Page Contents

Producer companies mean the companies which are registered under the companies act,2013 and it is formed by (A) by any 10 or more individuals every individual should be producer (B) 2 or more producer institution (C) combination of 10 or more individual and more producer institution and the things which have been produced through farming activities.

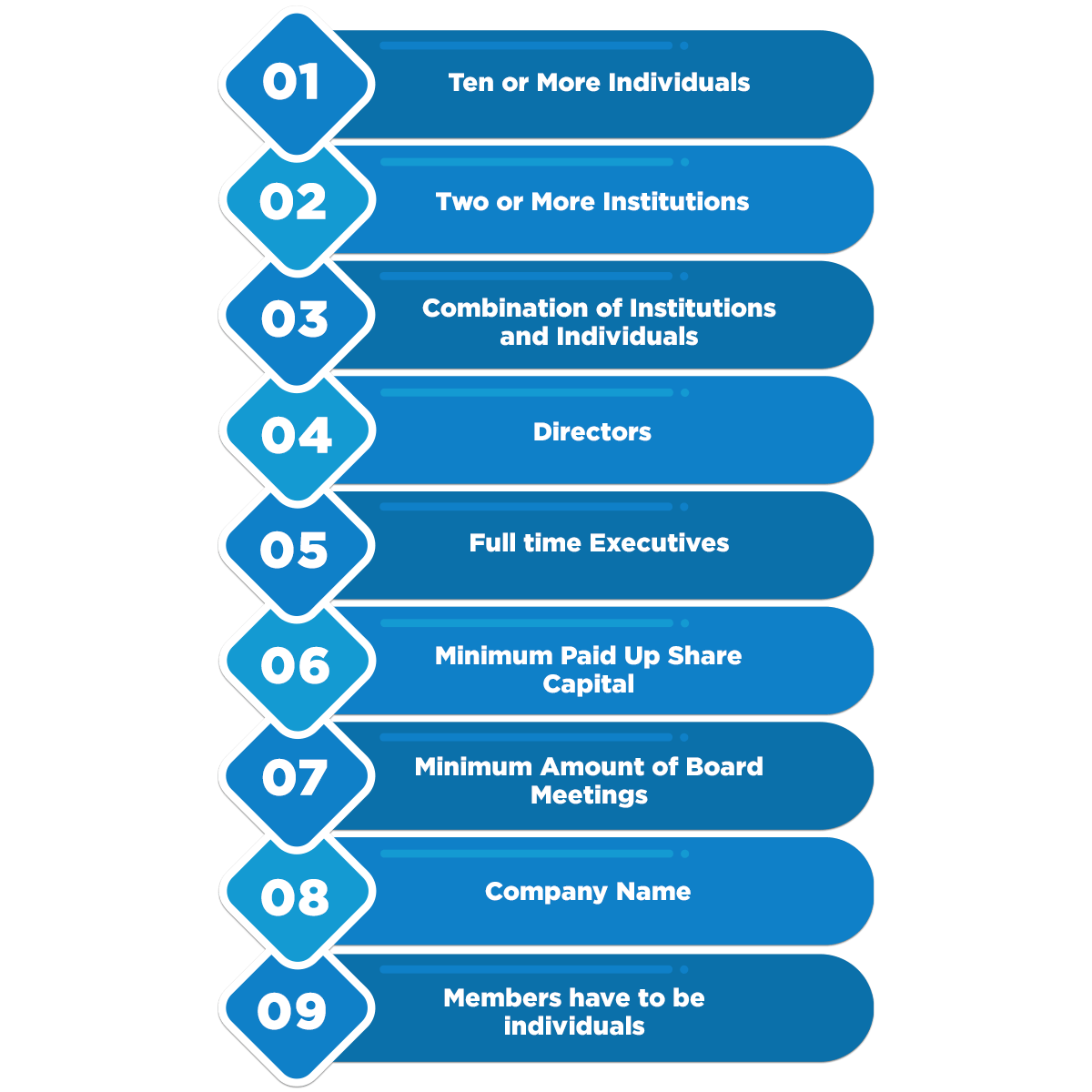

(1) ten or more individuals, each of them being a producer or any two or more Producer institutions, or a combination of ten or more individuals and Producer institutions, desirous of forming a Producer Company having its objects mentioned in section 581B and otherwise complying with the provisions of this Act in respect of registration, may form an incorporated Company as a Producer Company under this Act.

(2) If Registrar is satisfied with all the requirements of this Act have been complied then the registrar shall, within thirty days of receipt of the documents, register the memorandum and the articles and all the other documents and issue a certificate of incorporation.

(3) A Producer Company is formed then the Member’s liability is limited by the memorandum to the amount if any, unpaid on the shares respectively held by them and be termed a company limited by shares.

(4) It may return to all its promoters all the direct costs that relate to the promotion and registration of company including registration, legal fees which shall be subject to the approval of the Members.

(5) On registration the Producer Company shall become a body corporate as it is a private limited company to which the provisions contained in this Part apply, without, however, any limit to the number of Members thereof.

Notice of the annual general meeting shall be accompanied by the following documents-

Memorandum of association and articles of association of the producer company duly signed by the registrar of the company and required to be presented to the registrar of the state where the company registered office is proposed to be situated to be set up.

-Minimum capital of 5 lakhs is required.

-Minimum of 5 directors and a maximum of 15 directors is required.

-It can not be converted into a public company.

Below is the list of documents that are needed from the Producer Company and directors for the registration producer company:

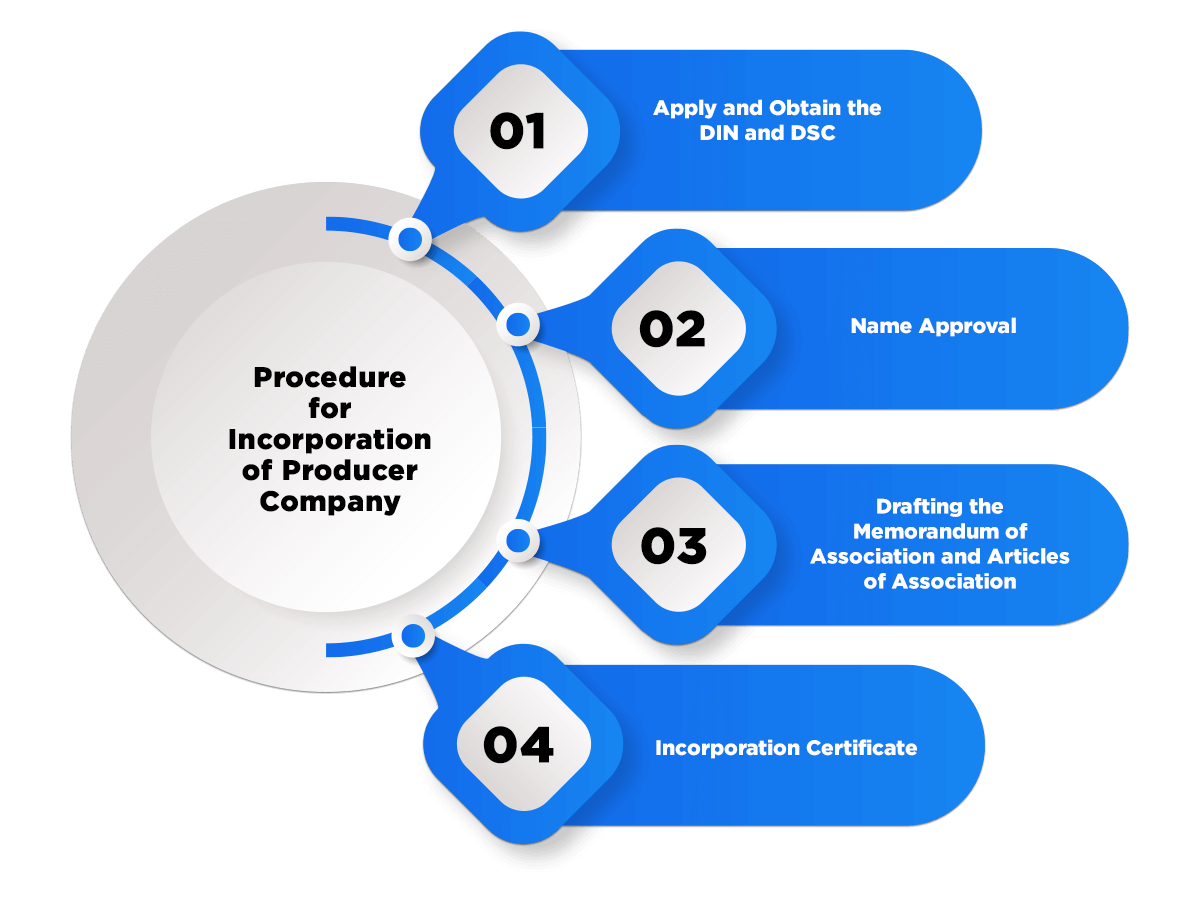

Step 1: Need Apply for DSC

Step 2: Then Apply for DIN

Step 3: Apply for Name Approval through RUN

Step 4: Drafting & submitting final incorporation documents

Step 5: Receiving Certificate of Incorporation & opening Bank Account

Agriculture income is exempt are exempt under the income tax act, 1961. But it does not mean that all the agriculture income are exempted from the income tax act,1961.

It depends upon the activity of agriculture whether the income is exempt or not. forex. If the green tea leaves are processed for manufacturing then 60 percent of income is exempt and 40 percent is taxable.

www.carajput.com; Producer company V/s Producer corporations

Q1 – weather the complaints of the producer company is only for the working producer company?

Ans. – no, the annual complaints of producer companies are for all companies wheater it is a working producer company or a nonworking producer company.

Q2 – does all type of agriculture income is exempt from income tax in producer companies?

Ans. – no, it depends upon the activity whether it is exempt from the income tax act,1961 or not.

Q3 – can the producer company can hold all 4 board meetings in a single quarter?

Ans. No, the producer company must hold a board meeting every quarter of the year.

Q4 – if any director interest changes then at which meeting he is required to disclose his interest?

Ans. – if there are any changes in the director’s interest then he is required to disclose his interest immediately following the next meeting of the board.

Q5- is there is an extension of holding the first annual general meeting of the producer company?

Ans.- the first annual general meeting of the producer company shall be held within 15 months extension of holding the annual general meeting can be granted with the permission of the registrar.

Q6- if articles specify the required number of quorum then one–fourth of the total member will prevail or articles?

Ans. If articles specify the required number of the quorum then it will prevail over one–fourth of the total number of members.

Q7- can a producer company can make an investment that is not mentioned in its object?

Ans.- no, a producer company cannot make an investment that is not mentioned in the object.

Our services shall be as follows:

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}