Page Contents

Below are the activities which is treated as supply for charging GST in real estate sector

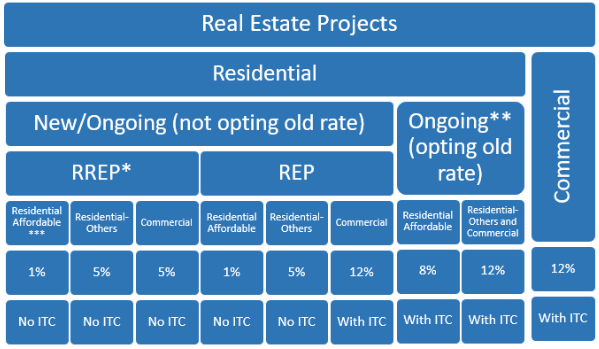

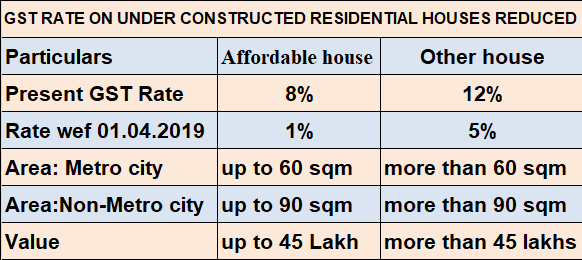

New GST Rate apply With effect from 01.04.2019 on supply of construction service which involving property in land transfer shall be as Bellow –

| Kind of Apartment | Rate of GST which is after deduction of value of land |

| Residential Apartments | |

| · Non affordable Residential Apartment | 5 Percentage without Input tax Credit on whole consideration |

| · Residential Apartment which is affordable | 1 Percentage without Input tax Credit on whole consideration |

| Shops, offices, godowns etc kind of Commercial Apartments | |

| Other than Residential Real Estate Project (RREP) | 12 Percentage without Input tax Credit on whole consideration |

| Residential Real Estate Project (RREP) | 5% Percentage without Input tax Credit on whole consideration |

Basic means of affordable residential apartment is a kind of apartment for residential in a project which

Definition of Residential Real Estate Project means a real estate housing project which

To be Notes:

Popular Articles :

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

Overview Taxation of Firms & LLPs in India Key aspects of taxation of partnership firms and limited liability partnerships are… Read More

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

{kind=link}

{kind=link}

{kind=link}