Page Contents

GST is the indirect tax that imposed on the services and goods on the basis of the primary of value addition. Hence, the imposing of the tax is totally based on the value addition at the single stage of the chain of supply until the finished product reached the final consumer. In this kind of system of tax, to invalidate the cascading effect on the tax, it exists a way to set of taxes paid acquisition of the basic material, parts, services, plant and machinery, consumables, and so on. It used for manufacturing goods and services. The part used to of set to the tax liability is known as the input tax credit. We cover the concept of the Input under the GST in detail.

In the GST, each person that comes under the supply chain that comes in the process of controlling, getting the GST tax, and remitting the amount collected have to complete the GST registration. Input tax credits help to avoid the double taxing and the cascading effect of the and Input tax credit is given to adjust the tax paid on the acquisition of the basic materials, consumables and the services and goods that helped in the producing and supply and the sales of the goods and services. After using the ITCM, organizations are able to net neutrality in the prevalence of the tax and makes sure that input tax part doesn’t invade into the cost of the supply of services and goods or cost of the creating.

A person who has the GST registration can claim the ITC on the basis of the right documents and filling the form of the GST- returns. If you want to claim the ITC then you must have the following documents ready.

Further, the below conditions are also important to fulfill for claiming the ITC.

In the GST, the ITP is not accessible regarding the below services or goods:

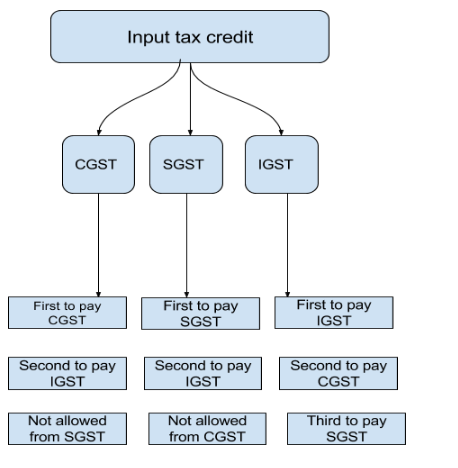

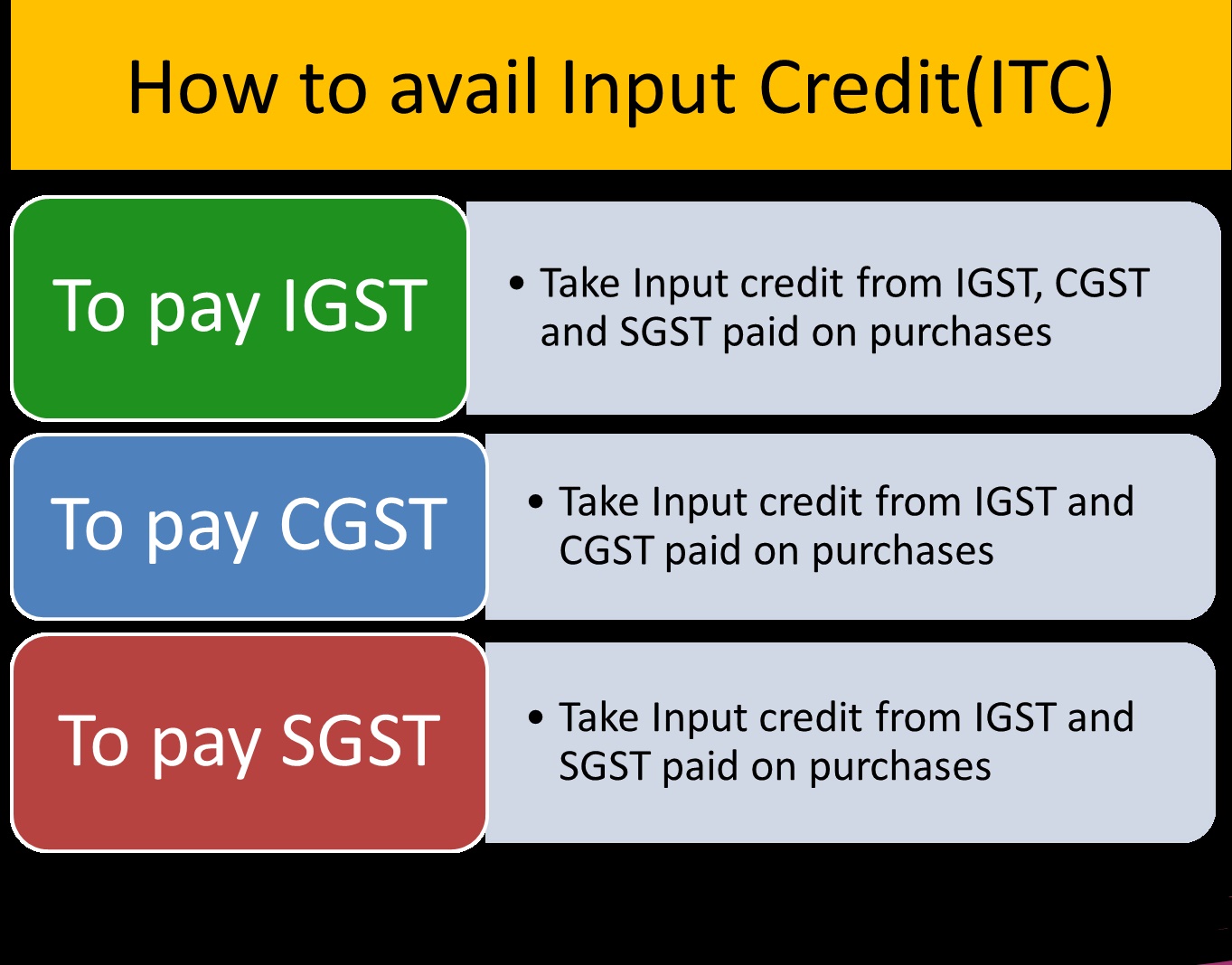

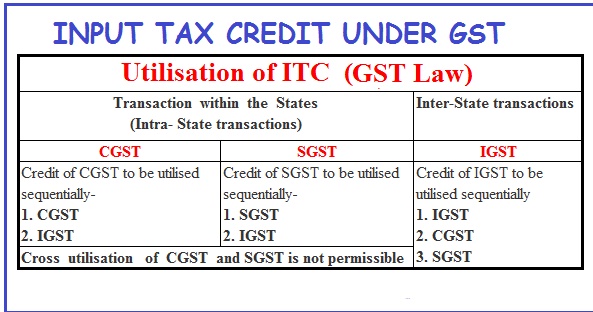

The SGST and CGST ITC will be attention to the electronic credit books of the person or taxpayer which is organized by the GST Network. The price of the ITC in the electronic credit books which can be used for the payment of the CGST and the remaining price, if any, can be used for the payment of the IGST. The price of the ITC on the account of the CGST on the EC book can’t be used for the payment of the SGST.

In addition, it’s required to note the amount of the output tax that can be created by using the ITC. Any amount on the account of interest and penalty is important to be created out of the price available in the computerized cash books of the person or taxpayer.

A simple guide to CGST, SGST, and IGST, if you need to understand the difference.

A simple guide to electronic cash ledger and procedure for making GST payment.

(a) he is in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other tax paying documents as may be prescribed;

(aa) the details of the invoice or debit note referred to in clause (a) has been furnished by the supplier in the statement of outward supplies and such details have been communicated to the recipient of such invoice or debit note in the manner specified under section 37;‖. (PROPOSED VIDE THE FINANCE BILL, 2021)

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}