Page Contents

| Rate | Condition | Nature of service |

| 5% | No ITC on goods and services | Transportation of goods by the road where consignment note is issued (i.e. GTA services) (RCM) |

| 5% | No ITC on goods. ITC can be availed only on vessels, ships, etc. | Transportation of goods by vessel |

| 5% | ITC on goods can’t be utilised | Transportation of goods by rail |

| 12% | ITC eligible | Transportation of goods by road where consignment note is issued (i.e. GTA services) (Forward Charge) |

| 12% | ITC eligible | Multimodal transportation of goods |

| 12% | ITC can be availed | Transport of goods in containers by rail by any person other than Indian Railways. |

| 18% | ITC eligible | Other supporting, incidental or ancillary services |

| 18% | ITC eligible | Loading, unloading, storage and warehousing/cargo handling services |

| S. No | Nature of service |

| 1 | The hiring of the motor vehicle to GTA as means for transportation of goods |

| 2 | GTA services provided to Government and its departments |

| 3 | Transportation of specified goods by rails like agriculture produce, milk, salt, and food grain including flours, pulses, and rice |

| 4 | Services provided by a goods transport agency to an unregistered person other than a specified category like the factory, Body corporate, etc. |

| 5 | Transportation of goods by the road where consignment note is not issued |

| 6 | Services by way of transportation of goods by a vessel from India to Foreign Country |

| 7 | Transportation of goods by an aircraft or vessel from the customs station of clearance in India to a place outside India |

| 8 | Specific exemptions in relation to loading, unloading, storage, and warehousing of rice & storage & warehousing of cereals, pulses, fruits, nuts, vegetables, etc. |

| 9 | Services by way of transportation of goods by an aircraft from a place outside India up to the customs station of clearance in India. |

| 10 | Transportation of specified goods by GTA like agriculture produce, milk, salt, and food grain including flours, pulses, and rice |

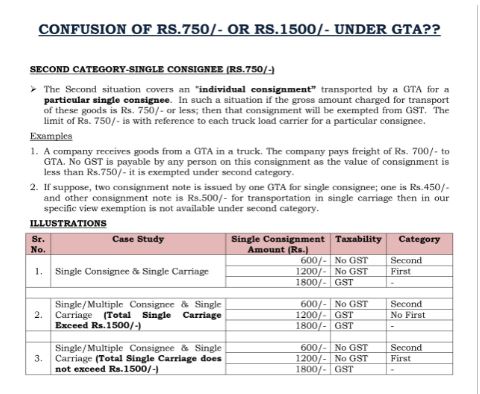

In case Goods, If consideration charged for the transportation of goods ON A CONSIGNMENT TRANSPORTED IN A SINGLE CARRIAGE does not exceed INR 1500/-

In Goods, if consideration charged for transportation of ALL SUCH GOODS FOR A SINGLE CONSIGNEE does not exceed INR 750/-

individual consignment covered in above said exemption means all goods transported by goods transport agency for “a consignee“

In contradistinction to this, fixing of exemption limit of INR 1500/- is not limited to the consignment to the individual consignee but it refers to consignments relatable to more than 1 consignee.

This would be our effort to describe the whole idea in a concise way. If you are also faced with a problem or confusion related to this matter, please feel free to contact the Rajput Jain and Associates team, and as an RJA team will assist you to resolve all your questions along with offering realistic solutions to your GST concerns!!!

FOR FURTHER QUERIES CONTACT US: W: www.carajput.com E: singh@carajput.com T: 9-555-555-460

Popular blog:

MCA Changes in Indian Company formation- 2026 A series of reforms measures put forth by the Ministry of Corporate Affairs… Read More

Complete Guide to Reverse Charge Mechanism (RCM) under GST Under Goods and Services, tax is generally paid by the supplier…But… Read More

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

{kind=link}

{kind=link}