Page Contents

(Rupesh Kumar Gupta vs. PNB (NCLAT), 2020)

(Ashish Kumar vs. Vinod Kumar Pukhraj Ambavat, 2020)

(Vivek Jha vs. Daimler Financial Services India, 2020)

(Ishrat Ali vs. Cosmos Cooperative Bank Ltd. 2020)

(Yogesh Kr. Jashwantlal Thakkar vs. IOB, 2020)

(Ishrat Ali vs. Cosmos Cooperative Bank Ltd., 2020)

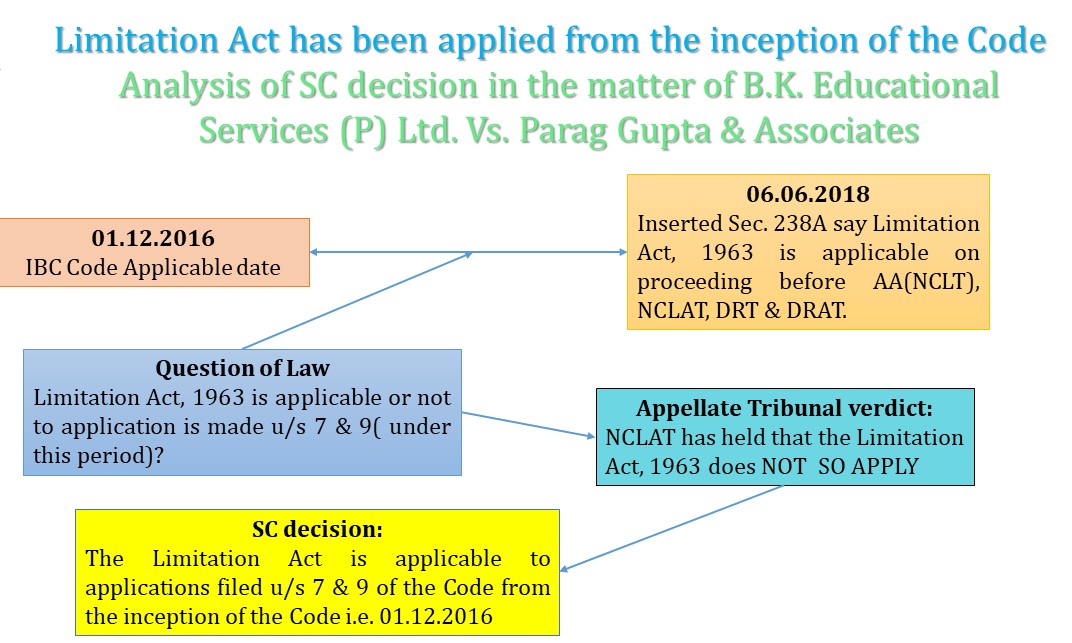

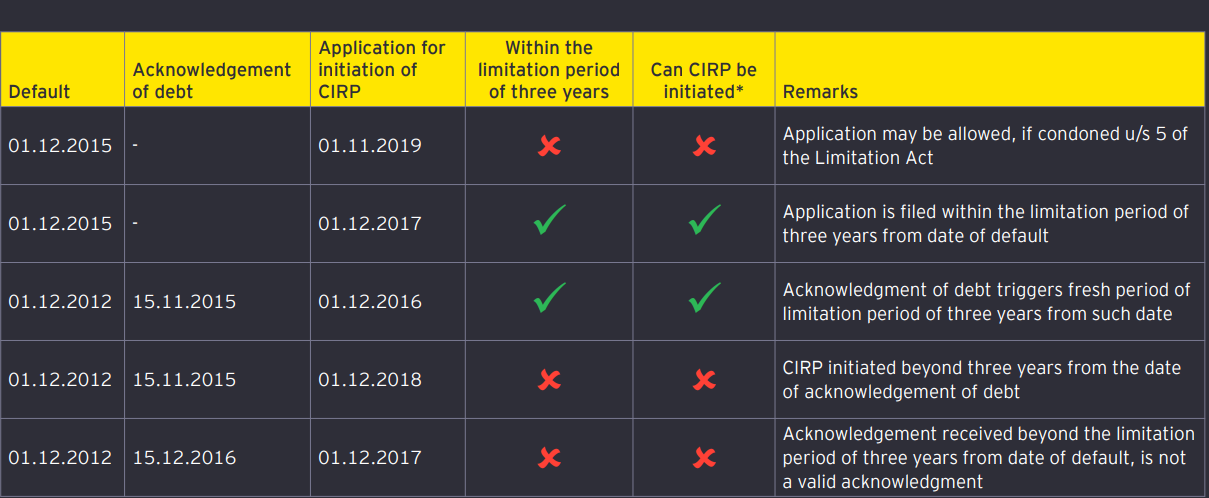

(Supreme Court in B.K. Educational Services, Jignesh Shah, Gaurav Hargovindbhai Dave, Babulal Vardhaji Gurjar)

(NCLAT in B.K. Educational Services vs. Parag Gupta)

Although the limitation Act does not extinguish a right would be a time-barred claim filed by the Financial Creditor/Operational Creditors be allowed during the Corporate Insolvency Resolution Process? If yes, is it not a matter of granting a new lease of life to a time-barred claim?

| S. No. | SARFAESI (Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest) Act, 2002, | |

| 1 | Narasimham Committee I and II and Andhyarujina Committee | SARFAESI Act, 2002 |

| 2 | Applicability | Whole of India |

| 3 | Net owed Funds of ARC | Not less than 2 crores |

| 4 | ARC to make application to RBI for Registration | within 6 months from the commencement |

| 5 | Sponsor | Holding not less than 10% of the paid up capital of the ARC |

| 6 | Appeal by ARC | 30 Days |

| 7 | In case of Joint Financing | Action only when creditor holding 60% of amount outstanding agrees |

| 8 | If dues are not fully satisfied from sale of secured assets | Creditor can then proceed against borrower by applying to DRT |

| 9 | What is the time limit within which Chief Metropolitan Magistrate or District Magistrate shall pass an order after receipt of the affidavit from the authorised officer of the secured creditor | Within 30 days of receipt of application and within such further period not exceeding in aggregate 60 days |

| 10 | Taking over of the management of business of a borrower by an asset reconstruction company | Section 9(a) |

| 11 | Taking over of the management of business of a borrower by a Secured Creditor | Section 13(4)(b) |

| 12 | Appeal to DRT by person aggrieved by action of creditor | 45 Days |

| 13 | DRT must dispose of the application filed under Section 17 | Within 60 days of the application extension of not more than 4 months |

| 14 | If borrower resides in J&K | Court of District Judge in that State (where borrower resides) |

| 15 | Appellate Tribunal for borrower in J&K | High Court |

| 16 | Time limit for validity of Notice of Caveat | 90 days from date of lodgment |

| 17 | CG power delegate power for establishment of Central Registry | RBI |

| 18 | Central Register shall not record particulars of transactions relating to | Extinguishment of security interest |

| 19 | Whi is responsible for furnishing information on modification and satisfaction of security interest | ARC or Secured Creditor |

| 20 | Central Registrar be intimated regarding satisfaction of security interest | 30 days from the date of such payment or satisfaction |

| 21 | If a person contravenes or abates contravention of any provision of the Act | Imprisonment for a term which may extend to one year or with fine or both |

| 22 | Time limit within which appeal against penalties can be made | 30 days from the date on which such order was passed |

| 23 | Appeal by ARC for cancellation of Registration Certificate | 30 days to Central Government (Ministry of Finance) |

| 24 | Who can cancel the ARC Registration | RBI |

| 25 | An Asset Reconstruction company Works as | Agent, manager & Receiver |

| 26 | CERSAI | Central Registry of Securitisation Asset Reconstruction and Security Interest (CERSAI) |

| 27 | Chg in Management or Takeover | If o/s more than 25 crs |

| 28 | If any person contravenes or attempts to contravene the provisions of this Act, he shall be punishable with– | Imprisonment which may extend to 1 year and Fine |

| 29 | Where any ARC or any person fails to comply with any direction issued by the RBI under this Act, penalty is imposed— | Not exceeding Rs. 1 crore or twice the amount involved in such failure, whichever is more |

| 30 | penalty imposed under section 30A shall be payable within a period of | 30 Days |

| 31 | If the ARC fails to comply with the directions issued by RBI? | 5 lakhs |

Popular blog:-

India has consistently maintained that the power to enact laws rests exclusively with its Parliament, acting within the framework of… Read More

Alternative (lower) tax regimes are available to assessees other than individuals/HUFs under the Income Tax Act. What does it mean?… Read More

ITR Filing Assessment Year 2026-27: Due Dates, New ITR Changes, Revised Return Rules & Compliance Guide The due dates for… Read More

Tax Audit at a Glance: Important Points for Futures & Options Traders Income Tax Treatment of Futures & Options Traders… Read More

Common Misconception of Crypto taxation in India Crypto Futures Contracts A crypto futures contract is a legal agreement between two… Read More

HRA Exemption under Old Tax Regime: New Rules Effective from 1 April 2026 Salaried Employees & HRA: New Rules Effective… Read More

{kind=link}

{kind=link}

{kind=link}