| Q2 FY 2018-19 | 7.3% |

| Q1 FY 2018-19 | 7.3% |

- KVP compounded interest annually

Withdrawal of money before the expiry of the period

Investors are entitled to withdraw their investments under the scheme at any given time but there are some limitations:

- No interest will be granted on premature withdrawals made within 1 year. Even the beneficiary will have to pay a tax according to scheme legislation.

- In case Premature withdrawals made after 1 year for up to 2.5 years shall earn interest but at a discounted rate.

- Premature withdrawal after a 2.5-year period will not incur any fines and will therefore earn interest at the appropriate rate.

Calculation of premature redemption value

- Here’s an instance of measuring the balance assigned to the KVP certificate on premature redemption. Let’s say the denomination for a certificate was Rs.1000:

| Encashment After | Amount to be Received (Including Interest) |

| 2.6 yrs but less than 3 yrs | Rs.1,176 |

| 3 yrs but less than 3.6 yrs | Rs.1,215 |

| 3.6 yrs but less than 4 yrs | Rs.1,255 |

| 4 yrs but less than 4.6 yrs | Rs.1,296 |

| 4.6 yrs but less than 5 yrs | Rs.1,339 |

| 5 yrs but less than 5.6 yrs | Rs.1,383 |

| 5.6 yrs but less than 6 yrs | Rs.1,429 |

| 6 yrs but less than 6.6 yrs | Rs.1,476 |

| 6.6 yrs but less than 7 yrs | Rs.1,524 |

| 7yrs but less than 7.6 yrs | Rs.1,575 |

| 7.6 yrs but less than 8 yrs | Rs.1,626 |

| 8 yrs but before 8.6 yrs | Rs.1,680 |

| 8.6 yrs but less than 9 yrs | Rs.1,735 |

| 9 yrs but before maturity | Rs.1,793 |

| On maturity | Rs. 2,000 |

Tax liability for Kisan Vikas Patra

- Under this scheme, no tax-benefits are available. The accumulated interest is taxable under ‘Income from Other Sources,’ paid annually. And, 10 % TDS is deducted from the interest.

- Thus the final maturity amount is excluded from tax deductions.

Kisan Vikas Patra (KVP) vs. Fixed deposit(FD) vs. National Saving Certificate(NSC)

- A Fixed Deposit is applied to a bank or NBFC managed financial instrument that provides borrowers with higher interest rates than saving accounts.

- National Savings Certificate is an Indian Government Savings Bond that is used in India as a tool for small deposits and income tax saving schemes.

| Basis of difference | Kisan Vikas Patra (KVP) | Fixed Deposits (FD) | National Saving Certificate (NSC) |

| Investment | Minimum- Rs.1000 Maximum- No limit | Minimum- Rs.50 Maximum- Not Limited | Minimum- Rs.100 Maximum- Rs.1,50,000 |

| Rate of Interest | 6.9% annually | Differs from bank to bank. Highest ROI is offered by IDFC bank i.e, 8.50% | 6.8% annually |

| Maturity Period | 10 years and 4 months | 10 years. However, subscribers can withdraw money after 7 days from the date of investment | 1. NSC under VIII issue mature in 5 years. 2. NSC under IX issue mature in 10 years. |

| Premature Withdrawal | Withdrawals are allowed before maturity but it is advised to keep the corpus invested for 8 years to get best returns | Money can be withdrawn as and when the subscriber wants, after 7 days | Withdrawals before maturity are very difficult and restricted |

| Liquidity | Lock-in period of 2 and a half years | No lock-in period. The tenure of Fixed deposits range from 7 days to 10 years | Lock-in period of 5 or 10 years |

| Tax Treatment | Returns on KVP are taxable | Tax saver FDs are tax exempted for up to Rs.1.5 Lakh under Section 80(c) | Enjoys tax benefits and exemption under Section 80(c) |

Prime Minister’s Social Security Schemes

- Insurance plans and pension schemes in India are being widely overlooked. A relatively small number of Indians vote for protection schemes.

- Prime Minister Modi initiated three Social Security Programmers to allow more people to participate in those programmers like Pradhan Mantri Jeevan Jyoti Bima Yojana, Atal Pension Yojana and Pradhan Mantri Suraksha Bima Yojana

- Here’s a summary on the three schemes of social security:

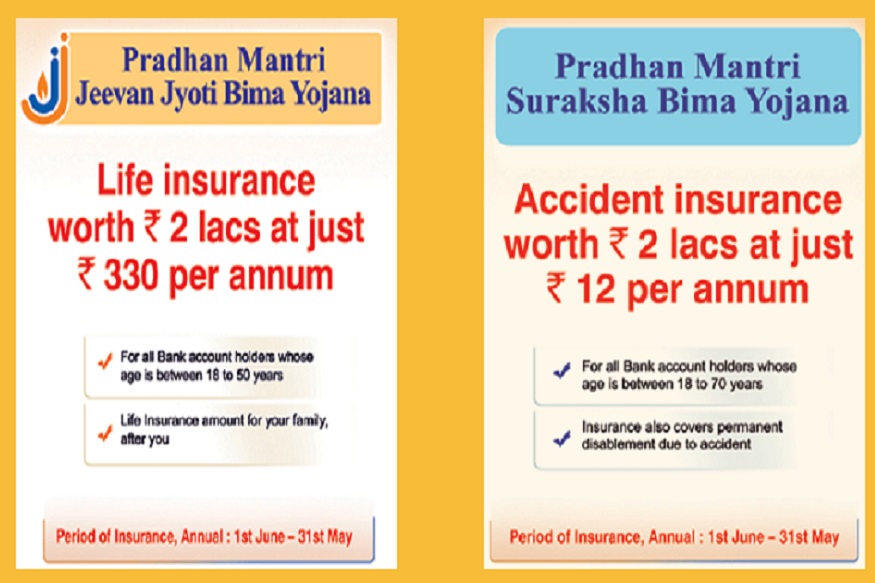

1. Pradhan Mantri Suraksha Bima Yojana (PMSBY)

- Due to the increasing importance of life insurance, the Prime Minister launched the PMSBY which provides life cover for people aged 18 to 70-year-old.

- For a small premium rate of only Rs. 12 per annum, this scheme guarantees that all those living below the poverty line can afford life cover.

- In the event of an unexpected death or the insurance holder’s total disability, a sum of Rs. 2,00,000 will be paid to the family. And in case of partial handicap a sum of Rs. 1,00,000 will be given.

- In reality PMSBY is interconnected with Jan Dhan Yojna. All who have their accounts under the Jan Dhan Yojana Scheme are liable under this scheme for life protection.

- Prime amount is deducted annually directly from the account.

- The insurance cover will be discontinued until the person is 70 years old or if the account balance isn’t adequate to subtract the annual premium.

2. Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

- PMJJBY is a Government-backed life insurance scheme. Figures reveal that just 20 per cent of the Indian population opts for insurance of any kind.

- This system is targeted at supporting insurance policies and increasing customer numbers.

- Anyone between the ages of 18 and 50 years, can get the benefit of the Pradhan Mantri Jeevan Jyoti Bima Yojana. To get the benefit of this scheme, you must pay Rs. 330 per annum (and taxes) amount.

- It provides a sum amount of two lakh rupees in sustainable life insurance protection in case of death due to any cause unexplained.

- An insured person has to keep a savings bank account with respect to the participating bank.

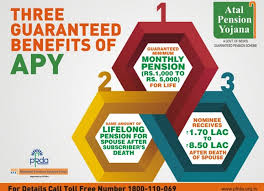

3.The Atal Pension Yojana (APY)

- In Hindustan, the percentage of the population who apply for pension plans is very limited, in general, and especially among the weaker masses.

- Prime Minister Modi launched the Atal Pension Yojana to allow the working poor to get benefit from pension schemes. This scheme focuses on the employees from India’s unorganized market.

- The scheme is available to all holders of bank accounts. A guaranteed income would be applicable to members between Rs. 1K and Rs. 5K if they enter the scheme between 18 years and 40 years of age.

For five years, if apply before December 31, the Central Government will pay

- 50 % of the gross contribution or

- Rs. 1000/-per annum

whichever is lower.

The termination threshold for the donation and the initiation of the pension is 60 years.

Also, check out these two other significant schemes which are directed specifically at the economically weaker classes:

1. Pradhan Mantri Jan Dhan Yojana

- The scheme aims to offer standard bank and debit card accounts to everyone. A person at zero balance can open an account with any branch of the bank.

- Few key highlights are, for all Aadhaar-linked accounts, Rs. 5K overdraft facility, A Rupay Debit Card pre-loaded with Rs. 1,00,000 accidental insurance cover.

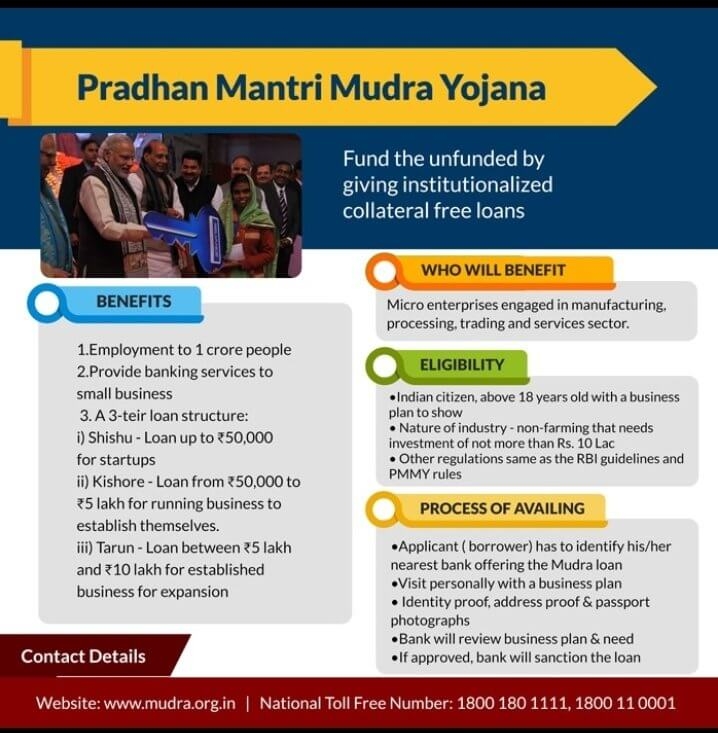

2. Pardhan Mantri Mudra Yojana (PMMY)

Under the Pradhan Mantri Mudra Yojana (PMMY), the Mudra Loan is made available to micro and small non-farming & non-corporate enterprises. Here are the Loan Details:

| Amount | The upper limit of Rs. 10,00,000. For e.g. · Shish – Loans up to Rs. 50,000 · Kishore – from Rs. 50,001 – Rs. 5,00,000 · Tarun – from Rs. 5,00,001 – Rs. 10,00,000 |

| Fees of Processing | Shishu and Kishore – no fee Tarun – 0.5% of the loan amount |

| Eligibility | Both for New as well as existing enterprises |

| Time period | 3-5 years |

Bhamashah Yojana

Introduction

- On 15 August 2014, Rajasthan’s government launched Bhamashah Yojana in a straightforward way for the simple allocation of financial and non-financial benefits of government schemes to female beneficiaries.

- Bhamashah Yojana is known to be the first step towards digital transformation in the state.

- The scheme is named after Bhamashah, a popular minister, financier and general of the army who was a close assistant of Maharana Pratap when he became financially vulnerable to the degree that he reached the point of poverty.

- Financial and qualifying candidates are distributed from the end to the end and advantage and non-financial service.

Objective

- Launched with the aim of women’s financial inclusion and advancement, the Rajasthan Bhamashah Yojana was initially launched in 2008, when about 50 lakh women registered, and at that time only 29 lakh accounts were available.

- The initiative seeks to make women financially stable and through the Bhamashah Card Yojana provides the benefits of several other schemes.

- Bhamashah card issued under this yojana in the house woman’s name is connected to a bank account.

- The card also provides the women with biometric authentication and key banking features, along with several cash incentives that are deposited directly into the bank account.

Bhamashah Card

- The applicants who apply for the Bhamashah scheme will get their Bhamashah cards which are made in their family’s woman’s name.

- Using the card all family members will be eligible to take advantage of the rewards. Candidates can register for the card using online as well as offline tools.

For access the Bhamashah card is

- University tuition Stipend for

- Loan for small business startup

- Free medical care for such conditions and procedures at designated hospitals

- Recognition of Unrestricted and Subsidized Ration recipients

- Women pursuing vocational training to develop their careers

Characteristics of Bhamashah Yojana

- Scheme aims to pass benefits provided by the Government of the State directly to the helpless women in society

- The scheme allowed 1.5 Million women to open their bank accounts and take advantage of the benefits

- Bhamashah Card also gives Rs.30000 medical protection to the needy and the vulnerable in the event of medical emergencies

- Women carrying the Bhamashah Card will buy ration from the stores using the biometric method.

- Government benefits from Bhamashah Yojana are paid directly to the beneficiary’s account, which also leads to minimising wrongdoing

- The Bhamashah Card is issued to the students and mentally disabled individuals qualifying for the scheme

- Men can also take advantage of Bhamashah Card benefits by paying Rs.20 or Rs.25.

Qualification to apply Bhamashah Yojana

The following conditions must be fulfilled to apply for the Bhamashah Yojana-

- Adults needing financial assistance to start up a business

- People needing medical care requiring financial support for operations.

- Children must be registered in government schools and colleges that offer enrolment in learning institutions to train for coaching tests.

- Women who fight for their identities and want to set themselves up as leaders

How to Apply for Bhamashah Yojana

1. Offline application

To qualify for the scheme offline, the candidates will visit the camp in both rural and urban areas arranged by the state government for each ward in all the village panchayat.

2. Online application

- Even the qualifying candidates can apply online for the Bhamashah Yojana by submitting their Aadhaar number.

- The applicant will be asked to fill out a form the details of which will be used for the Bhamashah card production.

- If the candidate does not have her Aadhaar number, the candidate may use e-Mitra- Kiosk to get her Aadhaar card and then apply for the scheme.

How to modify Bhamashah Portal Info

In the event of any modifications to the Bhamashah card, candidates are required to access the official website and make the changes themselves.

You may update the following information on the Bhamashah online portal-

- A family member expired

- Changes in related records, for example, bank account

- Addition of new family member

- Change of place of residence address

- Marriage for every family member

But the applicant would have to use her SSO ID to edit Bhamashah online.

Necessary documents to apply for Bhamashah Card

Please send the following documents when applying for the Bhamashah card online-

- A copy of the application

- Certificate of caste

- Letter of expérience (for businesses)

- Certificate of birth

- Proof of identity (Aadhar card, passport, ration card, etc.)

Pradhan Mantri Awas Yojana

- If you are trying to buy a house under Pradhan Mantri Awas Yojana ( PMAY) from the government, you might consider buying it under the Credit-Related Subsidy Scheme (CLSS).

- Government has extended the time-limit for subsidised CLSS housing until March 31, 2021. Pradhan Mantri Awas Yojana (Urban) was initiated on 25th June 2015 to provide pucca houses to all deserving beneficiary by 2022 to ensure accommodation for everyone in urban areas. Pradhan Mantri Awas Yojana (Urban) Project launched on June 25, 2015, to provide accommodation for citizens in urban areas by 2022.

- Project offers central assistance to implementing partners by States / Union Territories (UTs) and Central Nodal Agencies (CNAs) to provide accommodation for all qualifying families/beneficiaries against approximately 1.12 cr validated housing demand.

- The size of a house for the Economically Weaker Group (EWS) may be as large as 30 sq according to PMAY(U) guidelines. Mt. carpet region, however, Member States / UTs have the ability to raise the size of houses in conjunction and Ministry approval.

How to get your name on the PMAY list

If you’ve already enrolled for Pradhan Mantri Awas Yojana ( PMAY), the PMAY List includes four ways to find your name and information.

Pradhan Mantri Awas Yojana List:

- Candidates to the Pradhan Mantri Awas Yojana (PMAY) look forward to having their own house under the government’s flagship ‘Housing for All’ scheme by 2022.

- The main feature of the PMAY system is the Credit-Related Subsidy, which allows the owner to hold down the expense of buying the property.

- There are various criteria for qualification and after registering, the PMAY applicant receives a registration ID from which he or she can check the application’s viability.

- If you’ve already requested for Pradhan Mantri Awas Yojana ( PMAY), the PMAY List includes 4 ways to find your name and information.

- You might want your Aadhaar number, mobile phone, registration ID or examination ID to find the information, as the criteria vary in each case.

- The list Pradhan Mantri Awas Yojana can either list PMAY Urban or list PMAY-Gramin (rural). Here are four ways to search the Urban PMAY List and PMAYG list.

1. Check PMAY Urban List

A. With the use of Aadhar Card

By visiting https:/pmaymis.gov.in, visit the official PMAY website;

Press the link below: https:/pmaymis.gov.in/Find Beneficiary Details.aspx

To go to the next tab, click on ‘Search Beneficiary’ in the top pane. There was formerly an alternative to pick ‘Search By Name’ from the drop-down menu of ‘Search Beneficiary.’

Type your Aadhaar number on the next page and submit it.

Specifics of your PMAY response will be shown along with the status upon submission of the requisite information.

B. Without Use of Aadhar Card

You can check the Pradhan Mantri Awas Yojana list with your personal information and mobile number or with your assessment ID if you don’t have the Aadhaar number available with you.

• https:/pmaymis.gov.in/Track Application Status.aspx connect

• Enter personal information or assessment ID to obtain compliance status for PMAY compliance.

2. Check the list on PMAY-G

A.with the help of Registration number

If you have the registration number, please visit the official PMAY-Gramin website at https:/rhreporting.nic.in/entity/Beneficiary.aspx to see your name and other info on the PMAY Rural List.

B. Without the help of registration number

However, if you don’t have the registration number, the information might be available on the official PMAY-Gramin website.

• On your computer, to link https:/rhreporting.nic.in/entity/Beneficiary.aspx.

• You will be required to select State, District, Block, Panchayat, Scheme name, and other information on the next page.

• Your contact information, bank details, website details, fines, and complete details will be given upon request.

Tax planning tips for availing tax-saving benefits

National committee on deduction benefits u/s 35AC

Regards

Rajput Jain & Associates

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}