Page Contents

Many foreign companies have entered India with increasing globalization and liberalization to expand their business portfolio and diversify.

All companies that have been established and set up in India, whether Indian or international, must follow the laws and rules enacted by the government.

The difference is that the compliance requirements expected of a foreign subsidiary company in India are significantly greater than those required of an Indian entity.

Compliance for Foreign Subsidiary Companies in India

A foreign corporation is defined in Section 2(42) of the Companies Act, 2013.

“Foreign company” means any corporation or body corporate formed outside of India that:

There are three primary forms of time-based compliances, according to the regulated norms, rules, and statutes. The following are the types of compliances that must be met by a foreign subsidiary firm based on their intermittency:

These are the compliances that must be done on an annual or yearly basis for foreign subsidiary enterprises. The corporation must comply with the rules at least once every financial year.

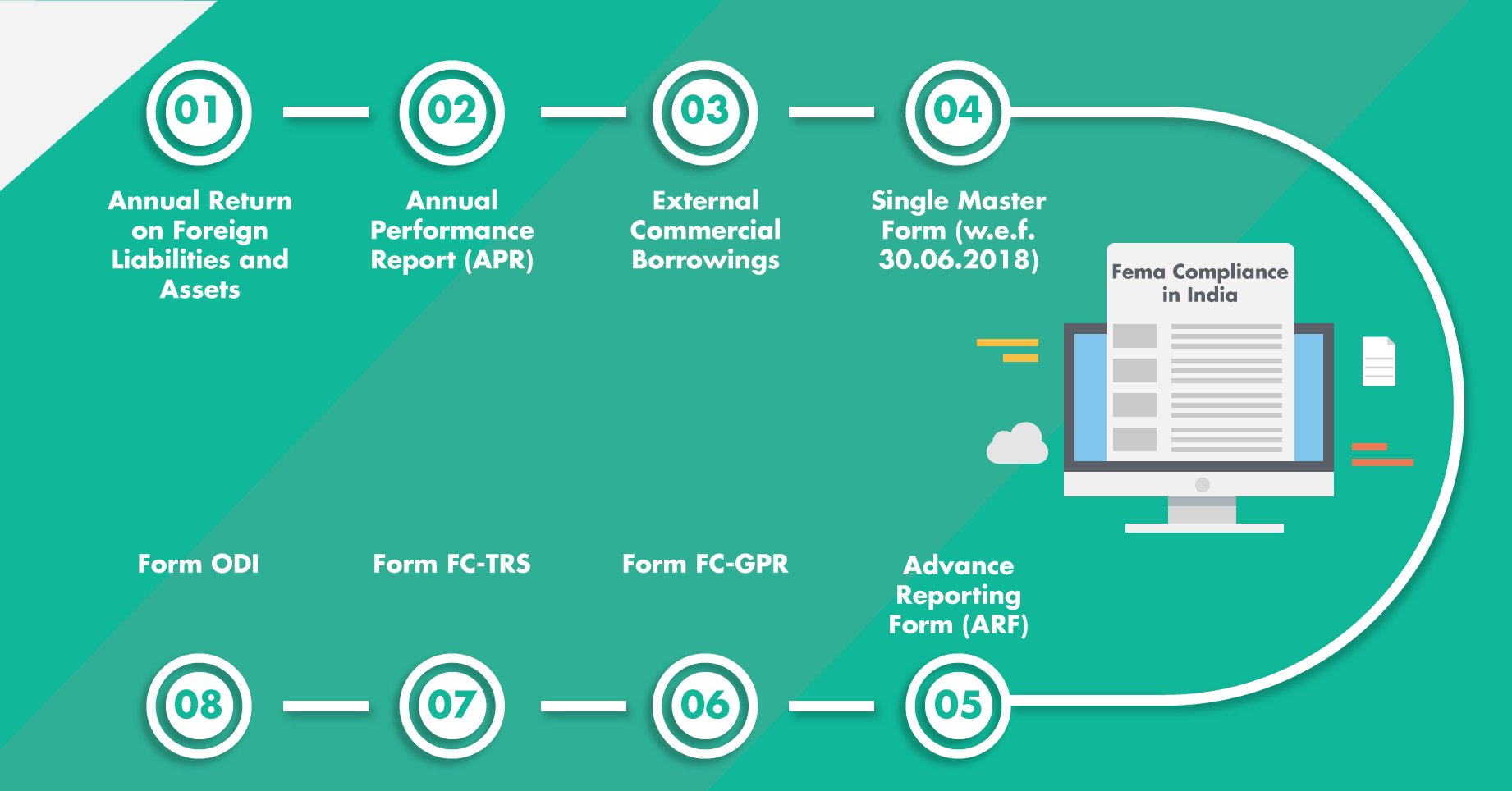

Compliance requirements for a foreign subsidiary include: Event-based compliance is another sort of compliance for a foreign subsidiary. This means that the corporation must comply with such regulations, particularly when doing certain activities or at significant events. There are two event-based compliances for foreign enterprises, according to RBI regulations and guidelines and the Foreign Exchange Management Act (FEMA) are as follows:

When shares of a foreign subsidiary firm are transferred from an Indian resident to a non-resident investor and vice versa, this form must be filled. Such transfers are possible through a sale or a gift.

These are the compliances that must be completed on a regular basis for a foreign subsidiary. These compliances, unlike yearly compliances, have to be performed at regular intervals throughout the year. These can be done on a monthly, quarterly, or half-yearly basis, depending on the needs.

All of the above-mentioned compliances for foreign subsidiaries must be met regardless of when they occur. If the company fails to meet them, harsh consequences like as penalties, interest, and other forms of punishment may be imposed.

If the noncompliance is substantial, the company may be subject to criminal charges and accusations under applicable legislation.

The penalties for non-compliance for the foreign subsidiary are outlined in Section 392 of the Companies Act, 2013. According to the clause, which took effect from April 1, 2014.

“392. Punishment for contravention: Without prejudice to the provisions of section 391, if a foreign company violates the provisions of this Chapter, the foreign company shall be punished with a fine of not less than one lakh rupees but not less than three lakh rupees, and in the case of a continuing offense, with an additional fine of fifty thousand rupees for each day after the first during which the foreign company violated the provisions of this Chapter.”

Section 392 and the penalties it applies for failing to comply with compliance requirements for foreign corporations can be explained as follows.

As a result, it is critical to comply with all regulatory requirements for both the foreign subsidiary and the parent company in order to continue operating without interruption from regulatory organizations or authorities.

The Companies (Registration of Foreign Companies) Rules, 2014, which give standards for foreign company registration in India, regulate the incorporation of a business in India by a foreign business.

Compliance requirements for wholly-owned subsidiaries and other provisions were explored in other articles. we will go over the other important compliance and requirements for such businesses.

Types of compliance for a subsidiary company:

The following are the other types of compliance for the subsidiary company in India.

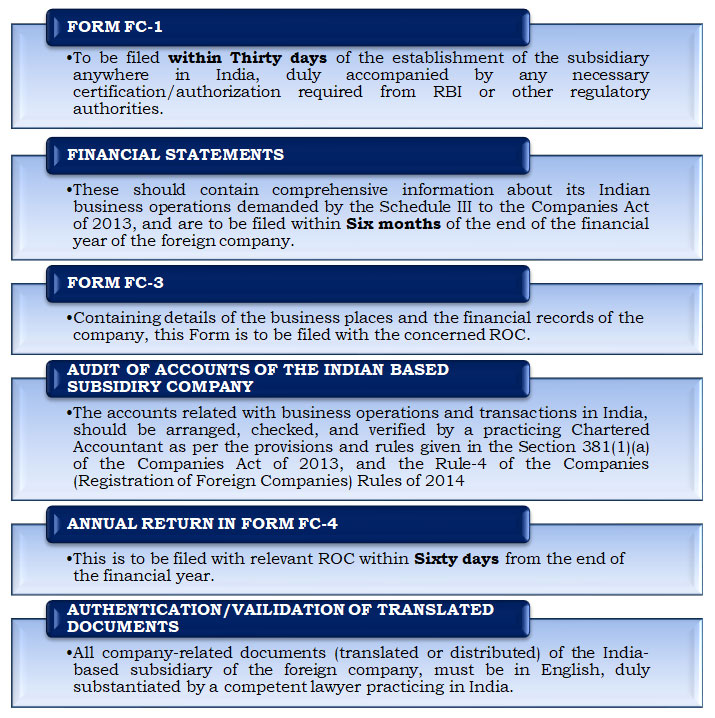

A foreign company must provide the Registrar of Companies with all information about its directors and secretary (ROC). While fulfilling this compliance for a foreign company, the following points must be kept in mind.

The foreign company’s financial statements:

For the purpose of foreign company compliance, it must prepare for each financial year financial statements for the business operations in accordance with Schedule III of the Act. The following items must be included in the company’s financial statements to ensure compliance for a foreign company:

Foreign company account audit:

They must have their accounts audited at regular intervals following registration for foreign companies in India. In accordance with Section 381(1) and Rule 4 of the Company Act, all foreign companies incorporated in India must have their accounts audited by a practicing Indian Chartered Accountant or by a Chartered Accountant firm.

Foreign company’s place of business:

All foreign companies are required to file details, in FC3 form, concerning the company’s entire place of business and locations in India until the date of the preparation of their balance sheet. It is important compliance for foreign companies that must be met in order to avoid penalties.

Filing of Annual Returns:

The foreign company must file annual returns with the registrar using Form FC-4. This must be filed within sixty days of the fiscal year’s end. To complete this compliance for a foreign company, the prescribed fees must be submitted along with the form.

Documents in a foreign company’s prospectus :

The following documents must be annexed or attached to the company's prospectus:

Rajput Jain & Associates Associate will understand your business requirements and help you with all related issues.

For any information/queries, you can contact us. Our team of experts can provide all the assistance related to Foreign Subsidiary compliance. For Contact:

Website- Click here

Email id- singh@carajput.com

Popular Articles :

Understanding Form 16, Form 16A & Form 26AS: A Complete Guide for Taxpayers When filing your Income Tax Return (ITR),… Read More

CFO Cum whole-time director? ROC Gwalior Says No in EKI Energy Services Case Corporate governance is built on the principle… Read More

Toughest Exams in India: More Than a Test of Knowledge, A Test of Character Every year, millions of students and… Read More

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

Overview Taxation of Firms & LLPs in India Key aspects of taxation of partnership firms and limited liability partnerships are… Read More

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}