Free CIBIL Update & major factor which may affect and help in improving CIBIL Score

TransUnion CIBIL Ltd., formerly known as the Credit Information Bureau Ltd., is one of India’s leading credit information firms. It was founded in 2000 and is widely referred to as the CIBIL credit agency

The Office is approved by the RBI and is governed by the Credit Information Companies (Regulation) Act of 2005. It has more than 2,400 members, including banks, financial institutions, non-profit financial companies, and housing finance firms. The credit bureau holds more than 550 million payment records for consumers and businesses.

What is the credit score or CIBIL?

- The CIBIL score represents your creditworthiness, which indicates whether your financial credibility is favorable or unfavorable.

- The scale is 300-900. This rating is determined by taking into account a few factors, such as the actions of loans, the history of repayments, the types of loans used, defaults in EMI or in repayment, etc.

- The greater the ranking is 900, the more likely you are to be approved for a loan or a credit card. A higher score suggests that you have been a good borrower and that you have a decent credit record.

- A score of 750 and above gives you greater access to credit and credit cards as per the basic information.

Also Read: Know What is a Credit Rating?

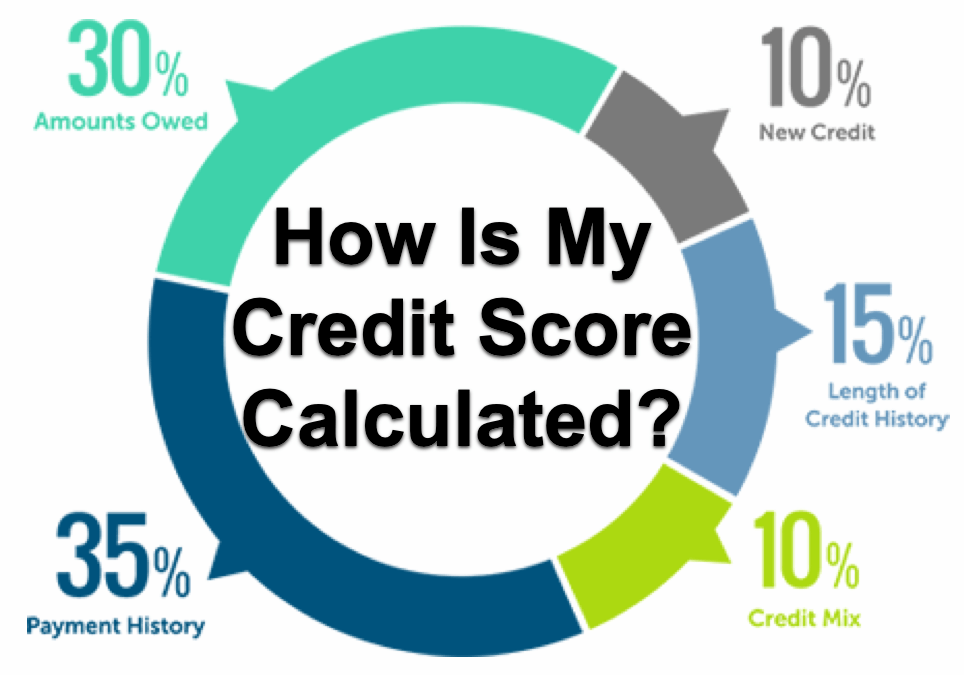

How does your credit score consist?

In the CIBIL SCORE, only 4 major factors consists are hereunder :

| History of payment | 30 percent |

| Other Reasons | 20 percent |

| Exposure of credit | 25 percent |

| Type and amount of credit | 25 percent |

Recognize how credit agencies measure your CIBIL score

To measure a CIBIL score, most agencies use financial position, loan type, and debt-to-credit ratios, etc. If you want to get an incredible CIBIL score, knowing the main information of how your score is measured is.

- Each authorized Company has its own way of calculating the credit score. But,

- the most important components measured are your financial background (which shows how successful you are in making the payments) and

- your amount of debt (represents how much credit you apply and how much you use).

- Combined these two reflect about 2/3 of the credit score.

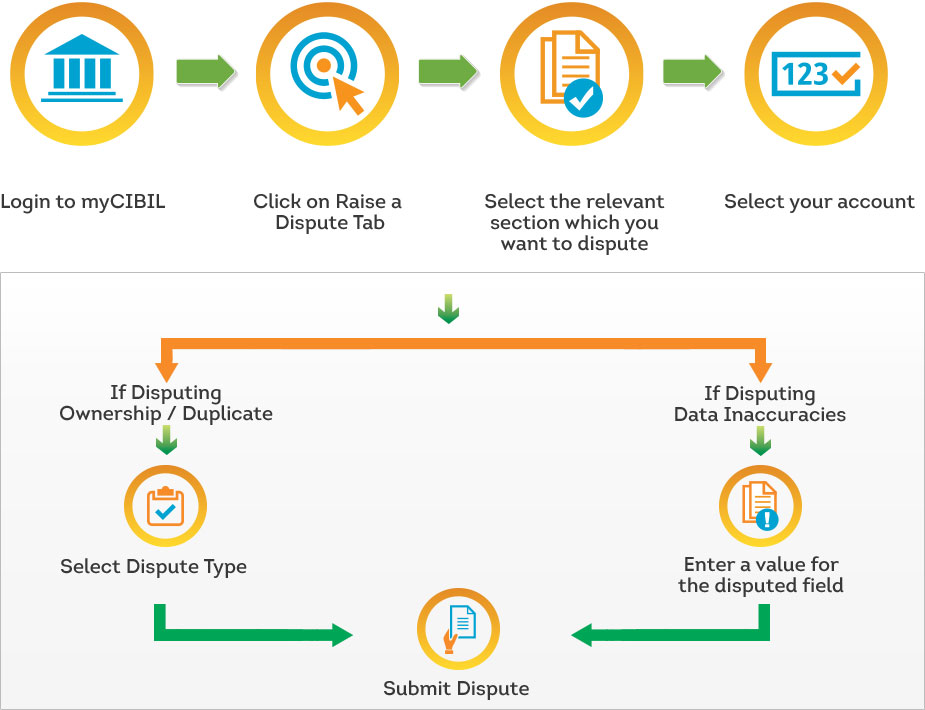

Check your free CIBIL report

- RBI was made mandatory in 2017 for all credit reporting agencies in the country to include CIBIL Report, to give customers one free credit score report per calendar year per person.

- You will get a free download of your CIBIL survey by accessing the official CIBIL website.

Several factors that affect your credit score

-

Past History of repayment of the loan, EMI, interest, etc.

- A significant part of your CIBIL score is paying your old outstanding bills on time.

- Payment background is one of the key variables impacting the CIBIL ranking.

- Late payment will diminish your credit score and will continue to appear on the record for up to seven years.

- Paying the credit card payments, as well as loaning EMIs on time should be a priority. A default in EMI is not a positive thing.

- When they look at your paper it pops out to a borrower. Default would have a larger effect in modern times than an EMI option more than two years earlier.

- 30-day delinquency will decrease the CIBIL score by 100 points according to a recent CIBIL study (as stated by Financial Express).

- If you appear to fail to make the payments by the due date, set up SMS or e-mail alerts or send standing orders about how to automatically subtract the EMI or credit card number.

-

Maintaining your total Debt Ratio

- Your debt is the biggest cause for your CIBIL, either great or worse. The aggregate amount of debt you have at a particular point in time would have a huge impact on your CIBIL ranking.

- The credit utilization ratio is the amount of credit you’ve used in comparison to your total credit limits.

- To get a decent score, you will have a low credit utilization ratio at all times. It is best to use up to 30 % of the overall credit limits as per experts. Going into more debt at once will result in a poor CIBIL ranking.

- This is that if you take too many loans at once your Income-to-debt ratio will drop and will affect your CIBIL. So choose not to take more loans at the same time, to keep a decent credit score.

- Take as much as you can quickly cover, without disrupting your schedule. In the first place consider the repayment schedule.

- It is equally important to handle your debt diligently and retain a decent credit score. Until you take up a loan then intend to repay it, if you can easily repay it then just go for it.

- The kind of loans you make use of is a significant element in deciding your Credit Score.

- If you are strong on unsecured, high-interest loans such as credit cards or personal loans, so it works against you.

- However, if you have a combination of secured loans, such as Home Loan and Car Loans, then it would have less negative effects.

-

Maintain your Outstanding credit balance as low as possible

- To calculate your score, credit bureaus look at the ratio of your total credit balances to the amount of your debt exist.

- It is advised to use a credit card for emergency purposes only, and to pay off the debt as quickly as possible your credit card balances should be under 30 % of the overall credit cap to be on the better side and for healthy investments.

- When your debt crosses this cap, it is adversely expressed on your credit report.

- The higher the credit card balance is the greater the risk of not making full payment and missed payments as well. Aim to keep the credit card balance low which may prevent such a case.

- However, to maintain a decent CIBIL score, it is still best to use your credit card to make the most of the transactions.

- It’s very essential to keep a decent credit score along with regular payments holding your credit card balance down.

-

Time to time check revaluated CIBIL Report

- You should keep reading frequently on your credit report. A summary of your credit score and survey from credit bureaus can be quickly viewed. Those agencies only have one CIBIL Report-free report every year.

- If you notice certain defects, you will instantly get them rectified.

- Falsely reported inaccuracies may be delayed or misrepresented personal information, etc. Daily tracking of the CIBIL score is of such interest that many of you don’t know about it.

- Chances of that your Credit records can contain errors or faults. These defects are very necessary for rectification and correction.

- This can occur because the provider avoids delivering the notification or it can also occur due to inaccurate details being implemented.

- These errors will harm your CIBIL and even impact your potential creditworthiness..

- There are several advantages of having strong CIBIL, which means getting a loan accepted at a cheaper rate of interest and you can even save money on any of the loans’ down payments.

- So it becomes important to keep a decent credit score to take advantage of such advantages.

-

Complete your full inquiries about your credit and its Score.

- Ignore numerous credit requests within a quick time period. Therefore, it is recommended that you just ask for credit when you genuinely need it.

- When you ask about a loan or credit card to a bank or financial institution, the borrower will take out the CIBIL report.

- Such an investigation is considered a “hard investigation,” because it impacts the ranking adversely. Meanwhile, it’s called a “soft investigation” when you review your own score or study.

- You should review your report various times and it won’t impact your CIBIL score as soft inquiries don’t show on your record.

- You prefer to apply for loans or credit cards to several lenders when you need credit urgently.

-

Size and amount of borrowing as per requirement only.

- A decent credit history helps make the score higher. It indicates you have good credit management experience. Lenders like to give loans to those with a rich background, as it makes it easy to judge yourself as a borrower.

- It is also best to stop closing old cards as you would miss out on the long credit history and related positive lending behavior. Getting a good mix of credits is critical.

- Having a positive, stable, and unsecured credit balance helps raise your CIBIL ratings. You need to make sure you don’t get heavily secured loans or unsecured loans and strive to keep a decent balance of both instead.

-

Keep maintaining your previous credit cards if possible.

- Maintaining your older credit cards will contribute a substantial amount to your credit score. This is because old credit cards help to keep the credit history going continuously.

- This will increase / good credit score. But it’s recommended to do this for as long as you can pay the bills on time. Otherwise, it could function in the negative.

-

Prepare the right mix between secured and unsecured credit

- You should really get a good balance of credit accounts. If you only have one type of credit account, your score may be lower.

- For instance, secured loans such as home loans or car loans boost your credit score as they display your financial track record over a long period of time and illustrate your dedication and willingness to repay when you take out a loan by promising your loan.

- On the alternative, having only unsecured debts or personal loans, credit card debt in your financial background will drag down your score too much.

- Stop applying for new credit too frequently: Applying for a new credit account will also have a negative effect on your credit score.

Read also Know Why You should use Credit Card?

Factors that help you to improve your credit score

-

Use credit lines responsibility

- Any money out of a credit card is borrowed money by the end of the day. Depending on the form of the credit line and the lending actions you need to return it to the lender, with or without interest.

- But make sensible use of your credit card, loan amount, or some other kind of borrowing. Don’t ever buy or spend more than you can afford to pay back. This could drive you into a debt trap.

-

Ignore late payments and forget about payment

- This repayment activity will also be disclosed to the credit agencies, impacting the ranking, aside from being paid late payment fines for the late payments.

- If you have to make several payments via credit card and loan EMIs, it is best to set up payment notifications or due date notices and keep them more coordinated.

- Never hesitate to make your payment this way. You will also be able to set up a direct debit agreement with your loan where the contributions are immediately withdrawn on the due date from the savings / current account.

- You never have to think about remembering due dates, or about late payments or missing payments.

-

Maintain less credit utility ration

- Ideally, you should not exceed 30 % of the overall credit card cap listed earlier by VAS.

- This is highly important in the future if you are applying for a home loan.

- The banks will calculate the debt-to-income ratio (DTI) while applying for a home loan. This measure assesses your gross liability to your overall sales.

- If your debt reaches 50 % of your earnings, banks are more likely to deny your offer. Another explanation you should have a good credit usage level is not to be greedy for the credit.

- If your credit lines incurred any of your bills you will look like a creditor who can not handle their bills on his own.

-

Always close the account instead of settling

- If in the past you have defaulted on any transactions that will be mirrored in your credit report and carry down your CIBIL ratings.

- Be sure the outstanding balance is paid off and close the account instead of settling for a payout.

- You should make sure the account is having a ‘locked’ status. Often, it is safe for the loan to get a formal certificate of closing from the provider.

-

Stability

- For years on the go, you need to be prepared and disciplined to retain a perfect credit score. Pay your bills every month even before the due date, and keep a close eye on your revenues and expenses.

- And by setting up a proper plan will you be able to monitor your savings consistently over the years and meet your loan repayment responsibilities.

- Wait for the credit score to rise

- Time is a crucial part of the equation to get a decent credit score particularly when you restart after your credit score decreases due to your past mistakes Once you start working on a credit enhancement plan,

- it can start to steadily show as an increase in your score beginning at least 6 to 8 months out.

- You’ll need a good credit history of at least 5-7 years before you can reach the top score of 850 +.

- Part of measuring your credit score takes into account the era of the oldest credit account.

- But stop transferring accounts or closing old accounts.

- Popular blog:-

-

RAJPUT JAIN & ASSOCIATES

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}