Page Contents

In Budget 2017 our honorable Finance Minister, Mr. Arun Jaitley introduced a new section 234F to ensure timely filing of returns of income.

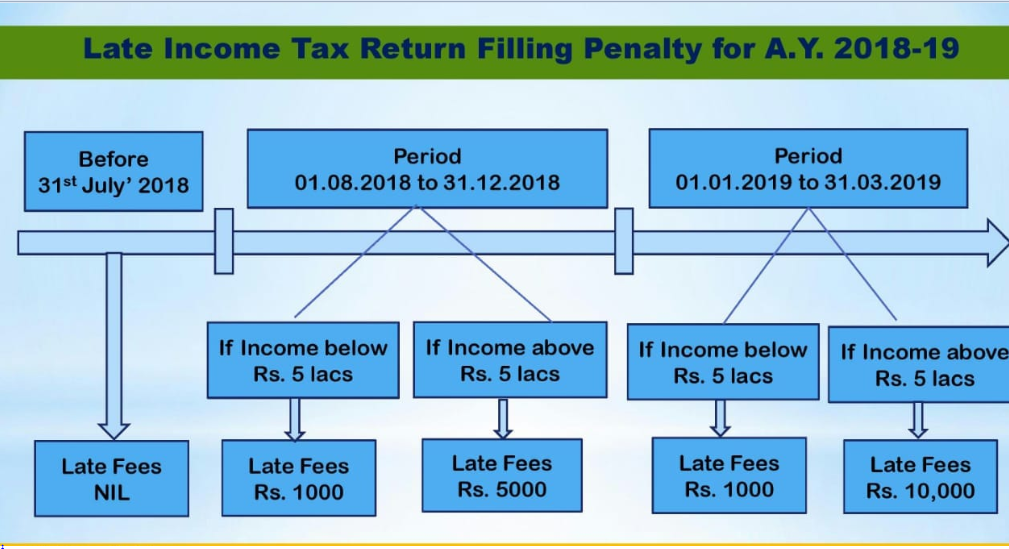

As per section 234F of Income Tax Act, if a person is required to file Income Tax Return (ITR forms) as per the provisions of Income Tax Law [section 139(1)] but does not file it within the prescribed time limit then late fees have to be deposited by him while filing his ITR form. The quantum of fees shall depend upon the time of filing the return and total income.

Provided that if the total income does not exceed five lakh rupees, the fee payable shall not exceed one thousand rupees.

More read:

If a person come under any of the following conditions, then he have to file the income tax returns: –

Due date of tax filing of all type of taxpayer are given below: –

| Category of Taxpayer | Due Date for Tax Filing – FY 2017-18 |

| Individual | July 31st 2018 |

| Body of Individuals (BOI) | July 31st 2018 |

| Hindu Undivided Family (HUF) | July 31st 2018 |

| Association of Persons (AOP) | July 31st 2018 |

| Businesses (Requiring Audit) | September 30th 2018 |

| Businesses (Requiring TP Report) | November 30th 2018 |

If ITR for AY 2018-19 is filed after due date but before 31st Dec of the Assessment year then fees of Rs.5000/- will be levied and If ITR is filed after 31st Dec, then Rs. 10000 will be levied as extra fees.

There is one exception that if your total income is below or equal to Rs. 5 lakhs then maximum penalty is Rs. 1000.

As per Finance Act 2017, Late fees under section 234F can be paid by the way of Self-Assessment Tax u/s 140A. Therefore, through Challan 280, under the head of Self-Assessment Tax, this fees can be paid from FY 17-18 and onwards.

| Rajput Jain & associates Address: -P 6/90 Connaught Place, New Delhi-110001 Mob no. 9811322785/ 9555 5555 480 Website: – singh@carajput.com |

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}