- Income Tax Return is a form used to file income taxes with the Income Tax Department. Income tax is a tax on an individual’s income imposed by the Central Government.

- Each citizen is responsible for filing income tax. These income reports are verified by the IT department, and if any excess amount is paid, the department will repay the amount to the bank account of the assessee. In order to avoid a penalty, all entities must submit taxes on time.

- The form containing income and tax information paid to an assessee is called the Return on Income Tax. The Indian Income Tax Department has different forms like ITR 1, ITR 2, ITR 3, ITR 4S, ITR 5, ITR 6, and ITR 7.

- RJA provides the best service and assists you in completing the correct form on time.

Income Tax Return Filing Service:

- Each year, there are numerous changes to Income Tax that affect your tax return. It is critical to file a correct income tax return in order to avoid receiving an unexpected tax notice.

- Our CA Expert will ensure that your return is done flawlessly and that all needed disclosures are included in your return, allowing you to relax and enjoy your weekends.

Things to keep in mind when preparing your tax return:

- Do not put off filing the IT return until the last minute.

- Always assemble all of the documents you’ll need to file an

- Select the appropriate IT return form. This is critical.

Reasons To File Your ITR Even If Your Income Is Not Taxable

Income Tax filing is a compulsory need for anyone with a taxable income of INR 2,50,000/- & above. It is also Compulsory for cases below :

- Expenditure INR 2,00,000/- & above in foreign travel. Or

- In case you are an individual who has paid an electricity bill over INR 1,00,000/- or

- Total deposits in accounts/ current account more than Rs 1 Cr.

Benefits of IT Returns:

However, reasons to file ITR even if income is not taxable. it makes sense to file ITR’s for many benefits like below mention. Benefits of It return are as follows:

- Loans: Bank loans, such as education loans, vehicle loans, and personal loans, are simple to obtain because they only require the previous three years’ IT returns.

- Applying for a Visa: Because immigration centres scrutinize many documents, IT returns proofs are required for visa applications.

- Keep away from penalties: Non-filing of income tax returns will result in significant penalties; therefore, it is always preferable to file in order to avoid legal ramifications.

- Meets the requirement as proof of income

- Applying for home loan/ a vehicle or other financial instruments

- Claiming refunds

- Claiming losses

IT Tax Refunds and Taxpayers’ Responsibility:

When a taxpayer pays more tax than his or her actual tax liability, he or she becomes eligible for a tax refund. To be eligible for the refund, the taxpayer must have filed the returns by the due date.

The IT department usually sends notices to taxpayers to ensure that the filing process goes as smoothly as possible. Any loss on house property, depreciation, business loss, or any other type of loss that is not offset against income can be carried forward to subsequent years.

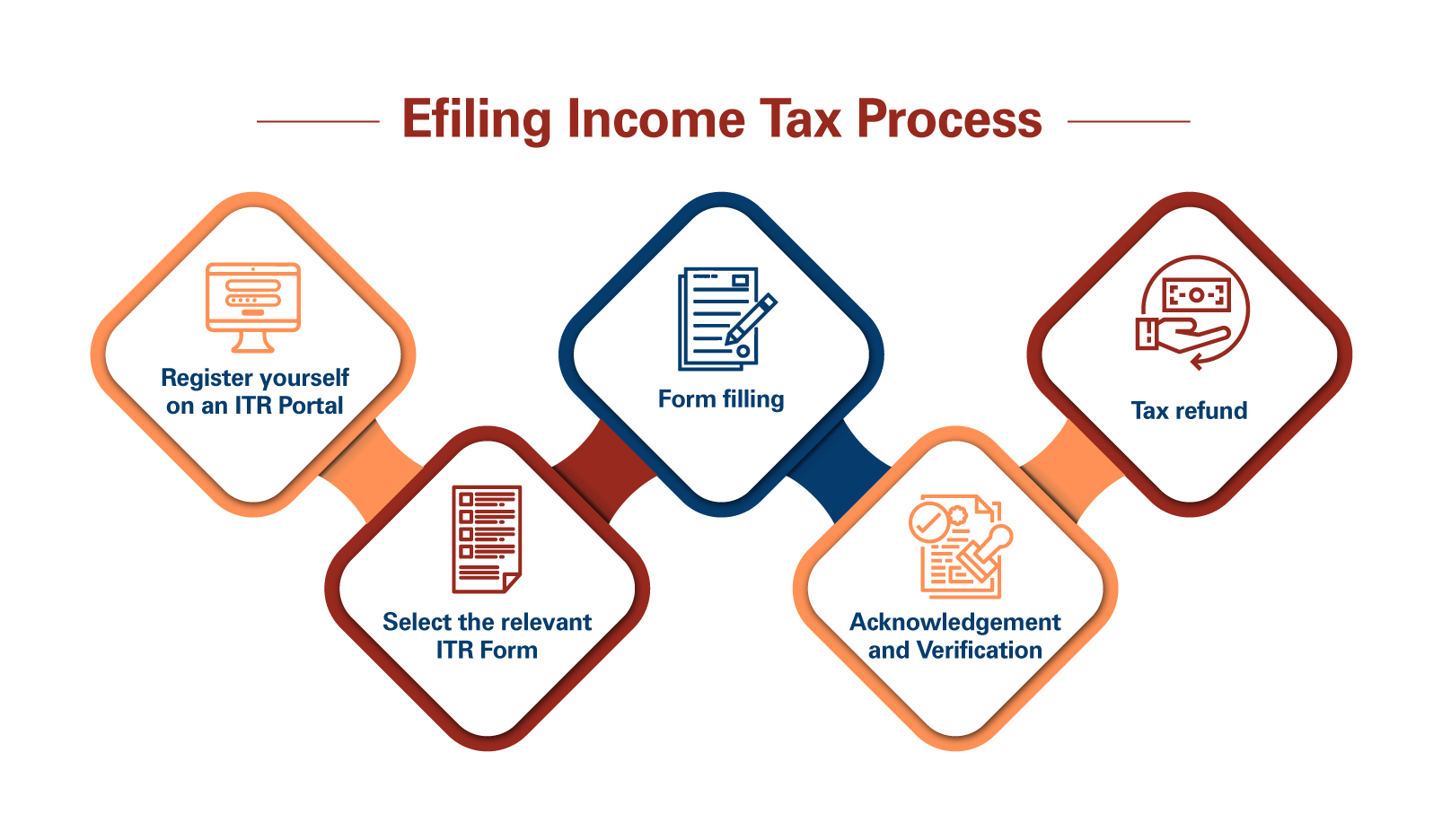

How do you file your tax return online?

A Detailed Procedure:

Gather all documents, such as bank statements, the previous year’s return, and Form 16, before filing your IT returns. Log on to www.incometax.gov.in

- Register using your PAN number. It serves as your identification.

- Form 26AS is available for viewing. It displays the amount of tax deducted by the employer. This amount should be reflected in the TDS on Form 16.

- Download the ITR Form that applies to your situation. Consult RJA if you don’t know which form to use.

- Fill out the entire form with the required information and then submit it.

- To find out how much tax you owe, click the Calculate Tax option.

- Pay the required tax, if applicable.

- On the tax return part of the form, fill in the details of the challan.

Filing deadlines for IT returns:

- A corporation or individual who is not subject to audit on July 31.

- 30 September: A firm or other entity that may be audited.

- Individuals and businesses must file late returns by March 31.

RJA suggests using Google Calendar to get early notice of due dates and file ITRs on time.

Acknowledgement of Income Tax Return:

When an ITR is filed, an acknowledgment slip is issued in duplicate. It includes information such as:

- Name

- Address

- Status

- Permanent Account Number

- A brief statement of taxable income

- Deductions

- Tax paid

- Verification

Who is required to file an income tax return?

- According to the Income Tax Department, the entities required to file IT returns on an annual basis are.

- Regardless of income or loss, every company, whether private limited, LLP, or partnership, is required to file IT returns.

- Individuals who receive income from mutual funds, bonds, stocks, fixed deposits, interest, house property, and so on.

- Individuals who receive income from charitable trusts, religious trusts, or from voluntary contributions.

- Individuals and businesses seeking tax refunds

- Salaried individuals with a gross income before deductions under sections 80C to 80U that exceeds the exemption limit

- Individuals with foreign income or assets, NRIs, and tech professionals on onsite deputation are all eligible.

- People who chose one job over another are also eligible.

For the purpose of filing a business tax return:

Every year, the IT Department of India requires all businesses operating throughout the country to file income taxes. TDS returns and advance taxes can be filed if required to ensure that the business complies with IT rules and regulations.

Filing a Tax Return for a Sole Proprietorship:

A proprietorship firm is led by a single individual known as the proprietor. Proprietorship is not a separate legal entity; the proprietor (business owner) and the business are the same. As a result, ITR filing for a proprietorship is identical to that of the proprietor.

Year after year, proprietors are required to file IT returns. The process is identical to that of filing an individual income tax return.

Filing requirements for sole proprietorship tax returns include:

Proprietors under the age of 60 with an annual income of more than Rs.2.5 lakh are required to file proprietorship tax returns. Owners who are over 60 but not over 80 years old and have a total income of more than Rs 3 lakhs are eligible.

If a proprietor’s total income exceeds Rs 5 lakhs, if he or she over 80 years must file an IT return.

Filing a tax return for a partnership firm:

All partnership firms are recognized as independent legal entities under the Income Tax Act and are subject to the same tax rates as LLPs and corporations established in India.

Filing a partnership firm’s tax return is required:

Partnership firms must file IT returns regardless of profit or loss. A NIL income tax return should be filed within the deadline if the company has been commercially inactive and has no reported income.

Filing of LLP Tax Returns:

All LLPs, or Limited Liability Partnerships, are considered separate legal entities, and their income tax rates are the same as for all Indian firms. The Income Tax Act mandates that all LLPs file their tax returns, regardless of whether they made a profit or a loss that year. A NIL income tax must be filed as soon as possible if the LLP has seen no business activity or registered income.

Filing of Company Tax Returns:

The Ministry of Corporate Affairs registers all forms of business formations, such as a private limited company, a limited company, a limited liability partnership, and a one-person corporation. The Income Tax Act requires all such businesses to file IT returns on a regular basis.

Filing of corporate tax returns is required:

Any company operating on Indian land that is registered with the government of India is required to submit its filed IT returns. This is also true for organizations that have been idle for a long time, with no commercial transactions and no income or expenses recorded.

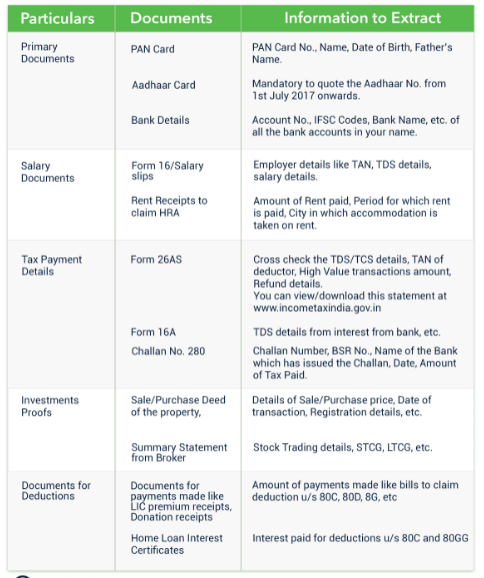

Required documents for ITR filling in India:

- Bank statements

- Proof of investments

- D.S. Certificates in Form 16 or 16A as applicable

- Purchase and selling documents for investments/assets.

- Tax challans, such as advance tax or self-assessment tax challans.

- A copy of the filed PAN application and its acknowledgment if the PAN is applied but not received.

- If you haven’t already applied for a PAN, you’ll need a completed PAN application form as well as two passport-size pictures.

- A copy of the audit report, balance sheet, trading, profit and loss account, and personal account of the proprietor or partners for firms.

- When no regular books are kept, a statement of receipts and payments is made.

- To substantiate claimed deductions, save receipts for payments of insurance premiums, provident purchases of NSCs, new equity shares, mutual funds, NSS, contributions, and so on.

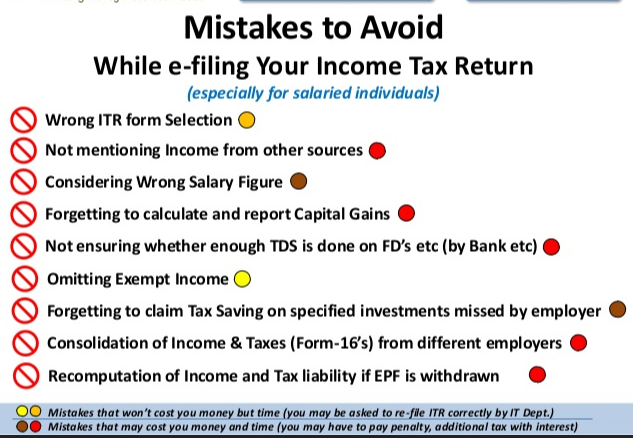

Common Errors When Filing Your Income Tax Return:

The following are some of the most typical mistakes to avoid while filing an ITR.

- The incorrect form was selected: The relevant ITR form should be chosen based on the taxpayer’s income and category.

- The Wrong Assessment Year was selected: The correct assessment year must be specified when filing an ITR; otherwise, it may result in double taxation and penalties.

- Details were entered incorrectly: Personal information of the assessee, such as name, address, e-mail address, cellphone number, PAN, and date of birth, must be verified while filing an ITR.

- Not disclosing the entire source of income : Regardless of whether the income is taxable or exempt, any income generated from sources other than the principal reference must be fully disclosed.

- TDS and Form 26AS are not reconciled: Forms 26AS and 16 must be reconciled.

- Return verification: Following the filing of an income tax return, it must be e-verified via net-banking or the EVC process on a mobile number and via email.

Non-filing of an income tax return carries a penalty:

- If a taxpayer fails to file an ITR on time, there are certain penalties that apply. On the late payment of income tax, a penalty is imposed. The highest penalty amount is Rs 10,000/-.

- Do you want to enjoy the benefits of these perks but are having difficulty filing it on your own? Rajput Jain & Associates resolves all of these issues by accurately filing your income tax return and helping you in receiving the maximum tax refund possible. You ca Hire Chartered Accountants to help you file your ITR.

Also Read :

F&Q on NRI Income Tax Compliance (Help Centre)

Key Provision for NRI Taxation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}