- Central Board of Direct Taxes has issued the notification on Procedure for registration and submission of SFT. Procedure for registration and submission of statement of financial transactions (SFT) as per section 285BA of Income-tax Act, 1961 read with Rule 114E of Income-tax Rules, 1962 has been notified by Central Board of Direct Taxes vide notification number Notification No. 3 of 2018 dated5th April 2018.

- Any person who is liable for audit under section 44AB of the Act and Receipt of cash payment exceeding two lakh rupees for sale, by any person, of goods or services of any nature – Make Sure your Statement of Financial Transactions (SFT) in Form 61A for the financial year 2016-2017 is to be filled by you till the May 31st, 2017

- Taxpayers who are liable for audit under section 44AB is a new inclusion who are liable for reporting the transactions from the financial year 2016-17 onwards.

- This will create a huge database for the government to do an effective cleaning up of the parallel economy.

Specified financial transactions (SFT)

- The CBDT in its press release dated 22.12.2016 has clarified that besides its Notification No.91/2016 dated 06.10.2016 that the aggregate of cash receipt during the year is not the benchmark for reporting.

- In other words, the requirement under SFT reporting is receipt of cash payment exceeding Rs.2 lakhs or more for sale of goods or services per transaction.

- Every person listed in section 285BA(1) is under an obligation to furnish a periodic statement of specified financial transactions (ISFT) as prescribed under the Income Tax Rules. Rule 114E of the Income Tax Rules, as amended w.e.f. 01.04.16, specifies the nature and value of reportable transactions, periodicity of furnishing of SFT, the format of SFT, etc.

- In order to reduce the generation and circulation of domestic black money, the Finance Act 2017 has imposed a prohibition on receipt of cash payments of rupees Two lakhs and above under new section 269ST, applicable w.e.f. 01.04.2017.

- Any contravention of the aforesaid provision would invite penalty on the recipient under Section 271DA which shall be equivalent to the amount of cash received. However, there would be no penalty if there is a good and sufficient reason for contravention of such provision.

High-value transactions

- To keep a watch on high-value transactions undertaken by the taxpayer, the Income-Tax law has framed the new concept of furnishing of Statement of Financial Transactions (SFT) in Form No 61A. It has replaced earlier annual information return reporting.

- Business assesses liable under tax audit, various financial institutions and professionals will have to report a slew of high-value transactions such as cash deposit, credit card payments, share sale, property deals, debentures, and mutual fund units among others.

- All these transactions are to be reported in a separate statement which will be Statement of Financial transactions (SFT).

- As far as the sale of goods or services is concerned, it would be interesting to analyze how these two types of machinery are going to supplement each other.

Rule 114E: Furnishing of statement of financial transaction: [w.e.f . 01.04.16]

Rule 114E. (1) The statement of financial transaction required to be furnished under Section (1) of section 285BA of the Act shall be furnished in respect of a financial year in Form No. 61A and shall be verified in the manner indicated therein.

(2) The statement referred to above shall be furnished by every person mentioned in column (3) of the Table below in respect of all the transactions of nature and value specified in the corresponding entry in column (2) of the said Table in accordance with the provisions of sub-rule (3), which are registered or recorded by him on or after the 1st day of April 2016, namely:—

| No.* | Nature and value of transaction | Reporting person |

| (1) | (2) | (3) |

| 10 | Purchase or sale by any person of immovable property for an amount of thirty lakh rupees or more or valued by the stamp valuation authority referred to in section 50C of the Act at thirty lakh rupees or more. | Inspector-General appointed under section 3 of the Registration Act, 1908 or Registrar or Sub-Registrar appointed under section 6 of that Act. |

| 11. | Receipt of cash payment exceeding two lakh rupees for sale, by any person, of goods or services of any nature (other than those specified at Sl. Nos. 1 to 10 of this rule, if any.) | Any person who is liable for audit under section 44AB of the Act. |

* Only items relevant to the discussion of this article are listed.

(3) The reporting person mentioned in column (3) of the Table under sub-rule (2) (other than the person at Sl. No. 10 and Sl. No. 11 w.e.f. 06.10.16)** shall, while aggregating the amounts for determining the threshold amount for reporting in respect of any person as specified in column (2) of the said Table,—

| (a) | | take into account all the accounts of the same nature as specified in column (2) of the said Table maintained in respect of that person during the financial year; |

| (b) | | aggregate all the transactions of the same nature as specified in column (2) of the said Table recorded in respect of that person during the financial year; |

| (c) | | attribute the entire value of the transaction or the aggregated value of all the transactions to all the persons, in a case where the account is maintained or transaction, is recorded in the name of more than one person; |

| (d) | | apply the threshold limit separately to deposits and withdrawals in respect of transaction specified in item (c) under column (2), against Sl. No. 1 of the said Table. |

(5) The statement of financial transactions referred to in sub-rule (1) in Form 61A shall be furnished on or before the 31st May, immediately following the financial year in which the transaction is registered or recorded.

** As per Notification No. 91/2016

(ALERT: As per sec. 285BA, r.w.r. 114E(6)(a) every reporting person mentioned in column (3) of the table under sub-rule (2) of rule 114E should obtain a registration number from IT Department for the purpose of filing Statement of Financial Transactions [SFT] in Form No. 61A.

Central Board of Direct Taxes vide Notification No. 13 of 2016, dt. 30.12.16 explained the procedure for Registration and generation of ITD registered Entity Identification Number [ITDREIN])

Issues:

| (i) | | Reporting in Form 61A [in case of transaction No.11 mentioned in Rule 114E(2) above] applies only to 44AB audit cases. |

| (ii) | | The norms of aggregation contained in sub-rule 3 of Rule 114E have been amended vide CBDT’s Notification No. 91/2016, dated 6th October 2016; clearly indicating that the said transactions do not require aggregation and the reporting requirement under Statement of Financial Transactions [SFT] for this purpose is on receipt of cash payment exceeding Rupees Two Lakh for sale of goods or services PER TRANSACTION. [Central Board of Direct Taxes –press release dated 22.12.16] |

Central Board of Direct Taxes, vide Notification No. 112/2022 dated 07 Oct 2022, amends Rule 114F(5) i.e. definition of ‘non-reporting financial institution’;

The amendment specifies that:

(i) a local bank, and

(ii) the financial institution with a local client base,

(iii) a financial institution with only low-value accounts qualify as a non reporting financial institution if there is any U.S. reportable account;

Section 269ST inserted by the F.A. 2017:

Under Section 269ST. No person shall receive an amount of two lakh rupees or more—

| (a) | | in aggregate from a person in a day; or |

| (b) | | with respect of a single transaction; or |

| (c) | | in respect of transactions relating to one event or occasion from a person, otherwise than by an account payee cheque or an account-payee bank draft or use of electronic clearing system through a bank account: |

Comparison:

- On one hand, any person who is liable for audit under section 44AB of the Act is liable to report, on yearly basis, all his transactions involving receipt of cash payment exceeding two lakh rupees for sale of goods or services of any nature in Form 61A electronically.

- other hand, as per newly introduced section 269ST, there is an equivalent penalty on receipt of cash payments of rupees Two lakhs or above, in the circumstances as specified in clause (a) to (c) of S. 269ST(1)!!

- Thus, these two types of machinery of the Act are clearly supporting each other for effective implementation of the legislative intent to curb black money through restrictions on cash transactions above specified limits. This is further explained below by way of the comparative chart in the context of transactions of sale of goods or services.

5.1 Applicability of Rule 114E and S. 269ST in sales transactions

| Sr. No. | Nature of Transaction | S. 269 ST w.e.f. 01.04.2017 applicable | Yearly Reporting in Form 61A w.e.f. (01.04.16) |

| (1) | (2) | (3) | (4) |

| 1 | Single Bill below Rs. 2,00,000/-. | | |

| 1.1 | – Full Recovery in cash | NO | NO |

| 1.2 | – Part recovery in cash | NO | NO |

| 1.3 | – Full recovery by Cheque | NO | NO |

| 2 | Single Bill exceeding Rs. 2,00,000/-. | | |

| 2.1 | – Full Recovery in cash on a single occasion | YES | YES |

| 2.2 | – Part recovery in cash below Rs. 2 Lacs | NO | NO |

| 2.3 | -Part recovery in cash above Rs. 2 Lacs on a single occasion | YES | YES |

| 2.4 | Part recovery in cash above Rs. 2 Lacs on multiple occasions but not a single receipt exceeds Rs. 2 Lacs | YES | NO |

| 2.5 | – Full recovery by Cheque | NO | NO |

| 3 | Multiple Bills issued during the year to the same person and the aggregate bill amount exceeds Rs. 2,00,000/-. (However, not even a single bill exceeds Rs. 2 Lacs) | | |

| 3.1 | – Full Recovery in cash on single occasion | YES | YES |

| 3.2 | – Part recovery in cash above Rs. 2 Lacs on multiple occasions (on different days) but not a single receipt exceeds Rs. 2 Lacs | NO | NO |

| 3.3 | – Part recovery in cash above Rs. 2 Lacs on multiple occasions (IN SINGLE DAY) but not a single receipt exceeds Rs. 2 Lacs | YES | NO* |

| 3.4 | – Part recovery in cash above Rs. 2 Lacs on a single occasion | YES | YES |

| 3.5 | – Full recovery by Cheque | NO | NO |

Assumptions:

| – | | Multiple bills issued to a person do NOT relate to one event or occasion |

| – | | ‘On single occasion’ means, at a moment in a day |

*Refer to CBDT’s press release, dt. 22.12.16 as discussed above

NOTE: In case of –

| – | | multiple Bills issued during the year to the same person and the aggregate bill amount exceeds Rs. 2,00,000/-; and |

| – | | One or more bills exceed Rs. 2 Lakh, |

- The assessee has to establish a one-to-one correlation in books of account between bills issued and cash receipts from time to time, so as to check the applicability of section 269ST.

- Therefore, dealers should specifically mention on every cash receipt the sale Bill No. and the date against which the cash is accepted.

Key points for understanding the Statement of Financial reporting

- The requirement of filing Annual Information Return (AIR) is now being replaced by Statement of Financial Transactions (SFT).

- SFTs have to be filed in separate form and not along with Income Tax (IT) returns.

- The form for SFT reporting is Form 61A. It consists of 4 parts.

- Due date for filing the first SFT for the financial year 2016-2017 is May 31, 2017.

- It is applicable for all the business taxpayers liable for tax audits, professionals, and financial institutions.

- Entities that will report are banks, professionals, fund houses, forex dealers, post office, nidhis, non-banking finance companies, property registrars, companies issuing bonds and debentures, and listed companies buying back shares from specific persons.

- Changes have created new classes of first-time filers who have to file SFT of specified transactions for FY 2016-17.

- Salaried individuals are not required to file for a statement of financial transactions (SFT)

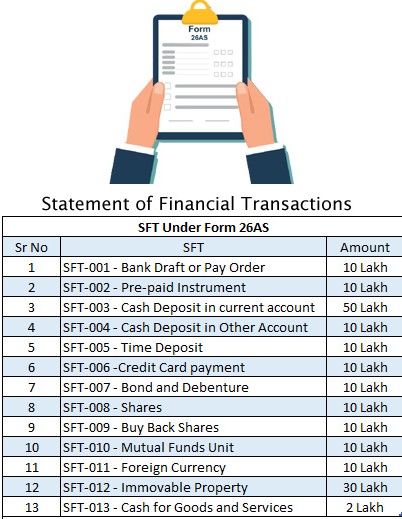

- The nature of transactions includes cash payment for the purchase of demand drafts or pay orders of Rs 10 lakh or more in a year; cash payment of Rs 10 lakh or more for purchase of prepaid RBI instruments, cash deposit or withdrawal of Rs 50 lakh or more from the current account; one-time deposit of Rs 10 lakh or more with banks, nidhis, NBFCs and post offices; payment of Rs 1 lakh or more in cash and Rs 10 lakh or more by other modes against credit card bill issued to a person during the year; and property registrars for deals worth Rs 30 lakh or more.

Deadline of Filling of Statement of Financial Transactions due date

- Last date for filing the SFT for Financial Year 2023-24 is May 31st, 2024.

- Statement of Financial transaction is required to be filed in Form No. 61A for transactions entered with third parties.

- While reporting the transaction in Form 61 ( Statement of Financial transaction) a business taxpayer will have to take into account all the accounts of the same nature maintained in respect of a person during a financial year; also, while attributing the entire value of the transactions to all the persons in cases where the account is maintained or transactions recorded in the name of more than one person.

- The penalty for the delay is Rs. 1000 per day.

- Filing of inaccurate information will attract a penalty of Rs 50,000.

We look forward for your valuable comment:

FOR FURTHER QUERIES CONTACT US: W: www.carajput.com E: singh@carajput.com T: 9-555-555-480

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}