Page Contents

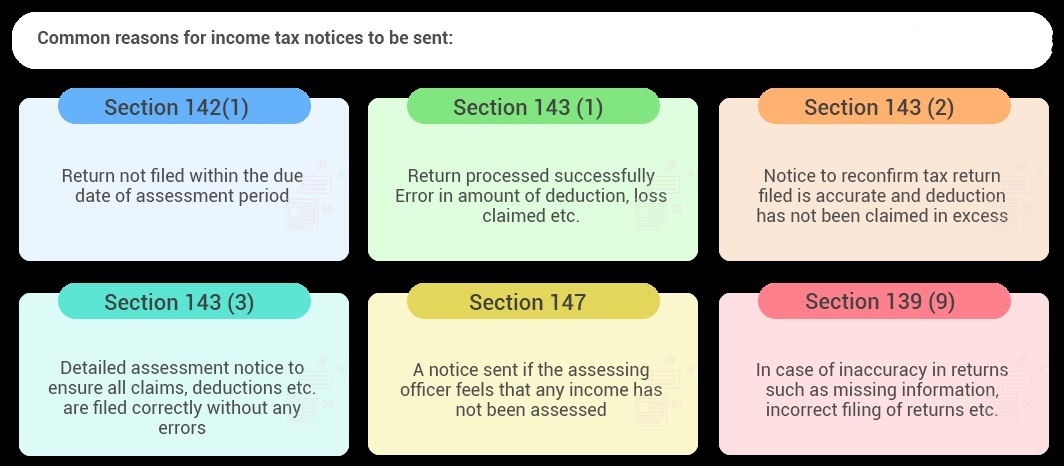

Section 142(1) Notice is generally intended to be used to invite taxpayers to provide the documents and details.

Section 143(1) allows for three different forms of notices to be sent as follows:

The IT returns need to be fully revisited in most corrective actions against a defective notice. As a result, in order to generate a correction IT Return, the tax preparation will need all of the papers used in the initial IT Return preparation.

To ensure that the response to the defective notification is approved, the revision / correction must be thoroughly scrutinized.

To respond to the defective notification provided under Section 139(9), follow the steps below :

The measures below should be performed if you receive a notice under any of the above mentioned sections.

If you receive a notification from the Income Tax Department, you must understand why it was sent. For a variety of reasons, notices may be sent.

For example, notices may be delivered in response to the Income Tax Department’s requests for information and documents.

In this situation, you must submit all of the necessary information. If the ITR contains a mistake, notices may be sent to correct the problem.

To avoid potential penalties, you should correct any errors in your return and respond to the notice within the time frame specified by the income tax department.

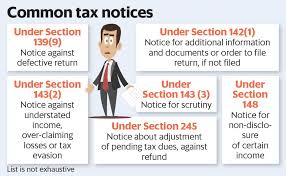

The following are the most common reasons that you might receive a tax notice:

The department processes the return and gives intimation under section 143(1) once it is filed. Details of the income tax return provided by the Assessee and calculated by the income tax departments are included in the income tax bulletin.

It may be sometimes that the Assessee takes tax, deduction, etc. credit incorrectly or a tax credit may not be provided by the department.

An error that is apparent in the record may be corrected in accordance with Section 154 of the Revenue Tax Act. Some of the mistakes that can be corrected include:

If the Assessing Officer considers the Assessee’s return to be defective, the Assessee may, by issuing a notice of income tax u/s 139(9) in the Income Tax Act, report the defect to the Assessee by giving us a chance of rectifying the defect within a period of 15 days. In certain cases where an income tax notice is issued pursuant to Article 139(9):

Intimation under Section 143(1), also known as Income-tax Notice 143(1), is the first stage in which all Income-tax returns are processed to correct arithmetic errors, internal inconsistencies (meaning bifurcation of a section such as Chapter VI A, etc.), tax calculation, and tax payment verification.

At this time, no income verification is performed. It is completed using computerised processing with no human intervention.

This is an intimation/income-tax notice for the processing of the assessee’s income-tax return. This income-tax notification is usually received as a pdf file via email from the Centralized Processing Centre (CPC) in Bengaluru.

This Income-tax notice is delivered to the Assessee to advise them that the Income-tax authorities seek to modify the outstanding tax demands of an earlier year from the refund due.

The demand may be for an earlier Assessment Year, and when a refund is claimed, it is offset against the demand. The Income-tax Department cannot adjust the refund in response to demand on its own.

This notice is being sent to Assessee for this purpose. If you disagree with the adjustment, you may express your dissatisfaction via an online response from the Income-tax Department’s e-filing website.

The income-tax intimation under Section 245 will also include the time limit for responding, after which the adjustment will be considered final and no further action will be possible.

This income-tax notice is distinct from the income-tax notice issued under Section 143(1). this income-tax notice is being issued in order to elicit a response to the errors/incorrect claims/inconsistencies that are subject to adjustment under Section 143(1) (a).

When compared to Form 16, Form 16A, or Form 26AS, an income-tax notice u/s 143(1)(a) is an intimation from the Central Processing Centre (CPC) demanding clarification of the mismatch between the income and deduction.

If you agree with the mismatch, you’ll need to file an amended return. The online response must also be submitted using the e-filing website.

The income-tax intimation sent under section 143 (1)(a) will also specify the time limit for responding, which is usually 30 days from the date of the notice.

The purpose of this income-tax notification is to obtain certain documents and information from taxpayers. The goal of an income-tax notice is to obtain information about the assessee before making a determination.

An income-tax notification can be issued in both circumstances where a return has been filed and when a return has not been filed and the deadline for filing has passed. The following notice is sent to the assessee:

The documents required vary depending on the type of income-tax notice. However, the following documents are required to respond to any Income-tax notice:

However, in some cases, the case should be reviewed only by tax experts. As a result, after you upload a copy of your income-tax notice, our Tax Experts will evaluate it and come up with a possible solution. You will be requested for the relevant documentation based on this.

EXC -001 implies that you engaged in a transaction that was not permitted by the Income Tax Act. It applies to cash transactions totaling more than INR 10 lakh in a calendar month.

Is it possible for a salaried person to receive a notice from the Income Tax Department?

Yes, a salaried person will receive an income tax notice. The notice under Section 143(1) is an intimation that ITD sends to each taxpayer.

However, you may receive additional income tax notices if IT has reason to believe that you have concealed income or for any other reason.

If ITD issues a notice, it will be delivered by mail to your registered address.

You can verify notices you’ve received using the income tax site, but keep in mind that not all notices can be reviewed there; for all notices inquiries, go to the ITD and ask your question there.

Do I get an income tax notice if I make a current account transaction?

Yes, if there is a reason, the income tax department can issue notices for current account transactions as well.

The communication of proposed adjustment u/s 143(1)(a) of the Income Tax Act, 1961 refers to any information provided by the department indicating that they are proposing an adjustment to the refund claimed by you in your income tax return. Such an adjustment could apply to any outstanding demand from previous assessment years.

The Income Tax Department issued a discrepancy in notice under section 143(1), and the discrepancy can be favorable or unfavorable.

If a demand is legitimate, it must be met. If the refund is INR 100 or more, IT will certainly pay you.

If any error is apparent from the record, you may file a rectification u/s 154 (1) correcting errors: Select the ‘Rectification’ option from the drop down list after clicking on ‘e-file.’

A notice of scrutiny assessment under section 143(2) can only be given for a period of six months after the end of the financial year in which the return was filed.

If you do not react to an income tax notice, you may face a variety of repercussions, depending on the type of notice you get. Fines of up to INR 10,000 can be imposed, as well as imprisonment for up to a year.

After your return has been satisfactorily completed, the income tax department will send you an intimation letter / notice under section 143(1).

The information you provided at the time of the ITR filing is detailed and a corresponding column contains the details of the tax department.

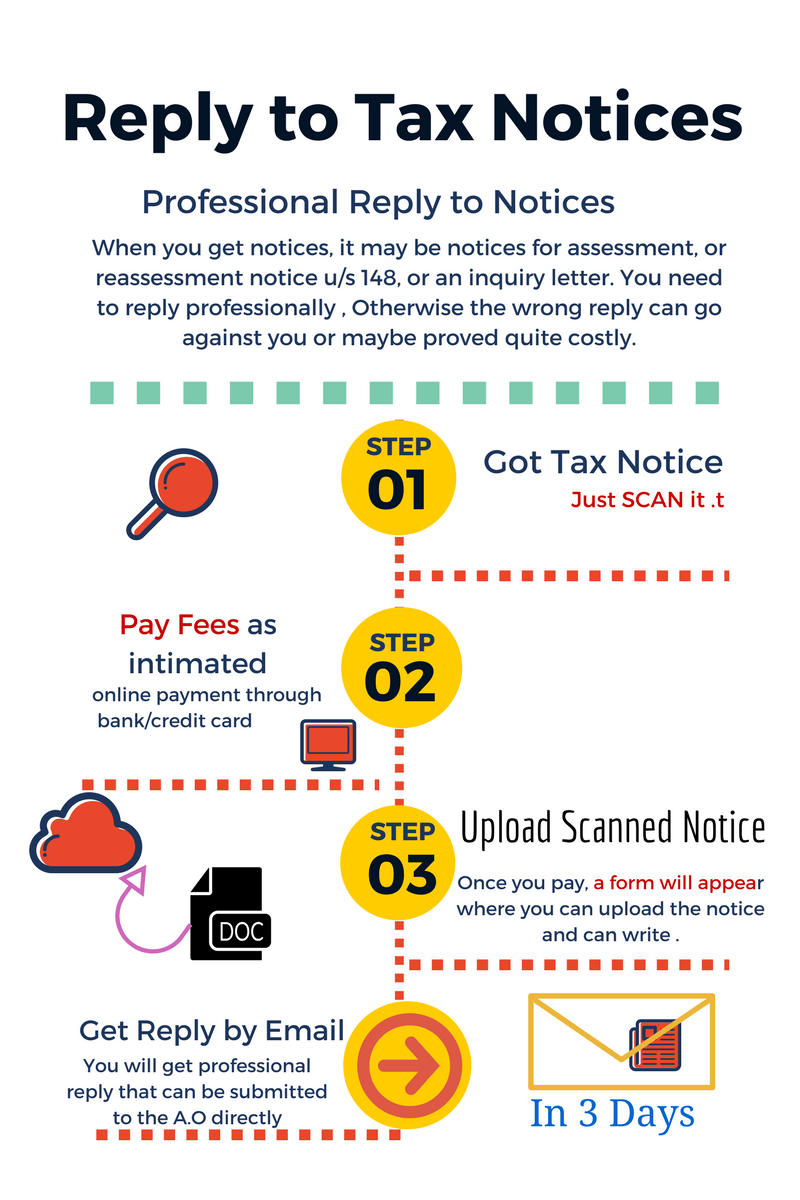

A tax notice may be responded online. You can visit the income tax department’s website which is used to submit your returns electronically. Log into your online account and respond to the notice that has been sent to you.

On demand, you can pay online your tax. You can visit the income tax department’s e-filing web site and login to your account.

Then, under the e-File option, you can check the amount of outstanding tax demand under Response to Outstanding Tax Demand.

Then, in the Pay Tax column, select Click Here. You will be directed to the NSDL website, where you can complete an online form and pay the tax on demand.

If you do not respond to the notice within 30 days, the income tax department will make the adjustment if there is an outstanding demand without providing you with another chance to respond.

ITRV (acknowledgement) is sent to your registered email address shortly after you file your ITR.

Otherwise, you can download it from your account on the official website of Income Tax India.

To respond to an outstanding tax demand online.

Delhi ITAT held that the AO proceeded to initiate reassessment proceedings u/s. 147 of the Act and to issue notice u/s. 148 of the Act.

On the basis of borrowed satisfaction and without any application of mind and examination of the so called material and information received from the investigation wing to establish any nexus, even prima facie, with the such information. Pioneer Town Planners Pvt. Ltd vs. DCIT (ITAT Delhi)

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}