Page Contents

BRIEF INTRODUCTION

The Foreign Exchange Management Act, 1999 (FEMA) is an act of the Parliament of India to consolidate and amend the laws regarding exchange with the target of facilitating external trade & payments and promoting the orderly development and maintenance of exchange market in India.

Contravention may be a breach or non-compliance of the provisions of The Foreign Exchange Management Act, 1999 (FEMA), and therefore the rules, regulations, notifications, orders or circulars or directions made thereunder.

RBI has been vested with the power to compound offences under The Foreign Exchange Management Act, 1999 (FEMA) and in case a contravention arises under Section 13 of the Act, the same be compounded within 100 and eighty days (180) from the date on which the officer of RBI receives the application for compounding.

Anyone who contravenes the provisions of the touch on adjudication, is susceptible to pay –

and where the contravention is of an unbroken nature, an extra penalty of Rupees Five Thousand for each day after the primary day during which the contravention continues.

Furthermore, as per the Section 15 of the Act, it was provided under the Compounding of Contravention, that where the contravener voluntarily admits contravention, pleads guilty and seeks redressal, the same shall file an application for compounding.

Section 15 of Foreign Exchange Management Act (FEMA), 1999 empowers bank of India to compound any contravention made under Section 13 of FEMA, 1999 except the contraventions under section 3(a).

Compounding refers to the method of admitting voluntarily the breach of any of the provisions of The Foreign Exchange Management Act, 1999 (FEMA) or the rules/regulations/notifications/orders/directions or the circulars issued under the said Act.

The person, admitting the contravening the provisions, shall make a request for compounding his mistakes.

This would indeed provide and protect such person from legal proceedings and makes the method simple and fast. The offence shall be compounded within 180 days from the date on which the requisite officer receives the application for compounding.

Any default/contravention in respect of any provision of The Foreign Exchange Management Act, 1999 (FEMA) shall be compounded by following officers, under the direction and supervision of the Governor of RBI.

| AMOUNT OF CONTRAVENTION FOR COMPOUNDING | COMPOUNDING AUTHORITY OF RBI |

| UPTO RS 10 LAKHS | ASSISTANT GENERAL MANAGER |

| MORE THAN RS 10 LAKHS, BUT LESS THAN RS 40 LAKHS | DEPUTY GENERAL MANAGER |

| RS 40 LAKHS AND ABOVE, BUT LESS THAN RS 100 LAKHS | GENERAL MANAGER |

| RS 100 LAKHS AND ABOVE | CHIEF GENERAL MANAGER |

It is to be noted that compounding provisions shall be applicable only in case of quantifiable contravention only.

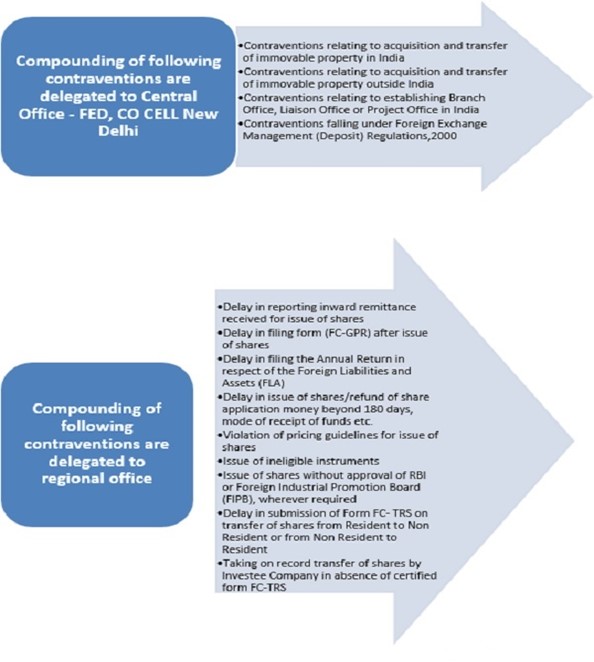

With a view to relax and simplify the process of handling operational issues and customer service, RBI provided for segregation of compounding powers between Regional and Central level.

For Instance – Kochi and Panaji Regional offices are eligible to compound contraventions, where the amount involved is less than Rs 100 Lakhs.

However, where the said amount is RS 100 Lakhs and above in Panaji and Kochi, the compounding will be handled at Mumbai RO and Thiruvananthapuram RO respectively.

Apart from the contraventions laid out in particular, application for all other contraventions needs to be submitted to Foreign Exchange Department, RBI, Mumbai.

The type of contravention is decided to stay seeable the subsequent indicative points:

Thus, the RBI provides for segregation and categorization of the contraventions as provided above and thus, both the contravener and any other person will not have any right to classify the contravention as technical Suo moto.

The RBI is guided by the provisions of section 13 of FEMA, whereby it’s said that the number imposed will be up to 3 times the number involved within the contravention. However, the number imposed is calculated on the premise of guidance note and which is additionally available on the RBI’s website for information of the overall public.

However, the guidance note is barely for the aim of indicating the premise on which the quantity to be imposed comes by the compounding authorities.

the particular amount imposed may sometimes diverge, reckoning on the situations of the case taking into consideration the subsequent factors:

An application for Compounding together with necessary documents and a requirement draft for Rs. 5000/- (Rupees five thousand only) drawn in favor of the “Reserve Bank of India” within the prescribed format shall be sent to the RBI.

the applying must contain pertinent details like, contact details, name of the applicant, the authorized official or representative of the applicant and email ID.

additionally to the appliance, the applicant must also furnish details within the format of Annex II of the foundations referring to Foreign Direct Investment, External Commercial Borrowings, Overseas Direct Investment and Branch Office / Liaison Office, as applicable, together with the Memorandum of Association of the corporate.

Also the most recent audited record together with an undertaking as per Annex-III of the principles must be attached stating that the applicant isn’t under any enquiry or investigation by any agency like the Directorate of Enforcement etc., as on the date of such application.

Where the applicant has not provided adequate details or where the desired approvals haven’t been obtained, the appliance so received by the RBI together with the applying fees of INR 5000 shall be returned and refunded by way of crediting the quantity to the applicant’s account through NEFT

As per the ECS mandate and details of their checking account per Annex-IV of the foundations furnished together with the applying.

Application must be made within the prescribed format containing the contact details i.e. the name of the applicant or his authorized official or representative of the applicant, telephone or mobile number together with the e-mail ID.

other than the applying in prescribed format, following documents must even be furnished:

If the applying for compounding isn’t filed within the prescribed format or the mandatory details, documents or declarations are missing or the applying is filed without the demand draft towards the applying fees, it’ll not be processed and can be returned to the applicant.

Once the appliance is completed altogether aspects within the given time then date of such submission is going to be considered because the date of receipt of application and shall be processed accordingly.

Serious contraventions i.e. contraventions involving concealment, terror financing or anything affecting sovereignty and integrity of the state or the cases

where applicant fails to pay the sum that compounding order was passed within the required fundamental quantity shall be directly stated Directorate of Enforcement for further investigation and necessary actions would be taken accordingly.

If the applicant again commits some contravention within the amount of three years which is comparable to the contravention that a compounding order has already been passed.

It shall not be compounded again and provisions of FEMA, 1999 shall prevail. Any contravention after the expiry of the amount of three years shall be considered for compounding.

Coordination with RBI is a difficult undertaking, but with the passage of time, RBI has made significant attempts to bridge this gap.

Today, RBI’s every move is in this direction. A good example is the consolidated Master Circular for each subject matter.

which is issued annually or half-yearly and compiles all of the alterations or circulars issued throughout the year into one document to give the concerned persons easy access and comfort while dealing with it, and which also served as the foundation for this article.

For query or help, contact: singh@carajput.com or call at 9555555480

Form 16A (Earlier Reflected in Form 26AS) Now Shows Deductor PAN: A Small Change with a Big Impact on TDS Reconciliation… Read More

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

{kind=link}

{kind=link}