Page Contents

CBDT by exercising their powers u/s 119 of the Income-tax Act,1961 (Act), with the objective of easing the process of selection of cases for issue of notices related to assessment reopening u/s 148 of the Act, directed that there are specified categories of cases that can be considered as ‘potential cases’ for taking action u/s 148 of the Act for the Assessment Year from 2013-14 to 2017-18 by the Jurisdictional Assessing Officer (JAO). These are as follows –

(a).Reports on investigation provided by the Directorate of Income-tax.

(b) Reports on investigation of Directorate of Intelligence & Criminal Investigation.

(c) Cases from Non-Filer Management System (NMS) & other cases as flagged by the Directorate of Income-tax (Systems) as per risk profiling;

4. Cases based on the information derived from field survey action, requiring action u/s 148 of the Act.

5. Cases based on the information provided by any Income-tax authority requiring action u/s 148 of the Act with the approval of concerned Chief Commissioner of Income Tax.

It is to be noted that, any other case, except for those mentioned above, shall not be considered for taking action u/s 148 of the Act by the JAO.

It is further clarified that any action u/s 148 shall be taken by the Assessing Officer, after forming a reasonable basis that the respective case involves tax evasion or income chargeable to tax has been escaped and such reasons to believe shall be recorded and the required sanctions be obtained from the requisite authorities.

However, these instructions shall not apply to the Central charges and International Taxation charges for which separate instructions have been prescribed.

The Income Tax Department has been provided with the power to reassess an individual’s previously filed income tax returns, under Section 147 of the Income Tax Act, 1961.

But for such reassessment, the Assessing Officer is required to perform the pre-defined criteria by sending a notice under section 148 for income Escaping Assessment.

In the Union Budget 2021, CBDT proposed to reduce the time limit to re-open income tax assessment cases from 6 years to 3 years.

However, a period of 10 years be provided, for reopening of assessment, where there are reasons to believe that the case involves, concealment of income of more than Rs 50 lakh.

An individual, who is filing their ITR in India, shall receive a notice under section 148, where the assessing officer has reasons to believe that the income disclosed by such an individual might have been escaped, to involve in tax evasion.

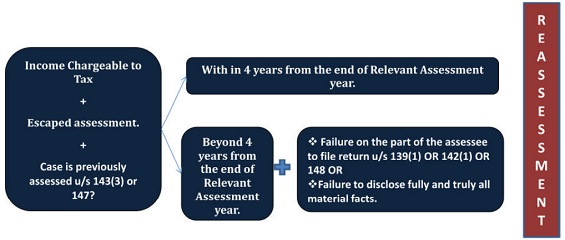

For the cases, where 4 years succeeding the relevant assessment years has elapsed, the assessment under Section 143(3)/ 148 can be made, provided the following three conditions are met –

Generally, where the assessing officer comes some material information disclosed fully and truly by the assessee, in their ITR, the AO may have prima facie reason to believe that income chargeable to tax has escaped assessment, on the basis of that material information.

However, the respective assessee can always raise the issue providing information that the AO was in receipt of such material facts at the time of original assessment.

The AO has the authority to receive information from any other sources including information/ material from the DIT (Investigation), which was not available at the time of original assessment.

Where the AO has to establish live link, with the information/ material provided in the return of income and/ or details filed by the assessee during original assessment, he needs to have reasonable belief that the assessee failed to disclose fully and truly all material facts necessary for his assessment.

Thus, the AO has to examine not only material facts, whether disclosed or not, but whether the same were disclosed fully and truly, since the disclosure of all material facts fully, in no matter means that it was disclosed truly also.

Thus, from the above information on reasons to believe, we can make out that for a valid reopening of assessment, it is one of the core ingredients required. There is a requirement of a new tangible material, and shall not be merely a change of opinion. There is a procedure to be followed to systematically perform and produce the reasons to believe. The procedural requirement includes the “Recording of Reasons”, “Requesting for reasons and disposal of its objection”.

Where the proof supporting the belief of the AO is available, the same be recorded in writing and be sent to the individual under section 148. Some facts or new documents are required evidencing the escaping of income during the original assessment. Where such new information or documents is available with the AO, he has the full authority to take action against such assessee under section 147 & 148.

As per Section 151(1) of the Income Tax Act, 1961, no notice be issued under section 148, by an Assessing Officer, after the expiry of four years from the end of relevant AY, provided the Principal Chief Commissioner or Principal Commissioner is satisfied, that the reason to believe recorded by the AO, is fit and valid under the law.

In case, the above requirement by the AO is not fulfilled, then the AO has no right to issue notice under section 148, if he is below the rank of a Joint Commissioner, provided the Joint Commissioner is satisfied, on reasons recorded by such AO.

For successful and valid reasons, the AO shall apply his mind and make his own findings rather than, relying on others, or using frivolous information received from any department. Apart from this, a valid reason shall be drafted appropriately indicating the valid Reason to Believe.

It is clear from the above discussion, that where the provisions related to issuance of notice are not fulfilled, the notice shall be invalid. Thus, any reassessment under an invalid notice, shall be declared invalid. Section 153 specifies the time limit within which such reassessment be completed. As per the section, any reassessment relating to Section 148 of the Income Tax Act, shall be issued within a period of 4 years from the end of relevant AY, and the same shall involve escaping of income up to INR 1 lakh.

Where the case involves escaping of income exceeding Rs 1 lakh, the notice under the said section shall be issued within a period of 6 years from the end of relevant AY, subject to the fulfilment of provisions contained in section 151.

Similarly, the notice under section 148 could be served within a period of 16 years from the end of relevant AY, where the escaping of income relates to assets located outside India. Also, where the assessment has been completed under section 143(3) or 147, no further notice for reassessment be issued, after expiry of 4 years from end of relevant AY, provided the income chargeable to tax has escaped assessment for such AY due to failure on assessee’s part to file the return under section 139 or 142 or 148 and in case where the assessee fails to disclose the material facts, fully and truly, in the original assessment.

It is to be noted that every assessment, opened under any of the above sections, is required to be completed and closed, within 1 year from the end of the financial year in which notice is served. However, the said period is extended to 2 year, where any reference is made to TPO u/s 92CA.

Every assessee is advised not to take any notice lightly. Where any notice is received under section 148, the following points be taken care of –

Q.: Can any further claims be filed by the assessee during the reassessment?

Earlier, it was in practice that the income for purposes of reassessment cannot be proceeded with income beyond that originally assessed. Thus, new claims or deduction were not allowed in reassessment proceedings.

However, in the case of Vishwanath Products (2008) 117 TTJ 549, it is held that a fresh deduction can be claimed, provided, it does not reduce the income below the originally assessed income.

Q.: Can audit objections be a valid reason for reopening of assessment by the AO?

As discussed above, any opinion made by the AO, based on the opinion of the audit party, is not a valid source of information and the same was held by the Supreme Court in the matter related to Indian & Eastern Newspaper Society v. CIT, (1979) 119 ITR 996.

However, it was further clarified that the audit note could be valid information, provided the same is not regarded as reason to believe by the AO without application of his mind. This provision was clarified in the case of P. V.S beedies P Ltd- 237 ITR 13(SC).

Q.: Can any retrospective amendment be a valid reason to reopen the assessment?

Where the reassessment is made within 4 years after the end of relevant assessment year, retrospective amendment is a valid reason for reopening the assessment, but where the reassessment is made after the expiry of 4 years, the same is not allowed.

Q.: What are some of the tax management issues to be considered during the reassessment proceedings?

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}