Page Contents

In case of Samsung India Electronics (P.) Ltd. Vs. Commissioner of Central Excise and Service Tax, New Delhi (2015) 59 taxmann.com 444 (New Delhi-CESTAT) honorable Delhi CESTAT held that secondment/expatriation of staff does not amount to ‘manpower supply services’.

In the Instant case, assessee was an Indian subsidiary of Samsung, Korea. The Samsung, Korea provided expatriates to assessee, for which assessee paid certain amount to said foreign holding company.

Department argued that it amounted to ‘manpower supply services’ and was liable to tax under reverse charge in hands of assessee.

Honorable CESTAT observed that all throughout staff had been expatriated by foreign holding company, those staff remained ’employee’ of assessee with control and supervision of assessee.

Hence, secondment/expatriation of staff from foreign holding company to assessee would not amount to manpower supply services.

DGFT

DGFT has made Amendments to Foreign Trade Policy 2015-2020, which shall be effective from 1st July, 2015: Amendment has been made with respect to the Transitional Arrangement through which facility has been provided for exporters to continue to file applications for benefits under Chapter 3 schemes of the earlier Foreign Trade Policy (ies), as per procedures prescribed in the corresponding Hand Book of Procedures, v1 2009-2014.

Further, the Applicants shall continue to file applications in respect of FPS/ MLFPS/FMS/VKGUY/SFIS/ SHIS/IEIS and Agri Infrastructure Incentive Scheme Scrip in the application form and manner prescribed in the corresponding Hand Book of Procedures.

Recently, Haryana Value Added Tax, 2003 has been amended vide Ordinance issued by the Governor dated 31.7.15 published vide Notification No Leg. 9/2015 dated 3rd August 2015.

The concerned amendment is effective with effect from 3rd August 2015. The major amendment increasing time limits for conducting assessment/ reassessment/ revision are laid down as below, for your kind perusal:

Section 16 contains provisions regarding assessment of unregistered dealer’s liability to tax. Earlier in the case of unregistered dealer, the assessing authorities could assess the tax only within a period of three years from the end of the period for which the tax is to be computed.

Now, with the amendment that period of three years has been increased to six years.

Thus, with the effect of the amendment, the assessing authority can now assess tax of the unregistered builders, within a period of six years from the end of the period for which the tax is to be assessed.

For example, the builders who are not registered in 2009-10 and no assessments has been made under Section 16 of the HVAT Act, till now, and the period of three years has also expired.

However, with this amendment, the assessments could now be made for a past period of six years from the end of the period for which the tax is to be assessed.

More read:

Further, Section 17 (reassessment) and Section 34 (revision) has also been amended for increasing the time limit within which assessing authority can reassess the tax/revise the order.

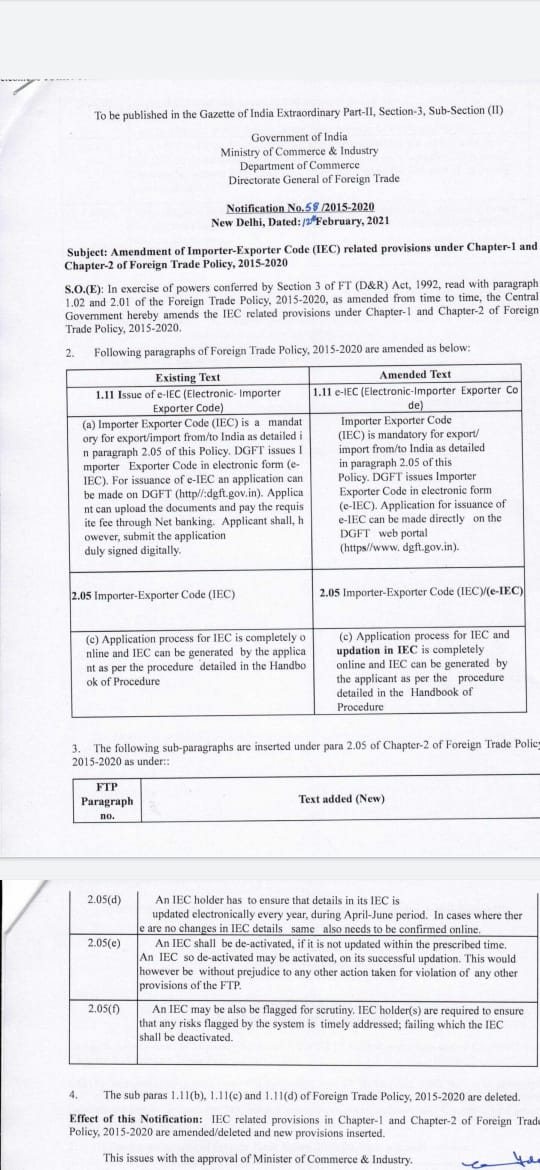

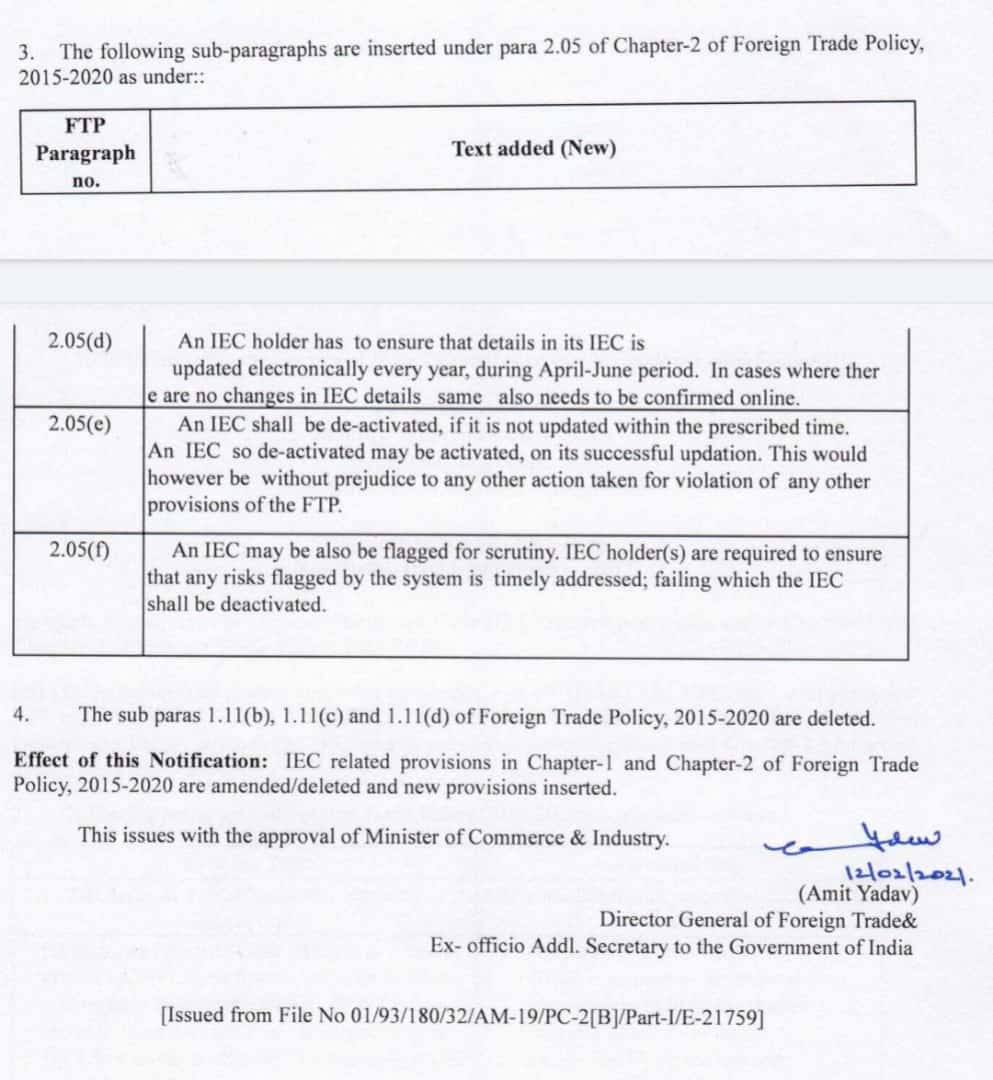

All IMPORT EXPORT CODE holders are required to update and validate their IMPORT EXPORT CODE details, Even without any modifications from April to June each year via online systems, which does not allow their IEC to be deactivated and no activity for import or export.

An IMPORT EXPORT CODE holder shall ensure that the IMPORT EXPORT CODE details are updated every year, during the period April-June, by electronic means.

If IMPORT EXPORT CODE details have not been modified, the required details must also be confirmed online.

If not updated within the prescribed time, an IMPORT EXPORT CODE shall be deactivated. On successful updating, IMPORT EXPORT CODE can therefore be deactivated. However, this would be without prejudice to any other measures taken to violate any other FTP provisions.

IEC application and update processes in IMPORT EXPORT CODE are fully online, and the applicant can produce the IMPORT EXPORT CODE in accordance with the procedure detailed in the Procedure Manual.

अपना IMPORT EXPORT CODE UPDATE कराये BEFORE 30 JUNE 2021 नही तो आपकी SHIPMENT HOLD हो जायेगी GOVERNMENT NOTIFICATION

NO 58/ 2015-220 DATE 12FEB 2021

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

Overview Taxation of Firms & LLPs in India Key aspects of taxation of partnership firms and limited liability partnerships are… Read More

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}