Overseas Direct Investment Without Remittance of Funds From India

An investment outside India will be done by an Indian party or a private or (single or in association with another resident individual or with an ‘Indian Party’).

All resident individuals, including minors, are allowed to freely remit up to USD 250,000 per yr.

An Indian Party is allowed to make overseas direct investment in any of the prescribed bonafide activities. However, reality and banking business are the prohibited sectors for overseas direct investment.

But Indian banks operating in India can found JVs/WOSs abroad provided they obtain clearance under the Banking Regulation Act, 1949, from the Department of Banking Regulation (DBR) and RBI.

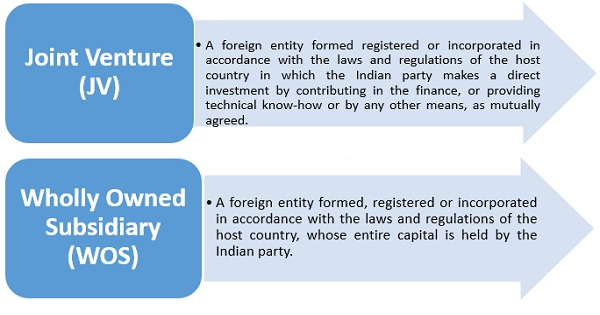

Forms of Entity that An Indian party can form for Overseas Direct Investment: –

♦ In both the cases, an Indian Party should approach a licensed Dealer Category – I Bank (hereafter, referred to as “AD bank”) with an application in Form ODI Part-I together with the prescribed enclosures/documents.

♦The AD bank should report the relevant Form ODI within the online OID application and procure UIN while executing the remittance and intimate to the Remitter which shall be employed by him all told the longer-term communication made with RBI.

| AUTOMATIC ROUTE | APPROVAL ROUTE |

No requirement for obtaining prior approval of RBI is required, where an Indian party make ODI in equity shares and in compulsorily convertible preference shares, subject to the following conditions: - The was should be engaged in bonafide business activity.

- Total financial commitment of the indian party in all was should not exceed 400 % of the net worth of the indian party as of the date of the last audited balance sheet.However, in case the financial commitment exceeding USD $ 1 billion in a financial year, the same would require prior approval of RBI.

- The indian party should not be on the reserve bank of india’s exporters’ caution list / list of defaulters.

- An indian party may extend a loan or a guarantee to or on behalf of the JV/WOS abroad only if there is already existing equity participation by way of direct investment in such an overseas entity.

- If there is no equity holding of the indian party, then a loan and guarantee can be granted by way of rbi approval.

- The valuation of shares of the company outside india shall be made by a chartered accountant or a certified public accountant.

- However, if the amount is more than USD 5 million, the valuation of the shares shall be made by a category i merchant banker registered in/outside india.

- Indian party routes all the transactions relating to the investment in a JV/wos through only one branch of an authorised dealer(ad) to be designated by the indian party.

Where the conditions prescribed under the automatic route are not fulfilled, the | jv/wos INDIAN PARTY IS REQUIRED TO SEEK PRIOR APPROVAL OF RBI BEFORE MAKING SUCH AN INVESTMENT. THE APPROVAL SHALL BE MADE, BASED ON THE FOLLOWING FACTORS – 1. PRIMA FACIE VIABILITY OF THE JV/WOS OUTSIDE INDIA; 2. CONTRIBUTION TO EXTERNAL TRADE AND OTHER BENEFITS WHICH WILL ACCRUE TO INDIA THROUGH SUCH INVESTMENT; 3. FINANCIAL POSITION AND BUSINESS TRACK RECORD OF THE INDIAN PARTY AND THE FOREIGN ENTITY; 4. EXPERTISE AND EXPERIENCE OF THE INDIAN PARTY IN THE SAME OR RELATED LINE OF ACTIVITY OF THE JV OR WOS OUTSIDE INDIA. |

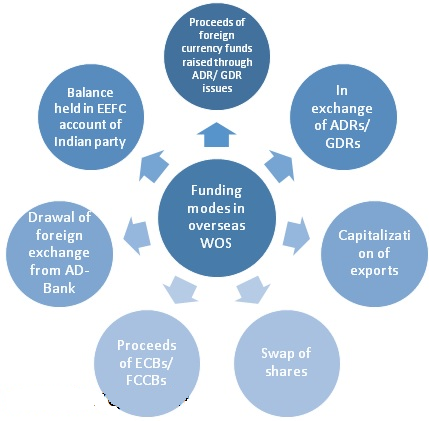

SOURCES OF FUNDS

- An Indian party may, with prior approval of RBI, undertake financial commitment without equity contribution in JV / WOS provided it’s as per the business requirement of the Indian party and also as per the legal requirement of the host country.

- “Financial commitment” as defined in regulation 2 (f) of interchange MANAGEMENT (TRANSFER OR ISSUE OF ANY FOREIGN SECURITY) REGULATIONS, 2004 means the number of direct investments by way of contribution to equity, loan and 100 percent of the number of guarantees and 50 percent of the performance guarantees issued by an Indian party to or on behalf of its overseas venture Company or Wholly Owned Subsidiary

- Proposals from the Indian party for undertaking financial commitment without equity contribution in JV / WOS could also be considered by the depository financial institution under the approval route supported the business requirement of the Indian Party and legal requirement of the host country during which JV/WOS is found.

- Accordingly, an Indian party must approach RBI through its AD bank to induce the approval for subscribing to the shares inconsiderately.

For more reading: setting-up subsidiary outside India

Also read more: Basic Document – filling FC-TRS FORM with RBI

TRANSFER BY WAY OF SALE OF SHARES OF JV/ WOS OUTSIDE INDIA

An Indian Party may transfer by way of sale to a different Indian Party or to a resident outside India.

Any share or security held by it in a very JV/ WOS outside India subject to the following conditions:

- The sale doesn’t end in any write-off of the investment made;

- In case shares of overseas JV/ WOS are listed, the sale is to be effected through stock exchanges;

- If shares of overseas JV/ WOS aren’t listed and shares are disinvested by a personal arrangement – share price mustn’t be but the worth derived by CA/ CPA;

- An Indian Party mustn’t have any outstanding dues from the overseas JV/ WOS;

- The overseas JV/ WOS has been operative for a minimum of one full year and therefore the APR along with audited accounts for that year has been submitted to order Bank;

- An Indian Party isn’t under any investigation by CBI/ DoE/ SEBI/ IRDA or the other regulatory agency in India.

Further, An Indian Party may disinvest, without prior approval of the bank, in any of the under noted cases where the quantity repatriated after disinvestment is a smaller amount than the initial amount invested:

The Indian Party shall make sure that the sale proceeds of shares/securities shall be repatriated within 90 days from the date of sale of shares/securities and therefore the documentary evidence to the present effect shall be submitted to the RBI through the designated AD bank.

RESTRICTIONS ON FORMING STEP DOWN SUBSIDIARY (SDS) COMPANY

- There are not any restrictions on entities having JVs/WOSs abroad putting in place second-generation operating companies (step-down subsidiaries) within the general limits applicable for investments under the automated route.

- However, companies wishing to line up step-down operating subsidiaries to undertake financial sector activities will go with the extra requirements for direct investment within the financial services sector.

- The provisions of Notification No. FEMA 120/RB-2004 dated July 7, 2004, as amended from time to time, managing transfer and issue of any foreign security to Residents don’t permit an IP to line up Indian subsidiary(s) through its foreign WOS or JV nor do the provisions permit an IP to accumulate a WOS or invest in JV that already has direct/indirect investment in India under the automated route.

However, in such cases, IPs can approach the banking concern for prior approval through their Authorized Dealer Banks which can be considered on a case-to-case basis, betting on the merits of the case.

| ONE TIME | • THE INDIAN COMPANY INTENDING TO MAKE A DIRECT INVESTMENT UNDER THE AUTOMATIC ROUTE IS REQUIRED TO SUBMIT FORM ODI WITH THE DESIGNATED BANK, DULY SUPPORTED BY THE DOCUMENTS LISTED THEREIN. |

| RECURRING | • SUBMIT ANNUAL PERFORMANCE REPORT OF OVERSEAS ENTITY TO THE RESERVE BANK OF INDIA THROUGH AD BANK. • SUBMIT ANNUAL RETURN ON FOREIGN LIABILITIES AND FOREIGN ASSETS. • REPORTING OF THE DETAILS IN RESPECT OF DECISIONS TAKEN BY THE JV/WOS IN RESPECT OF DIVERSIFICATION OF THEIR ACTIVITIES /SETTING UP OF STEP-DOWN SUBSIDIARIES/ALTERATION IN ITS SHAREHOLDING PATTERN WITHIN 30 DAYS OF SUCH ALTERATION. |

| EVENT WISE | • RECEIVE SHARE CERTIFICATES OR ANY OTHER DOCUMENTARY EVIDENCE OF INVESTMENT IN THE FOREIGN JV / WOS AS EVIDENCE OF INVESTMENT AND SUBMIT THE SAME TO THE DESIGNATED AD WITHIN 6 MONTHS. • REPATRIATE TO INDIA THE AMOUNT IN RESPECT OF DIVIDENDS, ROYALTY, TECHNICAL FEES, ETC, AND THE SAME BE MADE WITHIN 60 DAYS OF THEIR DUE DATE. • WHERE THERE IS DISINVESTMENT, THE SALE PROCEEDS IN RESPECT OF SHARES AND SECURITIES, IS REQUIRED TO BE REPATRIATED TO INDIA IMMEDIATELY ON RECEIPT THEREOF AND IN ANY CASE NOT LATER THAN 90 DAYS FROM THE DATE OF SALE OF THE SHARES /SECURITIES AND DOCUMENTARY EVIDENCE TO THIS EFFECT SHALL BE SUBMITTED TO THE RESERVE BANK THROUGH THE DESIGNATED AD. |

INVESTMENT IN FOREIGN SECURITIES ASIDE FROM BY WAY OF DIRECT INVESTMENT

- By Way Of – Gift/ Inheritance/ ESOP

- As per regulation 22 of exchange Management (Transfer or Issue of Any Foreign Security) Regulations, 2004, General permission has been granted to a person resident in India who is an individual: –

- to accumulate foreign securities as a present from any individual resident outside India; or to acquire shares by way of inheritance from an individual whether resident in or outside India.

- An individual resident in India being a person who is an employee/ director of Indian office/branch of a far-off entity/ subsidiary of a foreign entity in India/ Indian company during which foreign entity has direct/ indirect equity holding, may accept shares offered by such foreign entity provided that:

- the shares under the ESOP scheme are offered by the issuing company globally on a uniform basis; and

- The annual return is required to be submitted by the Indian company to RBI, through AD Bank providing details of remittance/ beneficiary, etc.

- by way of bonus or right shares issued in respect of the foreign securities already held by them.

- to acquire shares under the Cashless Employees option Scheme issued by an organization outside India provided it doesn’t involve any remittance from India

| *MEANING OF PRI (PERSON RESIDENT IN INDIA): –A PERSON RESIDING IN INDIA FOR MORE THAN 182 DAYS DURING THE COURSE OF THE PRECEDING FINANCIAL YEAR. HOWEVER, IT DOES NOT INCLUDE A PERSON WHO HAS COME TO OR STAYS IN INDIA, IN EITHER CASE, OTHERWISE THAN: (A) HE HAS COME FOR OR TAKING EMPLOYMENT IN INDIA (B) FOR CARRYING ON BUSINESS OR VOCATION IN INDIA (C) FOR ANY OTHER PURPOSE, IN SUCH CIRCUMSTANCES AS WOULD INDICATE HIS INTENTION TO STAY IN INDIA FOR AN UNCERTAIN PERIOD. | *MEANING OF PROI (PERSON RESIDING OUTSIDE INDIA): –PERSON RESIDING OUTSIDE INDIA MEANS A PERSON WHO IS NOT COVERED AS PER THE DEFINITION OF PRI (PERSON RESIDENT IN INDIA). |

COMPLIANCE REQUIREMENTS WHEN SHARES ARE ACQUIRED WITHOUT CONSIDERATION

- The Indian Party Should Report the main points of the acquisition of securities by way of gift/ inheritance within 30 days of such acquisition.

- Where the ESOP is issued to an employee of an Indian branch/ subsidiary, the same is required to be reported in form as annexed below as Annexure A.

For more reading: Advantages and know details about Startup India Schemev

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}