CONVERSION OF LLP INTO COMPANY LIMITED BY SHARES.

- LLP Act, 2008 does not cover the conversion of LLP into Company but in Companies Act, 2013 conversion of LLP into Company is covered in section 366.

- Please note that recently MCA has notified Companies (Authorized to Register) Amendment Rules, 2018 which shall came into force on 16.02.2018 in which form URC–1 has been revised, which can be used for filling application by Company for registration under section 366.

COMPANIES CAPABLE OF BEING REGISTERED

The word “Company” for the purpose of this section shall include Partnership Firm (PF), Limited Liability Partnership (LLP), Co-operative Society but exclude Unlimited Company having more than and equals to 7 members, Company limited by shares, Company limited by guarantee.

According to Section 366 of Companies Act, 2013 read with rule 3 & 4 of the Companies (Authorized to Register) Rules, 2014:

SOME PRE-CONDITIONS FOR CONVERSION OF LLP INTO COMPANY LIMITED BY SHARES ARE AS FOLLOWS:.

- Any Company registered under Indian Companies Act, 1882, Indian Companies Act, 1913 & Companies Act, 1956 shall not be allowed for taking registration under this Part.

- The Company shall have at least 7 Members (i.e. a LLP shall consist of at least 7 partners at the time of conversion, if there are less than 7 then increase the number of partners first)

- A Company having its liability limited by an act of Parliament shall not register as Unlimited Company or Company Limited by Guarantee under this part (i.e. a LLP can only convert into Company limited by shares).

- Company shall before taking registration, take assent of all the members present & proxies (if allowed) in a general meeting summoned for this purpose.

PROCEDURE OF THE CONVERSION OF LLP INTO COMPANY LIMITED BY SHARES IS AS FOLLOWS:

Check whether number of members present is more than or equal to 7 or not (if not then increase the number of members first). Duly Conduct a meeting for this purpose and pass a resolution in this regard.

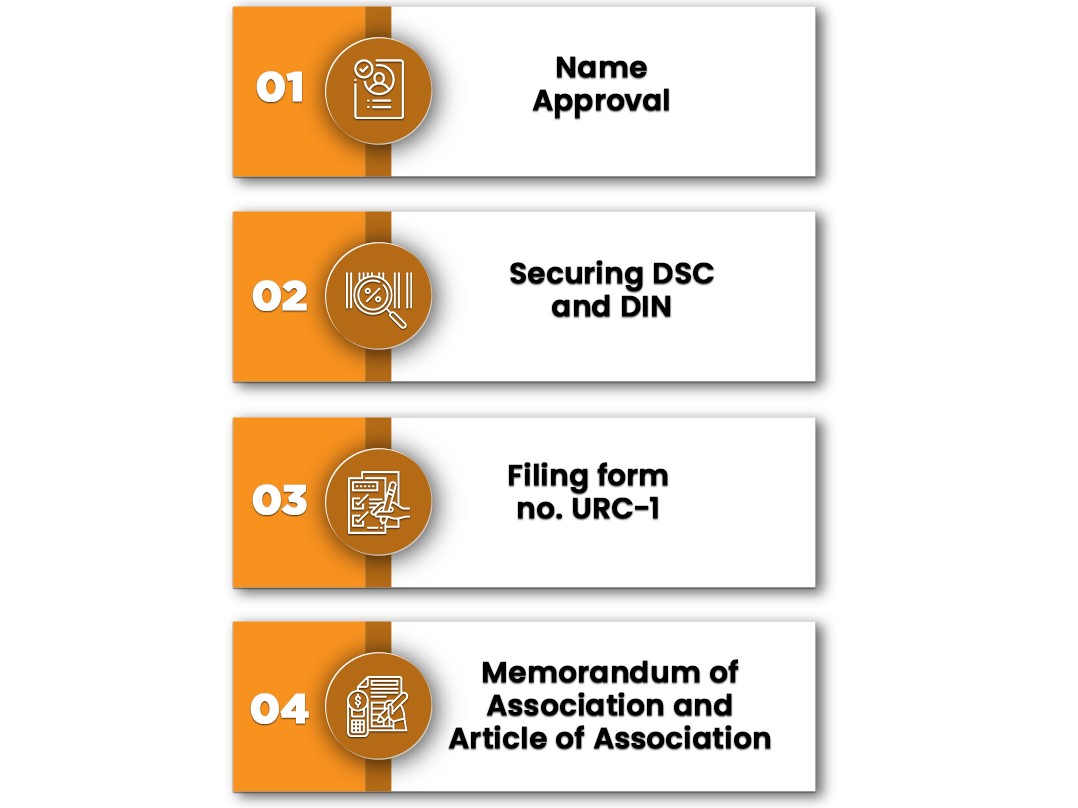

Obtain availability of name under section 4 of Companies Act, 2013 (record a ‘decision taken’ for this purpose).

Publish an advertisement in form URC-2 about such registration (seeking objections, if any within 21 days from publication), in English & Vernacular language newspaper circulating in the district in which LLP situate.

Know more about the relevant blogs:

Procedures for the conversion of partnership firm into Private limited company

Conversion of LLP into Company Limited by Shares

File form URC-1 and attach following documents in the form as per Rule 3 & 4:

- List showing names, address & occupation of all persons named as members with details of shares held, showing separately shares allotted for consideration in cash & for Consideration other than cash, also source of consideration. In case shares are numbered, each share by its number who on a day of seeking registration were partners in LLP.

- Affidavit from each proposed first directors that the proposed directors are not disqualified under section 164 to hold the position of the Director.

- List of names, address of partners of LLP.

- Copy of Limited Liability Partnership Deed (if revised then copy of past deed).

- Statement specifying Nominal share capital, No. of shares taken & amount paid, name of company with word limited/Pvt. Ltd.

- Consent/NOC from all secured creditors.

- Consent from majority of members whether present in person or in proxy (if allowed) in general meeting held for this purpose.

- Undertaking that proposed directors shall comply with requirements of Stamp Act.

- Statement of asset/liabilities certified by Chartered Accountant in Practice made for not earlier than 30 days from filling URC-1.

- Copy of latest Income Tax Return of LLP.

- Copy of notice published in Newspaper and proof of service to ROC.

- Declaration and statement of proceedings (if pending before any court/tribunal/ authority) shall be submitted with URC-1 that they have complied/filed all documents which are required to be filed under LLP Act & no any default persist till now.

Well enough! You have completed your part of duty now the part of duty of registrar begins……….Registrar shall within 30 days from filing the form, decide whether registration will be granted or not. If ROC satisfied with the documents presented then may issue Certificate of Incorporation (COI) in form INC-11.

With the issue of COI conversion is complete officially in all respect.

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}

{kind=link}