GST Registration under GST?

GST Registration Cancellation & Revocation under GST-How & Why Its Need?

- The GST Dept has made big changes to its operational activities and innovative ways of reviewing corporation. To make you realise all these modifications, we are here with the GSTR 3B Factual information series, which discusses these all improvements.

- In this blog, we are talking about the first fact/consequence of not filing a return on time. Registration Notice of suspension on the grounds of Mismatch.

New Rule 21(2A) of the Goods and Services Tax Rules, 2017.

- The outward supply reflected in GSTR 1 & ITC as displayed in GSTR 2A is compared with the value reflected in GSTR 3B Return using the EDW-ADVAIT method.

- If there is indeed a substantial difference between the two figures, the GST officer has the power to suspend your Certificate Of registration and then send you a notice to explain the mechanisms set out in Rule 21(2A) in Form REG 31.

- The very worst part is that, unlike some other laws in which the convicted is given an opportunity to clarify his or her case before even being punished, the GST law allows officers to punish Business owners with suspension before giving an opportunity to clarify the mistake.

- The Govt is also on track to further develop sophisticated methods capable of identifying sequence disturbances with the power of AI and BI.

- The same kind of issues may arise with the late return filing.

What can/should I do about it?

- As day-to-day regulations become pretty strict, you must also impact the way you handle your business tax data.

- You need to use GST software that combines GSTR 2A, GSTR 1 and GSTR 3B at all moments and inform you of problems just as they occur.

- Your GST software needs to identify key ratios and red flags so that you can take action and identify mistakes at the front of the dept.

More read: Registration of GST under Goods and Service Act, 2017

GST Registration Cancellation under GST- Why & How?

- Cancellation of GST registration describes that the taxpayer will no longer be a GST registered person; they will no longer have to pay or collect the tax.

- Taxpayers who have previously registered under the GST Act may apply to cancel the registration of a GST at a certain time they feel compelled to close their business or in any other scenario.

- After the registration has been cancelled, the taxpayer is no longer required to pay tax or to collect tax from ordinary people.

- Consequences of GST registration cancellation: Registration under the GST is compulsory for certain companies. If GST registration is cancelled and business continues, it will result in a GST offence and big penalties will implement.

- Following Implications of cancellations of GST registration

- The taxpayer is unable to collect and could no longer pay GST;

- There would be no need for the taxpayer to file any GST return.

- Registration under the GST is mandatory for individual businesses. If GST registration is decided to cancel and business continues, it will result in a GST violation and heavy penance.

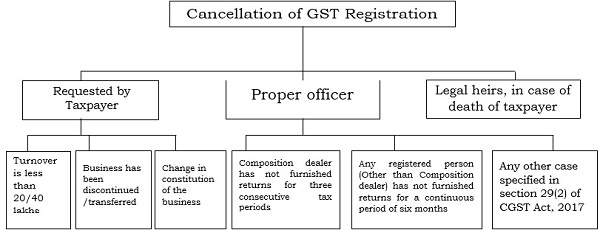

- Registration granted under the GST shall be cancelled for specified reasons. Cancellations may be made either by the dept or by the registered person or by personal representatives in the event of the death of the registered person.

- In the event of the cancellation of the registration by the department, provision has been made for the cancellation of the registration.

Also read : SOP for verification of Taxpayer who granted deemed registration

Cancellation of registration of the GST may be made by:

- Required by the taxpayer

- Migrated taxpayers:

- Any person who has been registered under the earlier indirect tax law like services tax etc had to migrate to the GST on a mandatory basis.

- For example, the VAT threshold for most states was 5 lakhs, when it is actually 20 lakhs for GST. However, make absolutely sure that you don’t seem to make inter-state supplies, as registration is mandatory for inter-state suppliers except for service providers.

- The request for cancellation, in the case of voluntary GST registrations, could be made without delay only after one year from the date of registration, e.g. Rs. 40 lakh or Rs. 10 lakh in certain states/union territories. • Such taxpayers had to make an application electronic means to the GST portal in FORM GST REG-29.

- Other than those of the migrated taxpayers

-

- The business has ceased.

- The business has been considered close, amalgamated, demolished or disposed of.

- The transferee must be registered; the transferor will cancel the registration if it ceases to exist.

- An instance of a change in the business example of the constitution; a private limited company has changed to a public limited company.

- By the appropriate GST Taxation officer: The tax officer may cancel the registration if:

-

- A taxpayer just hasn’t filed GSTR-1 because GSTR-3B has not been filed for more than 2 regular months.

- They are in violation of anti-profit making provisions.

- No business is carried out by the taxpayer from the declared place of business.

- Taxpayer issues invoices or invoices without the delivery of goods or services.

- Using ITC from electronic credit ledger to discharge more than 99 per cent of the tax liability for specified taxpayers with a total supply tax of a considerable amount of Rs. 50 lakh per month, with some deviations.

- By the Legal heirs to the taxpayer

-

- Prior to cancelling the registration, the officer would notify the person whose GST registration is subject to cancellation.

- Attested notification within seven working days from the date of service of such information as to why the GST registration is cancelled.

- The registered person may, within in the time stipulated, respond to the attested notice

What are the Consequences of cancellation of GST registration

- There is not required for furnishing any GST return by the Assessee.

- For Properitray concern businesses, GST Registration is mandatory. Business is running without GST Registration or GST registration is cancelled and organisation running a business still continued, which may result that an offence under GST law, & needed to face heavy penance will apply.

- The Assessee cannot collect & could not pay GST further period or anymore

- GST Registration once gets cancelled for specified reasons. That GST cancellation can either made by the GST dept or himself or the legal heirs/authorised in case of a registered person’s death.

- Once GST Registration has been cancelled by the GST dept, there is a specific provision for revocation of the registration cancellation.

Documents Required for Cancellation of GST Registration

- Reason for the GST cancellation

- Information & Details of stock of plant & machinery/capital goods

- ARN of latest GST return filing done

- GSTIN of the business entity

- Contact details of business entity (Mobile no. & Email id)

- GSTIN of transferee entity (in case business is transferred)

- Desired date of GST cancellation

- Aadhar and PAN & of Authorized signatory

- DSC in case of an LLP/company

- Information & Details of stock of semi-finished goods/finished goods/inputs

Forms for GST Registration cancellation

All of those who cannot follow the abovementioned procedure must submit an application for the cancellation to FORM GST REG 16. The legal heirs of the deceased taxpayer shall repeat the same process as the following.

- Application for cancellation must be made in FORM GST REG 16.

- The following information should be included in the FORM GST REG 16—

- Details of the inputs, semi-finished, finished goods held in stock on the date of cancellation of registration

- Liability on this

- Payment details.

- An order for cancellation under FORM GST REG-19 must be issued by the appropriate officer within thirty days from the date of application. The cancellation shall take effect from the date calculated by the officer and shall be notified to the taxable person.

Revocation for GST cancellation

What is the Revocation for GST cancellation?

- Revocation of the cancellation of GST Registration explained that the application form has been fully rectification done and that the GST Registration is still valid.

- This case can be applied only in case the GST Tax officer has forced to cancel the registration of a taxable person on his/her movement.

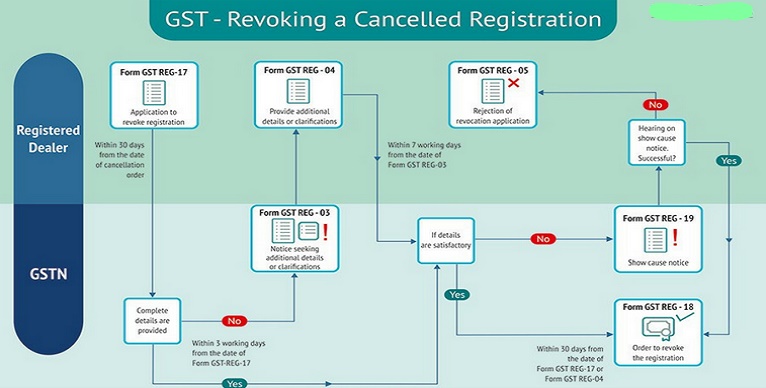

- Such a GST taxable person may again apply to the GST cancellation officer within 30 days from the date of the cancellation order.

When is the cancellation revocation applicable?

- This applies only if, on its own motion, the tax officer has cancelled the registration of a taxable person. Such taxable person may apply to the cancellation officer within 30 days from the date of the cancellation order.

Note: Application for revocation cannot be filed if the registration has been cancelled due to failed to submit returns. Such returns must be made in the first place along with the payment of all amounts of tax, interest and penalty due. Such returns must be made in the first place and all amounts of tax, interest and penalty due must be paid.

Procedure for Implement Revocation for GST cancellation

- A registered person may submit a request for cancellation in FORM GST REG-21 if his registration has been cancelled by the appropriate officer.

- It must be submitted to the Common Portal within thirty days from the date of the provider of the cancellation order.

- If the proper officer is satisfied, he may cancel the registration by order in FORM GST REG-22 within 30 days from the date of receipt of the application. Revocation of the cancellation of the registration must be recorded in writing.

- Proper officer may by order in FORM GST REG-05 reject the request for revocation and may convey the same with the applicant.

- Before rejecting the application, the competent authority must send a statement of cause in FORM GST REG–23 to show the applicant why the application must not be refused. The candidate must reply to FORM GST REG-24 within 7 working days of receipt of the notification service.

- Judgement of the appropriate officer shall be taken within thirty days from the date of receipt of the explanation from the application form in FORM GST REG-24.

Finally after receipt of the request for GST registration Revocation, in the form GST REG-21, if the Proper officer is completely comfortable with the reason/revocation of the GST Registration, the cancellation of the registration in the form FORM GST REG-22 shall be revoked.

After the receipt of Revocation Request

After the receipt of Revocation Request, in Form GST REG-21, if the officer is satisfied by the reason/ grounds for revocation of GST Registration, then he shall revoke the cancellation of registration in FORM GST REG-22

Be Caution: If you are a GST registered person who has a good deal and a stock in hand and by any error (due to a lack of consciousness of GST law) your GST number is cancelled.

it is recommended that before proceeding with the submission of any reply to the GST Officer, please ensure that you have sufficient knowledge of GST law or consult with the GST Expert even though, nowadays,

GST Department is quite serious in GST compliance and compliance, By placing a wrong reply may cancel your GST registration that can be harsh to the GST Registered person according to its Stock holding by the Business owner & GST tax liability on his stock in hand.

Feel free to contact us on 9555 555 480 or singh@carajput.com

Read also : Registration of GST under Goods and Service Act, 2017

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}