Page Contents

All the Transactions liable to be reported in the statement of financial transactions can now be classified into 2 Type:

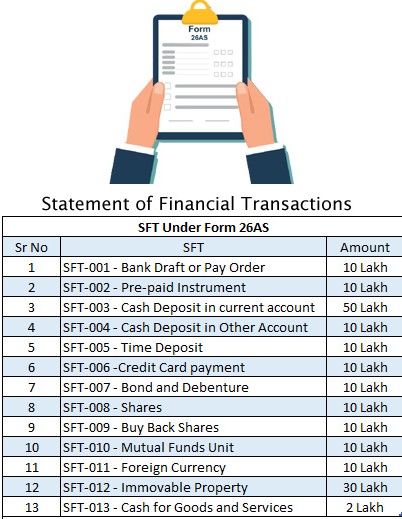

Below ‘SFT’ are needed to be reported if the value of the transaction cross the threshold limit, & it is registered or recorded by the specified person:

| Sl. No. | Particular and Nature of transaction | What is the Value of Transaction | Who is the Reporting Entity |

Foreign Currency Transactions | |||

| 1 | Expense in foreign currency via debit or credit card or Via issue of Travellers Cheque or Draft or any other instrument. | IF Total INR 10,00,000/- or more in a FY. | |

| 2 | Receipt from any person for sale of foreign currency including credit of such currency to foreign exchange card | IF Total INR 10,00,000/-or more in a FY. | ♦ Authorized Dealer ♦ Money Changer ♦ Offshore Banking Unit ♦ Any other person authorized to deal in foreign exchange or foreign securities |

Investments | |||

| 3 | Purchase or sale by any person of immovable property | IF Total INR 10,00,000/-or more in an FY. | Inspector-General or Registrar or Sub-Registrar under the Registration Act, 1908 |

| 4 | Receipt from any person for acquiring shares (including share application money) issued by the company | IF Total INR 10,00,000/-or more in an FY. | A company issuing shares |

| 5 | One or more time deposits (other than a time deposit made through renewal of another time deposit) of a person | IF Total INR 10,00,000/-or more in an FY. | ♦ Bank or Co-op. bank ♦ Post-Master General ♦ Nidhi Companies ♦ NBFCs |

| 6 | Receipt from any person for acquiring units of one or more schemes of a Mutual Fund (other than the amount received on account of transfer from one scheme to another scheme of that Mutual Fund) | IF Total INR 10,00,000/-or more in a FY. | A trustee of a Mutual Fund or such other authorized person managing the affairs of Mutual Fund |

| 7 | Receipt from any person for acquiring bonds or debentures issued by the company or institution (other than the amount received on account of renewal of the bond or debenture issued by that company) | IF Total INR 10,00,000/-or more in a FY. | A company or institution issuing bonds or debentures |

| 8 | Buyback of shares from any person (other than the shares bought in the open market) | IF Total INR 10,00,000/-or more in a FY. | A company listed on a recognized stock exchange purchasing its own securities |

Cash Transactions | |||

| 9 | Receipt of cash payment for sale, by any person, of goods or services of any nature, not being a transaction whose specific reporting is otherwise required | In case the Amount is more than Rs. 2 lakhs | Any person who is liable for tax audit under Section 44AB |

| 10 | Cash payment for the purchase of pre-paid instruments issued by the RBI | IF Total INR 10,00,000/-or more in an FY. | Bank or Co-op. Bank |

| 11 | Cash deposits in one or more accounts (other than a current account and time deposit) of a person | IF Total INR 10,00,000/-or more in a FY. | ♦ Bank or Co-op. Bank ♦ Post-Master General |

| 12 | Cash payment for the purchase of bank drafts or pay orders or banker’s cheque. | IF Total INR 10,00,000/-or more in a FY. | Bank or Co-op. Bank |

| 13 | Cash withdrawals (including through bearer’s cheque) from one or more current account of a person | IF Total INR 50,00,000/-or more in a FY. | Bank or Co-op. Bank |

| 14 | Cash deposits in one or more current account of a person | IF Total INR 50,00,000/-or more in a FY. | Bank or Co-op. Bank |

Below ‘SFT’ are required to be reported by the specified person “Company/Reporting Entity”. No threshold limit is prescribed for the Below transactions.

| Sl. No. | Particular and Nature of transaction | Who is Reporting entity |

| 1 | Interest income | ♦ A Banking company or a Co-op. Bank; ♦ Post-Master General; ♦ NBFCs |

| 2 | Deemed Dividend U/s 2(22)(a) to (e) | A Company |

| 3 | Capital Gains on the transfer of Units of Mutual Funds | ♦ Recognized Stock Exchange; ♦ Depository as defined in section 2(1)(e) of Depositories Act, 1996; ♦ Recognized Clearing Corporation; ♦ Registrar to an issue and share transfer agent registered under section 12(1) of the SEBI Act, 1992. |

| 4 | Capital Gains on the transfer of securities listed on any recognized stock exchange in India | ♦ Recognized Stock Exchange; ♦ Depository as defined in section 2(1)(e) of Depositories Act, 1996; ♦ Recognized Clearing Corporation; ♦ Registrar to an issue and share transfer agent registered under section 12(1) of the SEBI Act, 1992. |

| 5 | Final or Interim Dividend income | A Company |

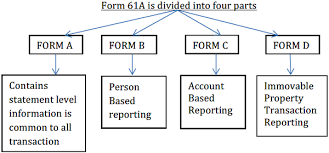

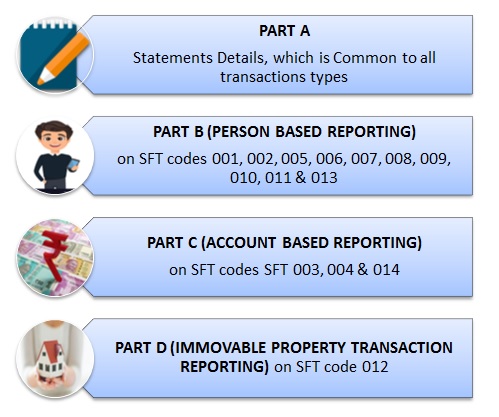

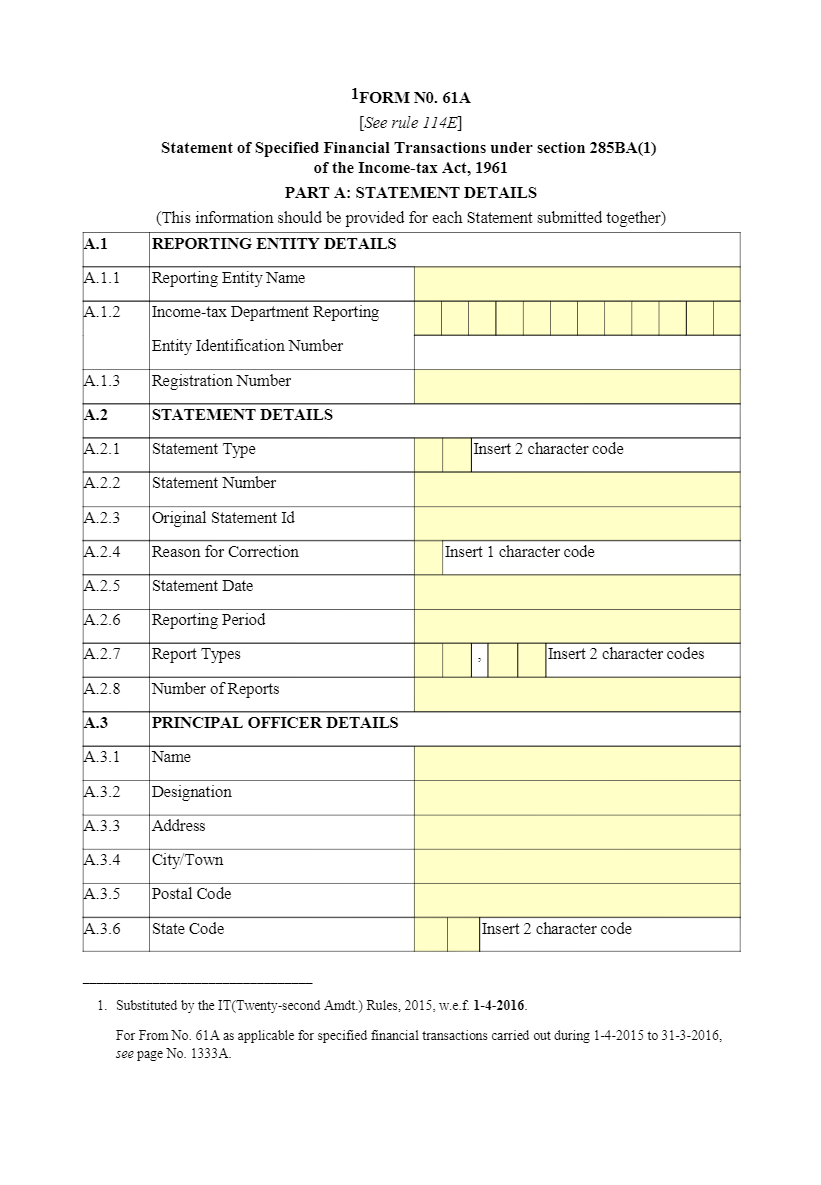

The statement of financial transactions shall electronically be submitted in relation to an FY by reporting entity with a DSC of the person responsible for verifying the declaration in Form No. 61A. The statement of financial transactions shall be submitted instantly after FY in which the transaction is registered or registered, on or before 31 May.

In case of non-furnishing of the statement of financial transactions within due date, Total, a penalty of Rs 500/- per day from the expiry of original due date till the due date mentioned in the notice and Rs 1,000 per day beyond the due date specified in the notice. (Reference from Section 271FA of the Act)

The penalty of Rs 50,000 will be levied on prescribed reporting financial institution if it provides inaccurate information in the statement where:

👉The last date for filing the Statement of Financial Transactions (SFT) for F.Y. 2023-24 is May 31st, 2024.

👉SFT is required to be filed in Form No. 61A for transactions entered with third parties.

Do ensure timely submission of your SFT!

Conclusion:

We look forward for your valuable comment:

FOR FURTHER QUERIES CONTACT US: W: www.carajput.com E: singh@carajput.com T: 9-555-555-480

Form 16A (Earlier Reflected in Form 26AS) Now Shows Deductor PAN: A Small Change with a Big Impact on TDS Reconciliation… Read More

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}