Page Contents

Query : Why cash credit or overdraft a/c can’t be attached for tax roecvery?

Answer: Cash Credit Account or Overdraft Account : In case of Cash Credit (‘CC’) or Overdraft (‘OD’) account customer is always in debit balance. There is no stage at which the bank is a debtor to its customer, nor at any point of time at which it holds any money. Thus, CC/OD accounts cannot be attached. However, tax authorities insist on attachment of CC/OD accounts of taxpayers to recover tax dues.

Dispute : The income-tax department is insisting on attachment of Cash Credit (CC) or Overdraft (OD) accounts of taxpayers to recover income-tax dues. Now following questions arise –

Judicial precedents

Decision of the Madras High Court : In case of K.M. Adam v ITO [1958] 33 ITR 26 (MAD.) the Ld. Counsel of revenue tried to justify attachment of CC/OD account on following basis “Immediately the customer drew a cheque on his overdraft account, which the bank had by reason of the arrangement with the customer to honour, the money which it thus decides to pay to its customer becomes at once the customer’s money which, between the time when the bank makes up its mind to pay and the time of the actual payment, it holds on the customer’s account.”

The Madras High Court was of the view that this approach was too metaphysical. If this theory would be applied to simple loan transaction, then it would be deemed that lender is holding sum for or on account of would be borrower whenever he makes up his mind to lend money and agrees to do so. When a bank lends money on overdraft and the customer is always in debit there is no stage at which the bank is a debtor to its customer, nor any point of time at which it holds any money on his account.

Thus, the Madras High Court has held that unless the bank is a debtor there could be no attachment; an unutilised overdraft account does not render the bank a debtor in any sense and, therefore, the bank is not a person from whom money is due to the customer.

In case of P. C. Chandra & Sons (India) Ltd. v. Dy. CIT [2015] 63 taxmann.com 38 (Calcutta) the judgment of K.M. Adam (Supra) was followed to hold that tax authorities could not attach cash credit account of the taxpayers to recover tax dues.

Thus, on basis of aforesaid observation of the High Court it could be concluded that –

Bank could not be deemed to be holding unutilized balance of CC/OD account on behalf of its customers; and, Tax authorities cannot attach OD/CC account of taxpayers.

Though tax authorities don’t have powers to attach OD/CC account of a taxpayer, yet it can attach current account, saving account or fixed deposit account as in such cases bank could be said to be debtor of assessee or holding money on behalf of the assessee. However, tax authorities cannot prematurely close the FD and demand its encashment.

Thus, tax authorities should discontinue its annoying practice of insisting on the attachment of OD/CC accounts of taxpayers to recover tax dues.

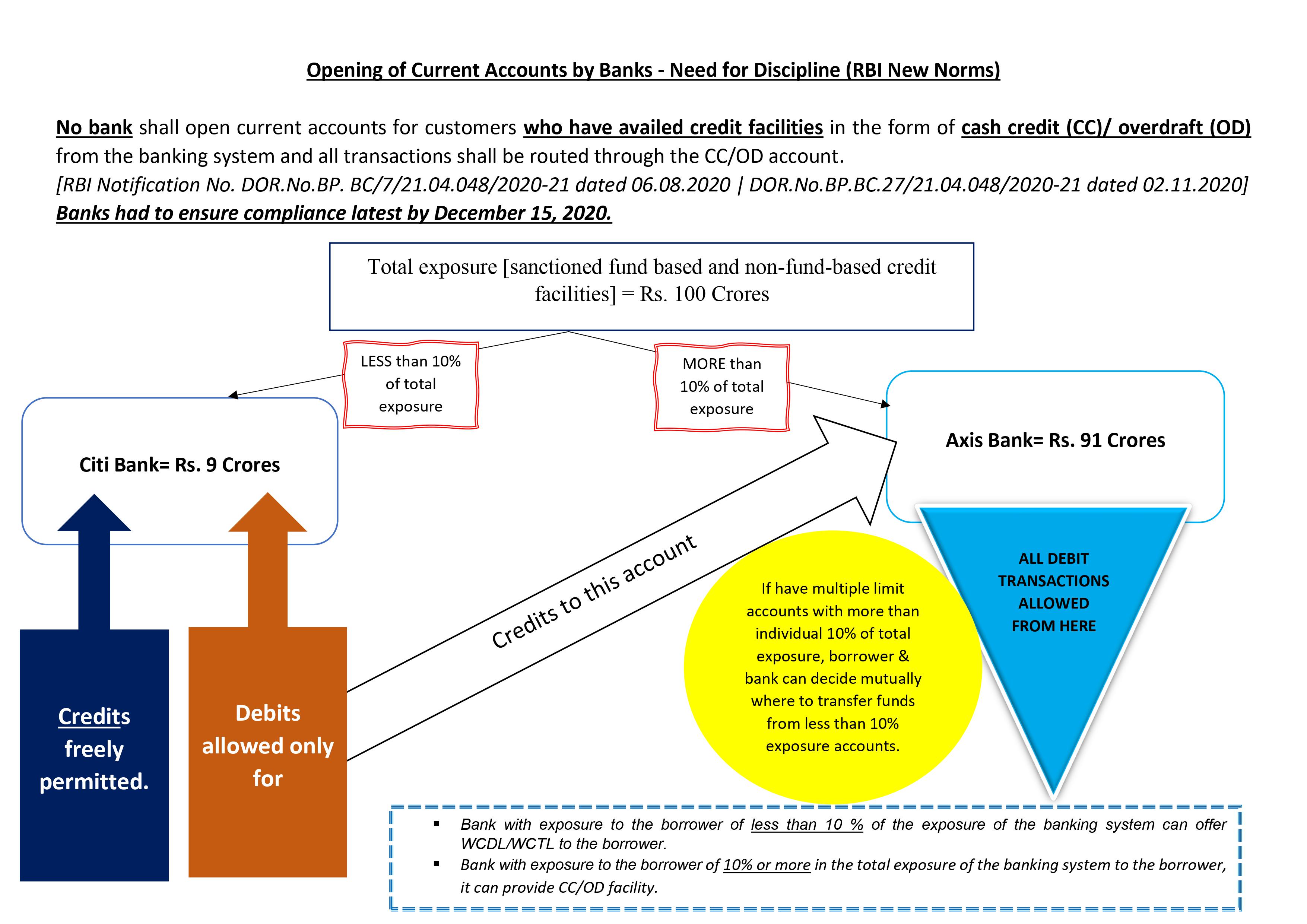

The RBI perceives that borrowers misuse money via multiple current accounts with various banks, despite the prevailing regulations and penal provisions.

The Guidelines for the monitoring of cash flows and controlling the use of the current accounts and for the substitution of NOCs are issued.

Customers now fall into three categories when applying for open current accounts. Current accounts cannot be opened to banks with customers that have existing bank credit facilities as cash (CC) or excessive (OD) credit systems. The CC/OD accounts must route transactions.

If a bank’s borrower’s exposure is below 10% of its bank system’s exposure to that borrower, CC and OD accounts can be opened. Debits from these accounts may be held only by the borrower’s CC or OD account held at a bank where the banking system is 10 percent or more exposed to the borrower.

Current accounts may be opened by banks with clients that have current credit facilities in the banking system but have no CC or OD facility. When the borrower’s exposure to a banking system amounts to 500 million or greater, only the corporate bank with a compulsory escrow mechanism may open the current accounts. Loan banks may open account collection provided that money is transferred to escrow accounts in these accounts only. Such borrowers cannot open banks that are not lending.

Banks that have no banking credit facility can open up current accounts under their due diligence policies with customers. In determining the overall exposure of the bank system, the RBI has clarified that only the exposure of scheduled commercial banks and payment banks is included. The other financial institutions are excluded from all NBFC exposure.

Every lending bank and other account-holding bank must monitor the current accounts, CC, and OD accounts and comply with the guidelines on a six-month basis.

The guides and exemption guidelines are a welcome step towards strengthening the banking system by implementing better discipline in terms of reimbursement to large borrowers and preventing misuse of funds. The implementation, however, presents bankers with a challenge.

| Feature | Cash Credit (CC) | Overdraft (OD) |

| Purpose | For business working capital (raw materials, inventory, daily ops) | For short-term liquidity needs (personal or business) |

| Eligibility | Against stock, receivables, business assets | Against FDs, salary/savings account, property, securities |

| Users | Businesses (traders, manufacturers) | Individuals & businesses |

| Limit Determination | Based on drawing power from stock/receivables after margin | Based on bank relationship, income, security, account history |

| Tenure | Short-term (12 months), reviewed annually | Short or long-term, renewed per agreement |

| Interest Charged | On utilized amount only, not full limit | Same — only on amount used |

| Flexibility | Structured for business cash flow | More flexible, usable for personal or business |

| Documentation | Requires detailed financials, GST returns, stock statements | Simpler, especially if backed by FD or salary account |

For query or help, contact: singh@carajput.com or call at 9555555480

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

Overview Taxation of Firms & LLPs in India Key aspects of taxation of partnership firms and limited liability partnerships are… Read More

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

{kind=link}

{kind=link}