Page Contents

POINT TO BE NOTED:

The requirement of Rs 1 crore for a tax audit is expected to be raised to Rs 5 crore with effect from AY 2020-21 (FY 2019-20) if the taxpayer’s cash receipts are restricted to 5 % of the gross receipts or turnover and if the taxpayer’s cash payments are restricted to 5 % of the aggregate payments. Below are different categories of taxpayers below:

| Category of person | Threshold |

| Business

| |

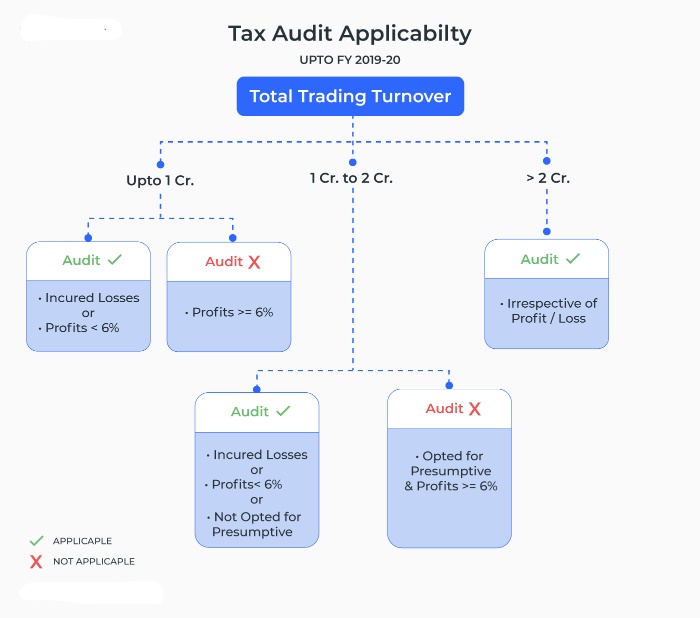

| Carrying on business (not opting for presumptive taxation scheme*) | Total sales, turnover, or gross receipts exceed Rs 1 crore in the FY |

| Carrying on business eligible for presumptive taxation under Section 44AE, 44BB or 44BBB | Claims profits or gains lower than the prescribed limit under the presumptive taxation scheme |

| Carrying on business eligible for presumptive taxation under Section 44AD | Observe taxable income below the limits specified by the presumptive taxation system and has income that exceeds the basic limit. |

| Carrying on business and is not eligible for presumptive taxation under Section 44AD by opting for presumptive taxation in any one financial year of the lock-in period, i.e. 5 consecutive years from the date on which the presumed taxation system was implemented. | If the income reaches the permissible amount not to be paid for tax in the following five successive tax years from the financial year in which the assumption of tax was not introduced, |

| Carrying on business which is declaring profits as per presumptive taxation scheme under Section 44AD | If the overall revenue, turnover, or gross receipts for the financial year do not exceed Rs 2 crore, the tax audit would not apply to such entities. |

| Profession

| |

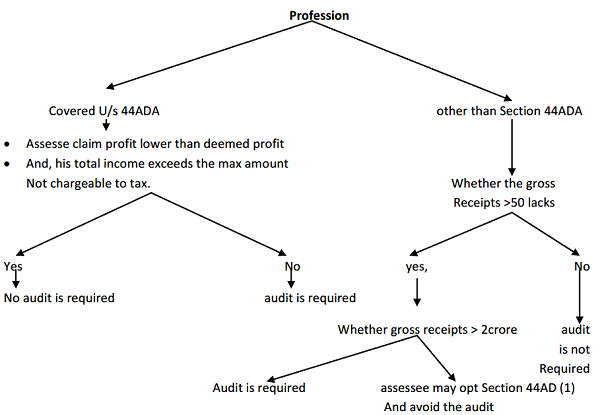

| Who Carrying on the profession | Total gross receipts exceed Rs 50 lakh in the FY |

| Who Carrying in the profession is eligible for presumptive taxation under Section 44ADA | 1. Claims for profit or gains below the permissible level under the presumptive taxation scheme 2. Profits increases the permissible sum not to be paid for taxation |

| In case of loss from carrying on of business and not opting for a presumptive taxation scheme | Total sales, turnover, or gross receipts exceed Rs 1 crore |

| If the gross income of the taxpayer exceeds the basic threshold but has suffered a loss from carrying on a business (not opting for a presumptive taxation system) | In case of loss from business when sales, turnover, or gross receipts exceed 1 crore, the taxpayer is subject to tax audit under 44AB |

| If continuing on business (opting a presumptive tax scheme under section 44AD) and making a business loss but with profits below the basic level | This Tax audit does not apply |

| If going on business (presumed tax scheme under section 44AD applicable) and making a business loss but with profits above the basic threshold | Declares taxable income far below limits specified by the presumed tax scheme and has income that exceeds the basic level. |

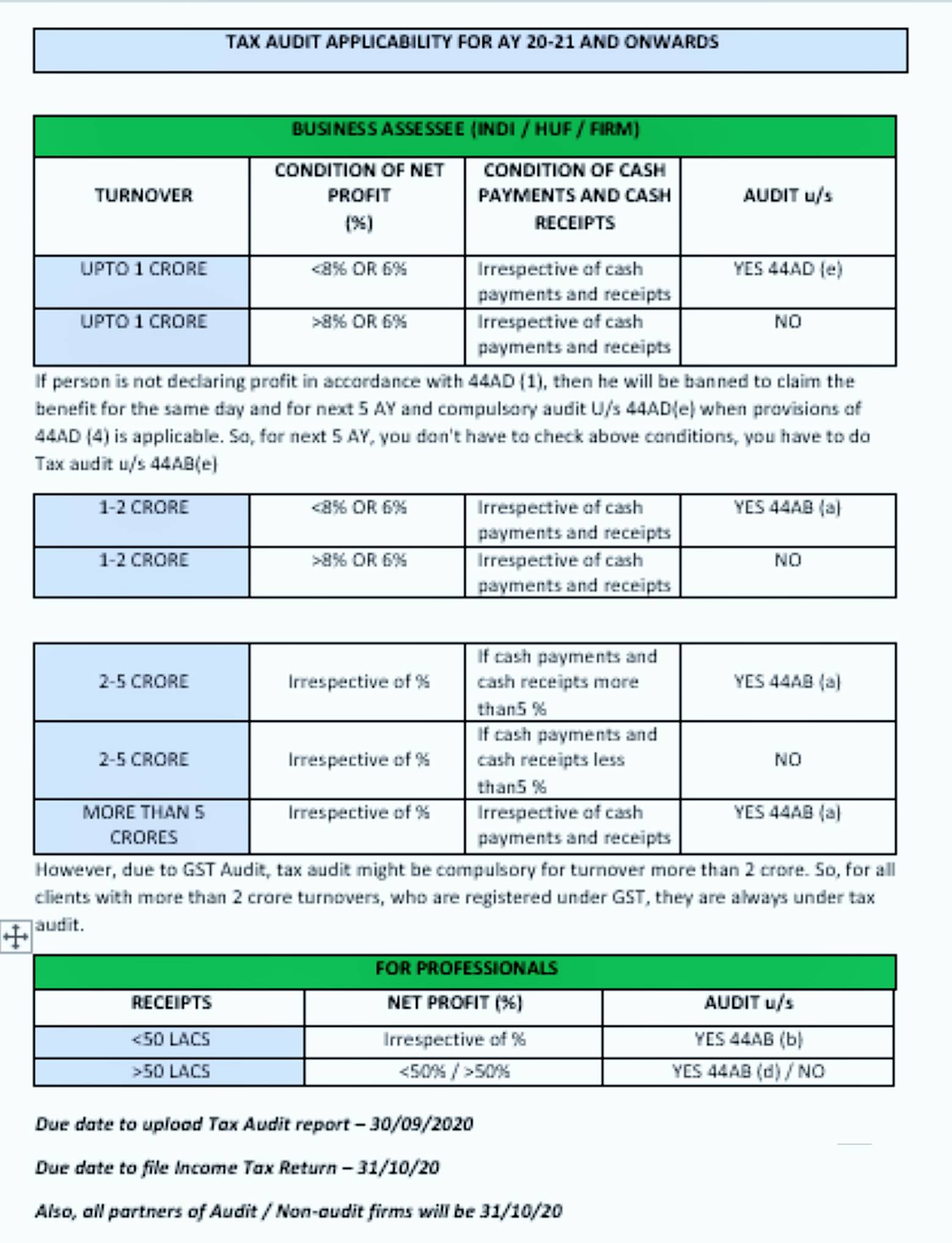

For effective from 01/04/2020, that is to say from the assessment year 2020-21, this requirement is changed as follows:

The scenario is as follows:

– In case Assess who have TO>2 crores (but less than 5 crores and have cash receipts and cash payments not exceeding 5 percent), they are NOT liable for a tax audit. This holds true regardless of whether the assessee shows income of up to 6 percent or 8 percent in 44AD or not.

– For assesse who have TO<2 crores (but have cash receipts and cash payments not exceeding 5 percent), they are liable for tax audit if they do not have an income of up to 6 percent or 8 percent as per 44AD.

Popular blog:-

Amendment in Tax Audit u/s 44AB

Deduction u/s 80CCD of Income Tax Act, 1961

Summary of the Proposed Amendments to the IBBI Liquidation Regulations (2026) The document proposes major changes to India's liquidation… Read More

India has consistently maintained that the power to enact laws rests exclusively with its Parliament, acting within the framework of… Read More

Alternative (lower) tax regimes are available to assessees other than individuals/HUFs under the Income Tax Act. What does it mean?… Read More

ITR Filing Assessment Year 2026-27: Due Dates, New ITR Changes, Revised Return Rules & Compliance Guide The due dates for… Read More

Tax Audit at a Glance: Important Points for Futures & Options Traders Income Tax Treatment of Futures & Options Traders… Read More

Common Misconception of Crypto taxation in India Crypto Futures Contracts A crypto futures contract is a legal agreement between two… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}