Issue Of Share Capital On Under Right Issue Section 62

Page Contents

Further Issue Of Share Capital On Under Right Issue Basis Section 62 of the companies act 2013

- Shareholders who, at any time, plan to increase their subscribed share capital increase their share capital by selling shares to their current shareholders who, at the date of the bid, are the holders of the share capital of the company.

- In basic words, the right issue is an offer to the existing shareholders to buy the equity of the company in proportion to the current stock. It is the best way to encourage capital in a business. It is up to the owners whether or not they support it.

- Unless the terms of the Article of the Company do not provide otherwise, the current owner still has the right to revoke this privilege for the benefit of some other individual.

- The firm sends the Letter of Offer to the owners of the company stating the number of shares offered and the time period during which the bid is to be approved.

- Time period recommended will not be less than 15 days, but not more than 30 days. In the case that no notice has been obtained from the shareholder side within the specified time period, the bid is considered to have been rejected.

- The existing shareholder of the company to purchase additional shares at discounted prices in proportion to their existing holdings. A shareholder entitled to receive the share on the basis of the offer rate prescribed in the letter of offer.

- For eg, the bid ratio is 1:2 which means that the shareholder owning two shares is able to receive one share if he only has 3 shares and is entitled to receive 1 share. If he has 4 shares, he is entitled to 2 shares.

- Through this offer, corporations give shareholders the right, but not the duty, to buy new securities at a discount on the existing stock price.

- In the case of non-acceptance of such a bid, the Board of Directors shall have the right to dispose of it in a manner that is not adverse to the owners and the company.

- If, at any point, a company with a share capital intends to raise its registered capital through the issuing of additional shares; those shares shall be offered—

ON RIGHT BASIS: to existing shareholders in proportion to the company’s paid-up equity capital owned by them by means of a letter of offer.

PROCEDURE FOR ALLOTMENT OF SHARES On RIGHT ISSUE BASIS:

- Note in writing to each Director at least seven days prior to the meeting of the Board of Directors. [Sec 173(3)] Pass the vote of the Board to accept the “Statement of Bid” The letter of bid also contains the right of renunciation.

- Dispatch of the Letter of Offer to all current shareholders by registered post or speed post or by online means at least three days before the opening of the issue.

- Convene a decision of the Board of Directors of the Pass Board to approve allocation and issue of shares.

- Receive approval, renunciation, denial of rights of shareholders

- Meeting of the Directors and Notification of Meeting of the Board of Directors given at least seven days prior to the meeting of the Board of Directors (Section 179(3)).

- The meeting of the Board of Directors will be held in compliance with SS-1 to accept the Board of Directors’ Decision on the adoption of the “Letter of Bid.”

- Letter of offer will be submitted to existing shareholders by registered post or by fast post or by online means, with proof of delivery to all current shareholders at least three days before the opening of the issue.

- For the case of the “Public Business” file MGT-1 within 30 days from the date of the vote of the Council.

- Register the return of allotment with Registrar in E-Form PAS-3 within 30 days of allotment of shares.

- The Register the return of allotment with Registrar in E-Form PAS-3 within 30 days of allotment of shares.

- File E-form MGT 14 within 30 days of issuance of securities.

- Addition to the E-Form PAS-3 I Board resolution on distribution and question of interest. (ii) Letter of Offer (iii) List of Allottes

- List of Allottes attached to E-Form PAS-3 shall state the names, address, profession, if any, of the owner and the number of shares assigned to each of the allottes, and the list shall be certified as complete and accurate by the signatory of Form PAS-3 in accordance with the company’s records.

- Issue of the share certificate over a span of two months from the date of issuance in the form-SH-1. Stamp duty paid within 30 days of the date of issue. Reasonable

- In the case of a listed firm – Unless otherwise mentioned, SEBI (ICDR) Regulation 2009 shall apply where the aggregate value of the stated offer is fifty lakh roupies or more. Provided that provision of this Regulation does not apply to securities issued pursuant to Regulation 9(1) of the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

The complete concept of Right Issue of shares company under the companies act, 2013

- FEMA provisions allow Indian companies to issue, if any, the right shares to existing non-resident shareholders, subject to the sectoral cap.

- Furthermore, this concern will also be concerned with in accordance with the other statute. (a) In the case of shares of a company listed on a recognized stock exchange in India, at a price as decided by the company; (b) In the case of shares of a company not listed on a recognized stock exchange in India, at a price not less than the price at which the right-based bid is made to a resident shareholder.

- It is appropriate to receive prior permission from RBI for Right Issue to former OCBs. An investor may allocate an additional right share out of the unsubscribed portion, subject to the condition that the total issue of the shares to non-residents in the company’s total paid-up capital does not exceed the sectoral cap.

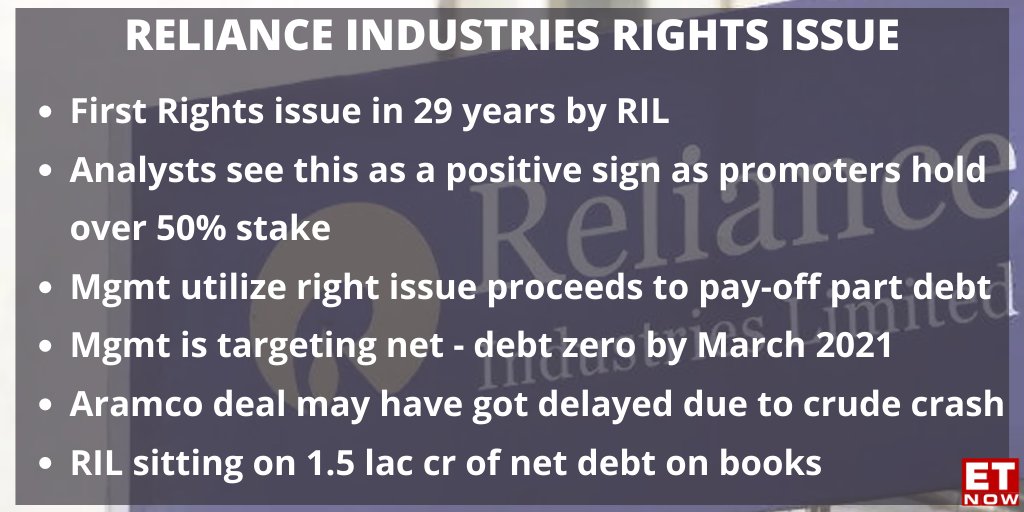

- RECENT RIGHT ISSUE Reliance Industries (RIL) which is India’s most popular corporation proposes to collect Rs 53,125 crore by giving Rs.1,257 a share discount of 14 percent. Existing RIL shareholders may buy One share for every 15 shares owned The target to raise this issue is to decrease the net debt to zero by 31 March 2021.

Complete Overview on Share Capital or Debenture

Also, read recommend blogs;

- The complete concept of right issue of share under the companies act, 2013

- Summary of SEBI relax encouraged provisional relief for the rights issue

Post by Rajput Jain & Associates