Page Contents

What’s the ESOP?

ESOP or Employee Stock Option Plan – also referred to as Employee Stock Ownership Plans in India – is a scheme by which a company allows its employees to purchase shares of the company.

In some cases, a foreign holding company offers such an option to employees of an Indian subsidiary. Under that same scheme, employees are given choices which enable the employee to purchase the stock at a rate just below the prevailing market value of the stock or provide the employee for a certain proportion of his or her compensation in the company’s stock.

ESOPs and RSUs have become increasingly common in India, with jobs starting to gain wide acceptance. Several multinational companies with employees in India are also going to offer ESOPs. Let’s see how ESOPs are required to pay taxes.

ESOPs are taxed on Two occasions –

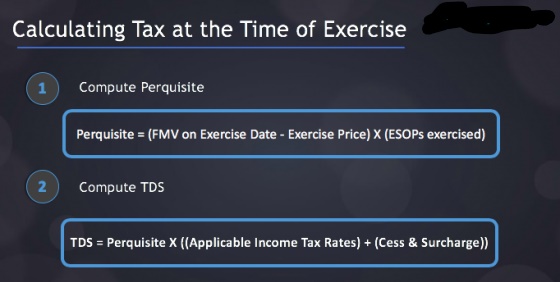

At the time of exercise, as a perquisite. : In case employee exercises the ESOP Option, he or she essentially agrees to purchase; the difference between the Fair market value (on the exercise date) & the exercise price is taxed as perquisite.

On this perquisite, the employer deducts Tax deducted at sources. This amount is shown in Form 16 of the employee & is included under the head of the total Income from salary in his income tax return.

In the event that the employer did not deduct TDS and pay it to the Govt as stated above, the employee should pay the tax on the very same dates. In these cases, the tax rates and the TDS rates shall be the ones applicable for the year that the ESOP has been allotted.

Budget 2020 amendment: from the year 2020-21: Employees receiving ESOPs from qualified start-ups do not have to pay tax in the year they exercise the option. The TDS on the ‘prerequisite’ is deferred from the following situations:

At the time of the employee’s sale – as a capital gain: In case of employee may choose to sell the shares as soon as they are purchased by the employee. If the employee sells such shares, there will be another tax event. The difference between the sale price and the FMV at the exercise date is taxed as capital gains.

Exercise price ——-<Perquisite>——-FMV on exercise date——<capital gains>——sale price

Advance tax regulations require that your tax fees (predicted for the whole year) be paid in advance. Advance tax is paid in instalments. Whereas the employer deducts TDS when you exercise your choices, you may have to pay advance tax if you have obtained capital gains.

For the 2020-21 financial year, individual instalments are due on 15 June, 15 September, 15 December and 15 March. You have to pay 100% of your taxes by March 15th.

Non-payment or late payments of advance tax results in criminal interest pursuant to Sections 234B and 234C.

Even then, it may be difficult to estimate the tax on capital gains and the advance tax on deposits during the first few instalments if the sale takes place later in the year. Consequently, when advance tax instalments are paid, no criminal interest is charged if the instalment is short due to capital gains. Residual instalment (after the sale of shares) of advance tax so if due must include a tax on capital gains.

Some other aspects must also be considered in order to accurately calculate the sales tax of ESOPs.

The rate at which your capital gains are taxed depends on the length of their holding. The holding period shall be measured from the time of exercise to the date of sale. Equity shares listed on a recognised stock exchange (where STT is paid on sale) are considered to be long-term gains when held for more than one year. If sold within one year, short-term gains are considered. Currently, long-term earnings on listed equity shares are tax-free, while short-term earnings are taxed at 15%.

In the event that you have incurred a loss, you are permitted to bring forward short-term capital losses in your tax return and modify and set them against the gains in the coming periods.

When you have bear the Long term loss on equity shares is a dead loss – i.e no use of it and has no income tax treatment of it, simply because capital gains on it is also not taxable as well.

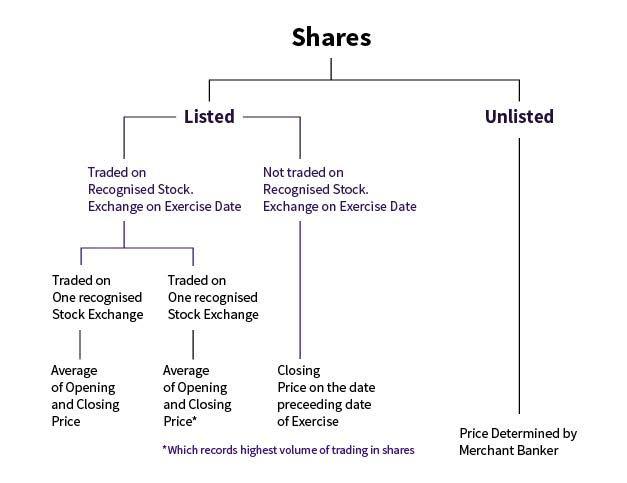

The Income Tax Act distinguishes between the tax treatment of listed and unlisted shares. The tax treatment for shares not listed in India or listed outside Is still the same because. That is, if you own the shares of an American company, they won’t be listed in India. They may be regarded unlisted for the purpose of taxes in India. Shares are short-term if held for less than 3 years and long-term if sold after three years. The period of holding starts from the exercise date up to the date of sale. Throughout this case, short-term earnings are taxed at income tax slab rates, and long-term earnings are taxed at 20% after cost indexation.

Your income is taxable in India on the basis of your residence status. If you are a resident, all your income from everywhere in the world is taxed in India. And from the other hand, if you are a non-resident or resident but are not ordinarily resident and have exercised your choices or sold your shares, you may have to pay tax outside India. You may be able to reap the benefits of DTAA in such a case. It ensures that your income is not taxed twice.

Some many disclosures have been introduced to the tax return form for foreign assets. If you own ESOPs or RSUs of a foreign company, you may have to disclose your foreign holdings in accordance with the FA schedule of your income tax return. above disclosure in the income tax return needed to be applicable to a resident Assesse.

Where assessee was an ‘ESOP Trust’ created by settler-company for implementing its ESOP scheme the assessee was merely acting as ‘Special Purpose Vehicle’. Shares held by the assessee were in fiduciary capacity and assessee did not have absolute rights over those, so these shares could not be categorized as business assets. Thus, gain arising to the assessee on the transfer of shares to employees of settler-company was to be treated as capital gain and not as business profits – [2015] (Mumbai – Trib.)

On the date of termination, the employee shall have the right to exercise his opportunity or to purchase stocks. However, there is no necessity for the employee to choose not to exercise his or her option. There shall be no tax consequences for the employee in a quite case.

Employee Stock Option Plan is a way to reward employees by offering Co Shares at a discounted rate. NRI Employee Stock Option Plan Shares come under the Non-PIS transaction & are taxable in India.

The Mumbai Bench of Income Tax Appellate Tribunal (ITAT) ordered HDFC Bank’s Dubai-based manager to pay tax on ESOPs in India. Unnikrishnan V. S., the assessee, He is an individual who’s also an employee of HDFC Bank Limited, Mumbai, and is currently serving in Dubai’s HDFC Bank Representative Office. The assessee’s status is as the non-resident. During the financial cycle in reference, the assessee exercised the options assigned to the assessee by HDFC Bank Limited on 27 June 2008 (50%) and 27 June 2009 (50%) respectively (50 %).

Once these options have been exercised in respect of 18,500 shares. The grant value for these options was Rs 219.74 per share, whereas its market price varied between Rs 507.40 to Rs 659, as at the date of exercise of the option. The perquisite value of these options is Rs.72,77,320, the gap in the market value of the shares with respect to the grant price of the shares. It was in this sense that, in respect of the exercise of options, HDFC Bank Limited deducted the tax at source on the said perquisite amount.

However, on 28 August 2013, while filing income returns, declaring total income of Rs 78,50,010 and requesting income tax refunds of Rs 21,46,410, the assessee claimed relief of Rs 20,44,855 accordance with section 90 .

When the income tax return was collected for inspection and this claim was further examined, the assessee submitted that “although the income from the ESOP perquisite was not chargeable to Tax in India, due to limitations in reporting and disclosure of the said income in the tax return, ” the assessee had to report and disclose the said income in its form, as reflected in the return of income filed by the assessee and seek a refund of TDS by the employer(HDFC Bank).

The employee of the bank also made an alternative request, stating that these amounts cannot be taxed in India, as provided for in the Indian-UAE Tax Treaty. Although rejecting the HDFC Bank employee’s contention that the ESOPs related to jobs in Dubai and income (perquisite value) did not accrue or exist in India and were therefore not taxable in India, the Coram headed by Vice President Pramod Kumar and Saktijit Dey rejected the HDFC Bank employee’s contention that Article 15 of the India-UAE tax treaty provides for taxation of the ESOP benefit in the country where the related employment benefit was accessible under income taxable in India. Thus, also under the tax treaty, it relates to services carried abroad as the ESOP income in India will be taxable in India.

Its always been a high priority for startups to carry amazing talent to a high price salary. This is where ESOPs come in to help entrepreneurs get the right kind of talent, even if they can’t pay the extra salaries that companies pay. It is because startups can provide employees with a bit of company or ESOP over a specific time period called the vesting period. Employees are allowed to practise their ESOPs after the vesting period.

The stock price provided to employees under ESOP (exercise price) is generally less than the market rate value of the stock.

Presently, while the Finance Bill 2020 is yet to be implemented, ESOPs are taxed twice pursuant to section 17(2) of the Income Tax Act.

Not everyone companies and companies giving ESOPs advantage from this move is advantageous to certain start-ups that meet specific conditions-

i. Start-ups must be incorporated between 01/04/2016 and 31/03/2021.

ii. The total turnover of the start-up must be less than 100 crores for the year in which the advantage is sought.

iii. It must be certified as a qualified start by the Inter-Ministerial Board of the Govt.

The data in the public domain recommend that there are about 250 start-up companies holding certificates from the Inter-Ministerial Board. No employees affected by this & the amount of cash that such employees will be able to retain the amount of income deferment for the Govt is not in public domain.

Tax treatment in respect of contributions made to and payment from various provident funds are summarized in the table given below

More read for related blogs are:

For query or help, contact: singh@carajput.com or call at 9555555480

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

Understanding Form 16, Form 16A & Form 26AS: A Complete Guide for Taxpayers When filing your Income Tax Return (ITR),… Read More

CFO Cum whole-time director? ROC Gwalior Says No in EKI Energy Services Case Corporate governance is built on the principle… Read More

Toughest Exams in India: More Than a Test of Knowledge, A Test of Character Every year, millions of students and… Read More

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}