Inverted Duty Structure Correction in the Footwear and Textiles Sector

- In order to correct the inverted duty structure in the Footwear and Textile Sector, the GST Council decided to introduce GST rate changes starting effective from 01.01.2022.

- All footwear, regardless of price, will be subject to a 12 % GST, while all textile products, including readymade clothing, would be subject to a 12 percent GST.

No appeal can be filed against a section 129(3) order Unless an amount equal to 25% of the penalty is paid,

- Under Section 116 of the Finance Act of 2021 proposes to add a proviso to section 107(6), stating: “Provided that no appeal shall be brought against an order made under Section 129(3), unless the appellant has paid an amount equal to twenty-five percent of the penalty.”

GST Provision for communicating invoice or debit note details to the recipient

- Under Section 109 of the Finance Act of 2021 proposes to amend section 16 of the CGST Act by inserting the clause “(aa) the details of the invoice or debit note referred to in clause (a) has been furnished by the supplier in the statement of outward supplies and such details have been communicated to the recipient of such invoice or debit note in the manner specified under section 37(a).

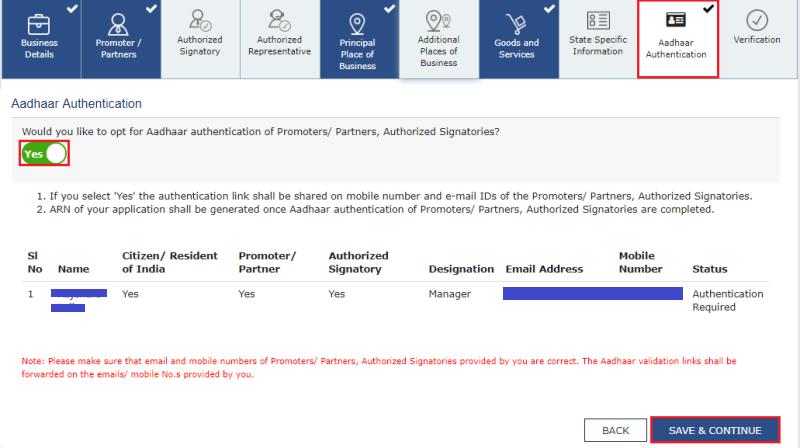

Aadhaar authentication System required for GST refund & Revocation requests.

- CBIC has announced that mandatory Aadhaar authentication for GST refund and revocation applications will take effect from 01.01.2022.

- its is Compulsory Aadhar authentication for claiming GST Refund application & application for GST Registration Revocation application effective from 01.01.2022.

When a proper officer detains or seizes items or a conveyance, he or she must give notice within seven days of the detention or seizure.

- Proper GST official detaining or seizing goods or conveyance shall publish a notice indicating the penalty payable within seven days of such detention or seizure and then pass an order defining the penalty payable within 7 days of the date of delivery of such notice.

GSTR-1 will be blocked if GSTR 3B is not filed.

- If you have not filed a GSTR-1 return in FORM GSTR-3B for the previous two return periods, the GSTR-1 return filing facility will be blocked on January 1, 2022.

- In case a taxpayer does not file GSTR-3B for October and November 2021, for example, the GSTR-1 filing facility will be unavailable beginning effective from 01.01.2022.

GST Commissioner empowered to attach provisionally, any property of taxpayer, including bank account related with them.

Under Section 115 of the Finance Act of 2021 seeks to amend section 83, namely

“(1) Where, after the initiation of any proceeding under Chapter XII, XIV, or Chapter XV, the GST Commissioner is of the opinion that it is required to do so for the purpose of protecting the interest of the Government revenue, he may, by order in writing, attach provisionally any property of taxpayer including bank accounts, belonging to the taxable person.”

The GST Commissioner’s power to call for information

- Under Section 119 of the Finance Act of 2021 proposes to replace section 151 with a new section titled

“Power to call for information”:

- GST Commissioner or an officer authorised by him may by order direct any person to furnish information relating to any matter dealt with in connection with this Act within such time in such form, and in such manner as may be specified therein.

Self-assessed tax shall include the tax payable in respect of details of outward supplies

- Under Section 114 of the Finance Act of 2021 proposes to add an explanatory note under section 75 stating that “For the purposes of this subsection, the expression “self-assessed tax” shall include tax payable in respect of details of outward supplies furnished under section 37 but not included in the return furnished u/s 39.”

Ola, Swiggy, Uber, Zomato, & other e-commerce companies are now subject to a new GST burden.

- At a GSTN Council meeting, it was decided that e-commerce operators should be held liable for tax on services provided through them such as passenger transportation by any type of motor vehicle, restaurant services or restaurant services provided with with some exceptions.

- The aforesaid statement issued by the Ministry of Finance after the meeting of GSTN Council. It will be become with effect from 01.01.2022,

Other changes related to e-commerce companies

- E-commerce operator services will no longer be required to collect TCS & file GSTR-8 in respect of ‘restaurant services’ on which it pays tax U/s 9(5) of the CGST Act, 2017, but will continue to collect TCS and file GSTR-8 for other services.

- Explanation issued related to modalities of compliance in respect of supply of “Restaurant Service” Via E-Commerce Operators w.e.f. 01.01.2022.

- E-commerce operator will be liable to pay Goods and Services Tax on restaurant service supplied through them including by an un-registered person.

- Total Turnover of person supplying restaurant service through e-commerce operator shall be computed as defined in under section 2(6) of the CGST Act, 2017 and shall include the aggregate value of supplies made by the restaurant via e-commerce operator.

- As e-commerce operator services are registered as per rule 8 of the CGST Rules, 2017 and there would be no compulsory need of taking new registration by e-commerce operator services provider for payment of tax on restaurant service.

- Registered persons supplying restaurant services through e-commerce operator. U/s 9(5) of CGST Act will report such supplies in Table 8 of GSTR-1 and Table 3.1 (c) of GSTR-3B, for the time being.

- e-commerce operator shall not be needed to reverse Input Tax Credit on account of restaurant services on which it pays Goods and Services Tax in terms of section 9(5) of the CGST Act, 2017.

- No Input Tax Credit could be utilized for payment of Goods and Services Tax on restaurant service supplied via e-commerce operator.

- E-Commerce operator shall pay the complete Goods and Services Tax liability in cash on restaurant service.

- CBIC recommended GST officials to be just and fair in enforcing the new GST compliance rules, which took effect on January 1, 2022.

- Finance Act of 2021, which was notified in December, included new measures approved by the GST Council. Buyers cannot claim tax credits if a seller fails to record or pay tax responsibilities, according to the rules. Furthermore, officials now have greater authority to seize assets in certain cases of tax evasion.

- If there is a mismatch in GSTR-1, officers would be able to take action against enterprises to recover dues if they under-report monthly sales while paying taxes (GSTR-3B).

- Businesses will also be unable to file tax returns for the current month if returns for the previous month’s sales are not filed.

The Central Board of Indirect Taxes and Customs said field GST officers shall be familiarized with the New GST rules and try to implement them in a “just & fair” manner, a person said, seeking anonymity.

But 2 clauses have created unease in the industry. “If there is an clerical error, unintentional & one furnishes a higher figure in GSTR-1 relating to outward supplies (sales) by mistake,

Rajput Jain & Associates said that GST amendment of the mistake will be allowed only in the next month.

Popular Articles :

Key takeaways about TDS under GST

Complete Guidance on TDS applicable on Goods and Services Tax

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}