Page Contents

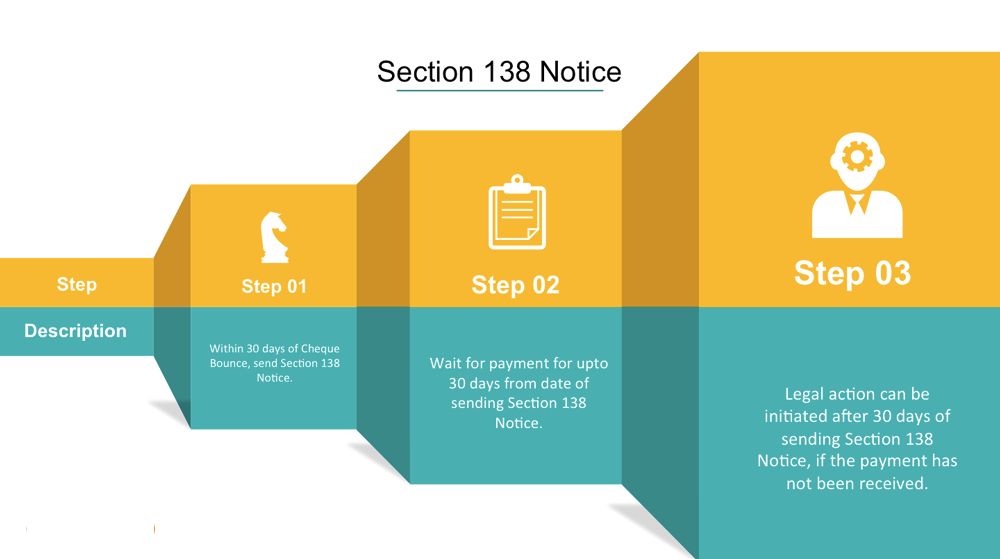

To initiate prosecution under Section 138, three condition precedents need to be fulfilled as below:

The prosecution can be launched against the payor and in the case where a company has committed an offence under Section 138, then not only the company but also every person who at the time when the offence was committed, was in charge of and was responsible to the company shall be deemed to be guilty of the offence and be liable to be proceeded against.

The Cabinet has approved an amendment to current law to allow for payment of an interim compensation in cheque dishonour cases with a view not to allow unscrupulous elements holding payments, pending long trial, sources said. An amendment to the Negotiable Instrument Act will allow a court to order for payment of an interim compensation ( interim compensation can be an amount not exceeding 20 per cent of the amount of the cheque) to those whose cheques have bounced due to dishonouring parties.

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}