Page Contents

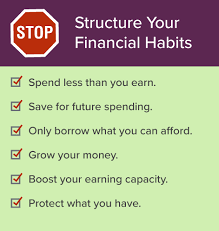

Live within your means: This is the number one rule for the effective administration of personal finance.

Make sure you buy what you can afford — This is the most fundamental thing you need to learn. Don’t depend on credits to buy something.

Let’s understand this better- suppose you want to buy your wife an expensive present, it might be a package of diamonds or something else. You may not have enough money to buy the same one. Whatever it may be, you decide to take a loan-a a personal loan or use your credit card.

But after some time, what you’ll realize is- you’re paying much more on interest than the actual amount borrowed. To resolve the particular debt, you need to pay monthly EMIs for a minimum of one to two years. These are all unnecessary debts that can be easily avoided. If the EMIs you pay towards this had been invested elsewhere- it would have resulted in even more profit!

Track your expenditures: Keep track of what you spend. This way, your account is less likely to be overspent. It’s also a great way to keep track of your credit card spending so you can avoid and restrict the excessive outgoing from your revenue.

Have a budget: You’re supposed to have a money plan. Like what do you want to do with it? What can you do to maximize the value of the same? Suppose you are also in your account of Rs 50000. Make break-ups and the expenditure and investment plans. You’re going to spend Rs 10,000 on supermarkets, Rs 10,000 on loan repayment (EMIs), Rs 5000 for driving, and others. Plan for full savings, and effectively invest the left number.

Clear your bills monthly: It’s always considered one of the good financial habits to clear your bills frequently. It not only removes the risk of late payment but also leads to savings. Credit cards are one of the plastic money commonly used which facilitates your financial life.

But, on a very high side, the interest rate charged. Late payment not only adds to the interest on your credit card bills, but penalties are the addons that make it huge. So, when you’re using a credit card, try paying the bill monthly, it’s a must if it’s not possible to pay the minimum.

Hold your debt rates low: It’s you are a need borrow for a few items like a home, car, or education. But only seek to borrow what you need when borrowing for these. Seek to borrow as little as possible & as per your capacity to payback. With a better credit score, your total loan payments need not be higher than 36 percent of your monthly income.

Make sure you pay the best prices: make sure you compare the price on various websites & stores when purchasing any item. Ensure that you pay the lowest prices for the products and services that you may have exposure to. Look for discounts, coupons, and offers to help to make your purchase worth.

To conclude, you’ll be better prepared for tomorrow by following and respecting healthy financial behaviors. Here are only a few simple steps to help you handle your money the right way:

This is a well-crafted and engaging piece on investing in mutual funds during market dips! Here are some suggestions for improvement:

Read our articles:

Form 16A (Earlier Reflected in Form 26AS) Now Shows Deductor PAN: A Small Change with a Big Impact on TDS Reconciliation… Read More

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

{kind=link}

{kind=link}

{kind=link}