Page Contents

www.carajput.com; GST No late Fees

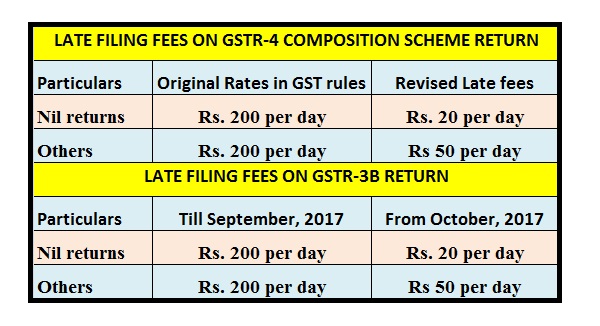

For each GSTR-3B return, a late fee of Rs. 500/- is capped.

In the perspective of the GST taxpayers’ massive relief the government has chosen to limit, on the basis of the condition that such GSTR-3B reports are filed prior to 30 September 2020, a late maximum fee of Form GSTR-3B to Rs 50/- (only 500) by tax return for the tax period July 2017 to July 2020.

Notice was provided to include zero late fees if no tax liability exists; and if there is any tax liability, the GSTR-3B returns filed by 30 September 2020 will be subject to a maximum late fee of Rs. 500 for such returns.

Thanks to further flexibility in the deferred fee paid for tax periods between May 2020 and July 2020, numerous representations have been issued.

In order to clean up past pendency of returns between July 2017 and January 2020, relief has been issued for February 2020 of April 2020 in addition to previously granted.

In addition, the design and implementation of a standard late payment are easier on an automated common portal.

The late fee for the return is only limited to Rs. 500/- if it is filed before 30 September 2020.

The GST Council, chaired by finance minister Nirmala Sitharaman and made up of state ministers, agreed to introduce an amnesty scheme to give taxpayers respite from late fees for pending returns.

For those taxpayers who did not have any tax burden, the late fine for non-furnishing of GSTR-3B from July 2017 to April 2021 has been restricted at Rs 500 per return.

GST Taxpayers who owe money will be penalised a maximum of Rs 1,000 in late fines if their returns are not filed by August 31, 2021.

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

Exemption limit under Long-Term Capital Gains computation in 115BAC Vs Classic 112 Income tax Basic Exemption Limit Under Income Tax… Read More

Top Reasons Why Startups Prefer the Pvt. Ltd. Company structure Starting a business is exciting—but one of the first and… Read More

Complete Overview Legal Entity Identifier (LEI) A Legal Entity Identifier (LEI) is a 20‑digit unique alphanumeric code used to identify… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}