Page Contents

“Relative”, in relation to an individual, means the husband, wife, brother or sister or any lineal ascendant or descendant of that individual ;

As per the Income-tax act, the term “relatives” is described in detail. As gift received in the form of cash, cheque, or good from your relative is fully exempt from tax. So if you receive gift money from any of your relatives listed below, you are not liable to pay any tax on the same.

Gift received from a relative is not taxable in hands of recipients under section 56 of Income Tax Act.

The persons who are considered as relatives are

In the case of individual

| Sr no. | Relative | Covered under |

| 1. | Husband/wife | Clause(i) |

| 2. | Brother and his wife | Clause(ii)with(vii) |

| 3. | Sister and her husband | Clause(ii)with(vii) |

| 4. | Wife’s bro. and his wife | Clause(iii)with(vii) |

| 5. | Wife’s sister and her husband | Clause(iii)with(vii) |

| 6. | Kaka – Kaki | Clause(iv)with(vii) |

| 7. | Fua – Foi | Clause(iv)with(vii) |

| 8. | Mama – Mami | Clause(iv)with(vii) |

| 9. | Masa – Masi | Clause(iv)with(vii) |

| 10. | Father – Mother | Clause(v)with(vii) |

| 11. | Grandfather – Grandmother | Clause(v)with(vii) |

| 12. | Son and his wife | Clause(v)with(vii) |

| 13. | Daughter and her Husband | Clause(v)with(vii) |

| 14. | Father in Law and Mother in Law | Clause(vi)with(vii) |

| 15. | Grand Father in Law (GFIL) and Grand Mother in Law (GMIL) | Clause(vi)with(vii) |

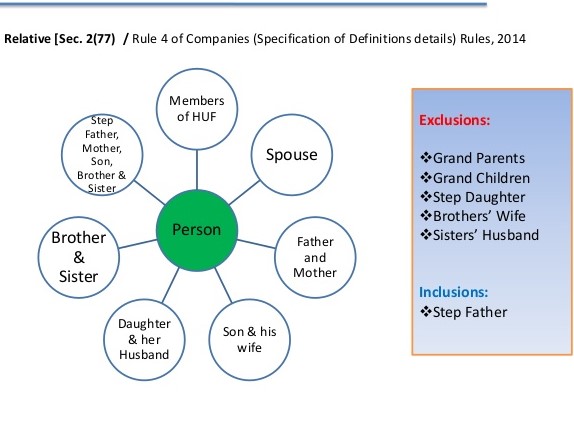

In the case of HUF – Any member of the HUF

A person shall be deemed to be a relative of another if,-

(a) They are members of a Hindu undivided family; or

(b)They are husband and wife; or

c) The one is related to the other in the manner indicated below

| Sr.no | Company`s act 2013 |

| 1 | Father(including stepfather) |

| 2 | Mother(including stepmother) |

| 3 | Son(including step-son) |

| 4 | Son`s wife |

| 5 | Daughter |

| 6 | Daughter`s husband |

| 7 | Brother(including step-brother) |

| 8 | Sister(including step sisters) |

| Relationship | Sec-2(41) of the income tax act | Sec-56(2) –gift | Sec-2(77) –foreign exchange management act |

| Spouse

| Yes | Yes | Yes |

| Parents( father/mother) | Yes | Yes | Yes |

| Brother /sisters | Yes | Yes | Yes |

| Son/daughter | Yes | Yes | Yes |

| Spouse of brother/sister | No | Yes | No |

| Spouse of son/daughter | No | Yes | Yes |

| Parent`s brother/sisters and their spouse | No | Yes | No

|

| Spouse`s brother /sister and their spouse | No | Yes | No |

| Grand-Parents and Grand Children | Yes | Yes | No |

| Spouse of Grand- Children | No | Yes | No |

| Great-Grand-Parents and Great-Grand- Children | Yes | Yes | No |

| Spouse’s Parents, Grand-Parents and Great-Grand- Parents | No | Yes | no |

The comparison graph of the definition of a relative under the acts referred to above is as follows:

| S. No. | Relative | GST Act | IBC Act | Companies Act | Accounting Standard | Income Tax Act | ||

| 2(77) | AS -18 | Ind AS -24 | 2(41) | 56(2)(vii) | ||||

| 1 | Grandson | Not Covered | Covered (Lineal Descendant) | Not Covered | Not Covered | Not Covered | Covered (Lineal Descendant) | Covered (Lineal Descendant) |

| 2 | Grand Daughter | Not Covered | Covered (Lineal Descendant) | Not Covered | Not Covered | Not Covered | Covered (Lineal Descendant) | Covered (Lineal Descendant) |

| 3 | Grand Father | Not Covered | Covered (Lineal Ascendant) | Not Covered | Not Covered | Not Covered | Covered (Lineal Ascendant) | Covered (Lineal Ascendant) |

| 4 | Grand Mother | Not Covered | Covered (Lineal Ascendant) | Not Covered | Not Covered | Not Covered | Covered (Lineal Ascendant) | Covered (Lineal Ascendant) |

| 5 | Father | Covered (If dependent) | Covered (Lineal Ascendant) | Covered | Covered | Not Covered | Covered (Lineal Ascendant) | Covered (Lineal Ascendant) |

| 6 | Step Father | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 7 | Mother | Covered (If dependent) | Covered (Lineal Ascendant) | Covered | Covered | Not Covered | Covered (Lineal Ascendant) | Covered (Lineal Ascendant) |

| 8 | Son | Covered | Covered (Lineal Descendant) | Covered | Covered | Not Covered | Covered (Lineal Descendant) | Covered (Lineal Descendant) |

| 9 | Daughter | Covered | Covered (Lineal Descendant) | Covered | Covered | Not Covered | Covered (Lineal Descendant) | Covered (Lineal Descendant) |

| 10 | Step Son | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 11 | Brother | Covered (If dependent) | Covered | Covered | Covered | Not Covered | Covered | Covered |

| 12 | Step Daughter | Not Covered | Not Covered | Not Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 13 | Step Mother | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 14 | Step Sister | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 15 | Son’s Wife | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 16 | Sister | Covered (If dependent) | Covered | Covered | Covered | Not Covered | Covered | Covered |

| 17 | Step Brother | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 18 | Husband/ Wife/ Spouse | Covered | Covered | Covered | Covered | Covered | Covered | Covered |

| 19 | Daughter’s Husband | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 21 | Member of a HUF | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 22 | Spouse’s Brother/Sister | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 23 | Liner Ascendant/ Descendant of Spouse (Including their Spouse) | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 24 | Spouse of Liner Descendant | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 25 | Spouse of Liner Ascendant | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 26 | Spouse of Brother/ Sister of the Individual | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 27 | Spouse of Spouse’s Brother/ Sister | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 28 | Spouse of parent’s Brother Sister | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 29 | Parent’s Brother Sister | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 30 | Dependent of Individual/ Spouse | Not Covered | Not Covered | Not Covered | Not Covered | Covered | Not Covered | Not Covered |

Related Persons as specified in GST law Regulatory Framework

Popular Blogs

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}