Page Contents

The purchasing power of money (the amount of products that one unit of money can buy) decreases when the price of products rises over time. Due to inflation, if two units of products could be purchased for Rs 100 today, just one unit could be purchased for Rs 100 tomorrow. The Cost Inflation Index (CII) is a tool for estimating inflation-related increases in the cost of goods and assets over time.

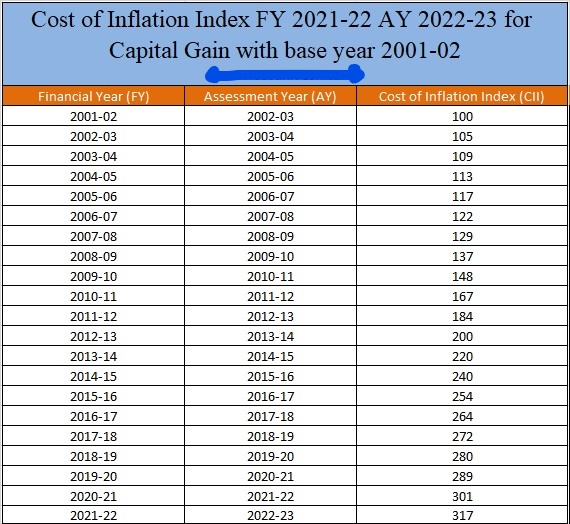

The Cost Inflation Index for the Financial Year 2020-21 has been released by the Ministry of Finance. For fiscal year 2020-21, the Inflation Index is 301. and FY 2021-22 is 317.

In Budget 2017, The Govt recommended changing the indexation benefit’s base year from 1981 to 2001. Keep in mind that the change in the base year affects all asset classes, although the impact varies depending on which assets benefit from indexation on long-term capital gains—capital assets.

The capital gain was calculated using 1981 as the base year up until March 31, 2017. This means that the fair market value of an asset purchased before April 1, 1981, might be used to compute the purchase price.

However, beginning April 1, 2017, the purchase price will be computed using the FMV of 2001. As a result, capital gains on assets purchased before April 1, 2001, will be assessed using fair market value as of April 1, 2001.

| Financial Year | Cost Inflation Index (CII) |

| 2001-02 (Base year) | 100 |

| 2002-03 | 105 |

| 2003-04 | 109 |

| 2004-05 | 113 |

| 2005-06 | 117 |

| 2006-07 | 122 |

| 2007-08 | 129 |

| 2008-09 | 137 |

| 2009-10 | 148 |

| 2010-11 | 167 |

| 2011-12 | 184 |

| 2012-13 | 200 |

| 2013-14 | 220 |

| 2014-15 | 240 |

| 2015-16 | 254 |

| 2016-17 | 264 |

| 2017-18 | 272 |

| 2018-19 | 280 |

| 2019-20 | 289 |

| 2020-21 | 301 |

| 2021-22 | 317 |

2022-23 331

2023-24 363

2024-25 376

2025-26 384

The Cost Inflation Index is used to correlate prices to the rate of inflation. To put it another way, if the inflation rate rises over time, prices will rise as well.

The CII value is significant because it is used to calculate the inflation-adjusted purchase price of assets and, as a result, the LTCG. It’s also crucial to calculate the long-term capital gains/losses (LTCL) on assets that have been sold or are scheduled to be sold in FY 2021-22. When it comes to the cost inflation index, there are two factors to keep in mind. To begin, his number would be used to compute inflation-adjusted cost solely for those assets that allow for inflation-adjusted (indexation benefit).

As a result, the CII value on equity mutual funds could not be used to calculate LTCG/LTCL. Second, this CII number is required to calculate the LTCG for FY 2021-22. You will pay the taxes on these gains when you file your income tax returns (ITR) for the Financial Year 2021-22 (AY 2022-23), which is next year.

By notifying the public, the government establishes the cost inflation index.

Long-Term Capital Assets are documented in books at their cost price. They exist at the cost price and cannot be revalued, despite rising inflation. Because the sale price is larger than the acquisition price, the profit amount remains high when these assets are sold. A greater income tax is also a result of this. The cost inflation index is applied to long-term capital assets, resulting in higher purchasing costs, lower profits, and lower taxes for taxpayers. To benefit taxpayers, the cost inflation index benefit is applied to long-term capital assets, resulting in higher purchase costs, lower profits, and lower taxes.

More read:Taxation on Income from Equity and Debt Mutual Fund

The cost inflation index’s base year is the first year, with an index value of 100. All other years’ indexes are compared to the base year to determine the percentage rise in inflation. Taxpayers can use the higher of the “actual cost or Fair Market Value (FMV) as of the first day of the base year for any capital asset purchased before the base year of the cost inflation index. The benefit of indexation is applied to the calculated purchase price. The FMV is calculated using a registered valuer’s valuation report.

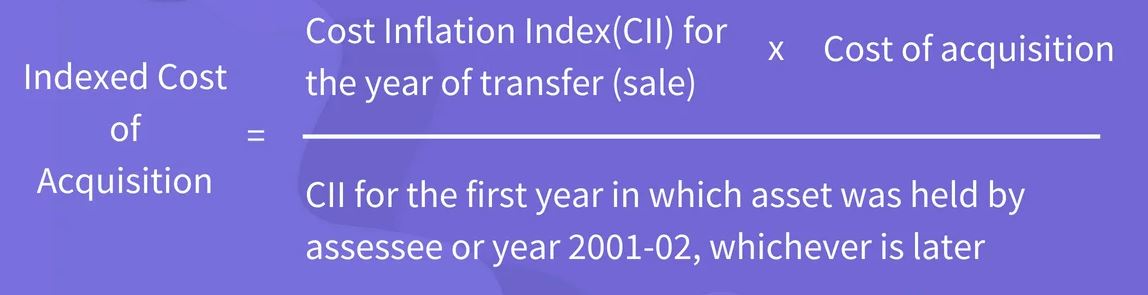

When the indexation advantage is applied to the capital asset’s “Cost of Acquisition” (buying price), it becomes “Indexed Cost of Acquisition.”

DIRECT TAX UPDATE :

Income Tax : CBDT has notified the Cost Inflation Index (CII) for FY 2016-17 at 1125 (FY 2015-16: 1081) – Notification No.42/2016, dt.02 JUN 2016. Income Tax : AIR Information without lawful enquiry is not sufficient to hold a belief that cash deposit is Income and hence cannot form reason to believe that Income has escaped assessment.(Sh. Amrik Singh, vs. Income Tax Officer ) [ITAT Amritsar ]

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}