Page Contents

The best investment schemes for savings taxes are three common choices for people seeking stable, reliable, and fixed returns on their investments to save tax.

Three such investment alternatives that are taxable of the Income Tax Act and that offer a permanent return are fixed bank deposits, post office time deposits, and national saving certificates (NSC).

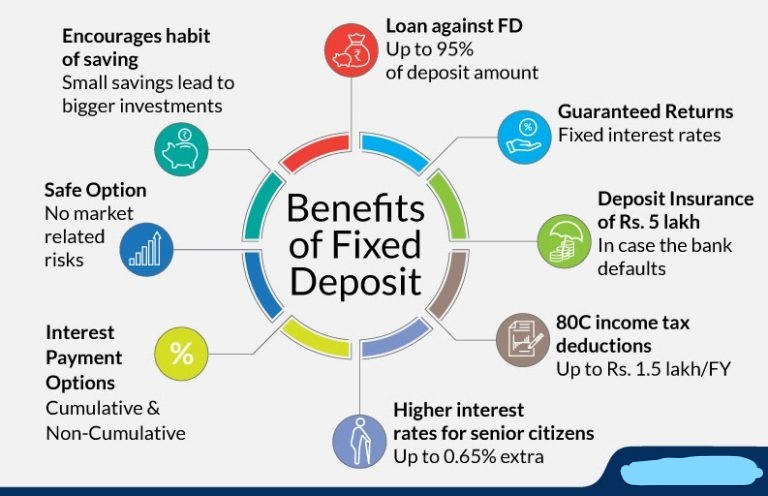

For many investors, especially senior citizens, bank deposits continue to be the option of choice when it comes to investing money in a safe place.

Some top tax-saving instruments on basic main factors are stability, liquidity, costs, transparency, ease of investment, return, and taxability of profits. Each factor was given equal weightage and the composite scores decided their position in the ranking.

The five-year banks’ tax-saving FD scheme will serve you if you are a taxpayer who wants to benefit from your investment in the FD bank. Investing in the bank FD tax saver is subject to Section 80C and will therefore allow you to save your tax.

In the year of receipt, the interest received is completely taxable by the lender. The return on a 7% FD is about 4.82% for an individual paying 31.2% tax (the highest tax rate).

Although the banking FD implicit guarantee is issued, the explicit guarantee is only up to Rs 1 lakh pursuant to the DICGC Act. The insurance is covered by the principal and interest received in each branch of a bank and is available for a deposit.

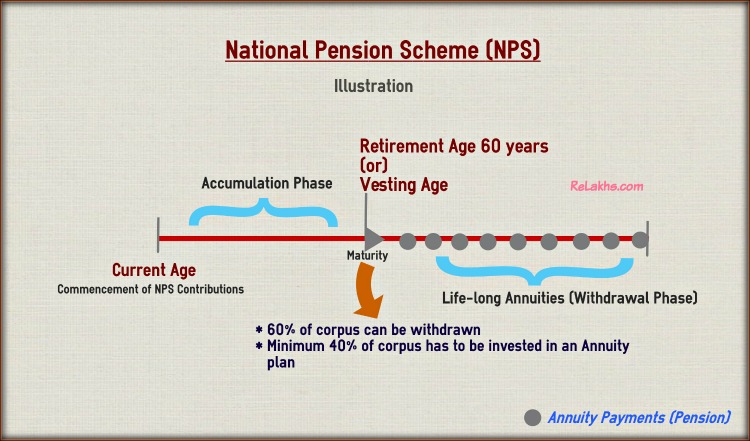

The tax is now free for 60 percent of the corpus that can be removed when retired.

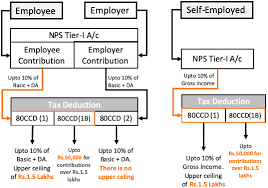

The NPS has only become more appealing by the changing investment and tax laws. Firstly, at the time of retirement, 60% of the entire corpus can be withdrawn tax-free.

Secondly, the active option of NPS is now open for investors to assign up to 70% to shares. You will stay invested until you are 70 and the withdrawals can be increased. In three separate parts, NPS will help save revenue. The deduction under Sec 80C is valid for donations up to €1.5 lakh.

The Sec 80CCD requires additional deductions up to Rs 50000 (1b). If you have up to 10% of your basic NPS pay, your employer will not be subject to taxes on that amount. The tax is now free for 60 percent of the corpus that can be removed when retired.

For those over 60, the Senior Citizens’ Savings Scheme was the best tax-saving and the Budget of last year allowed it more appealing by offering an additional $50,000 interest income exemption to seniors.

The total fiscal exemption for those over 60 is now Rs 3.5 lakh and over 80 Rs 5.5 lakh. The 8.7% of all SCSS small savings schemes provided by the SCSS is the maximum. The term SCSS is 5 years, which can be extended to another 3 years. But the cumulative investment cap of Rs 15 lakh remains.

Furthermore, the scheme is mainly open for investors over 60. When the investor decides to retire willingly and does not take another job the minimum age is 58. An additional Rs 50,000 tax exemption for interest income is granted to senior citizens.

The Sukanya Samriddhi Yojana is a smart way to save for taxpayers with a daughter under 10 years of age. The interest rate will be 8.5 percent until March and may adjust in April.

A higher rate than the PPF is provided by the Sukanya scheme. Much like the PPF, the interest received is tax-free and the investment has an annual limit of around 1.5 lakh. In any post office or designated bank with a minimum investment of about 1,000, accounts can be opened.

For a maximum of two children, a parent can open an account, but the combined investment in the two accounts cannot exceed ~ 1.5 lakh in a year. The best thing is that the account is opened on behalf of the infant and the gains from maturity have to be used for her education and marriage.

Basically, Traditional policies are not likely to offer the insurance cover that an individual really wants. Experts claim that one should have at least 6-8 times his annual revenue covered.

So, at the age of 30, anyone earning 50,000-60,000 a month should have a life insurance policy of approximately 40-50 lakh. The buyer would cost nearly 4-5 lakh per year for an endowment scheme providing a cover of 40-50 lakh. This is almost 60-70 percent of his overall earnings.

A term cover for Rs 1 crore, however, would cost him only Rs 7,000-8,000 a year, which will be just 1% of his income. When you go shopping for a tax-saving method this year, keep this equation in mind.

Ulips had a distinct tax advantage over mutual funds even before the tax on capital gains was revealed. Ulips offers investors not only equity funds but also debt and liquid fund options. It does not have any tax repercussions to turn from equity to debt or vice versa.

Short-term debt fund income and fixed deposit revenue are charged at a marginal rate. After indexation, long-term capital gains from debt funds are taxed at 20 percent. But still, Ulips’s revenue is tax-exempt. The new Ulips introduced by insurance firms are cost-effective and compete with direct.

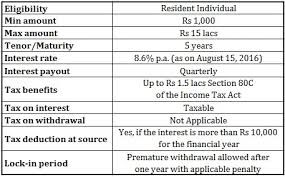

In a post office, the post office time deposit (TD) is almost like a bank fixed deposit, except one can only deposit for 1 year, 2 years, 3 years, and 5 years. The deposit made for a five-year term is liable for the tax gain of Section 80C.

The interest rate is currently 7.7 percent per annum, payable monthly but compounded quarterly (January 1 to March 31, 2020). The interest gained is completely taxable and, as in the case of bank FD, should be added to one’s ‘income from other sources.

NSC’s term is also 5 years, but there is no way to get daily interest payouts, not even annual payments, unlike bank FD and PO Time Deposit. It is possible to have the amount invested in NSC only upon maturity.

The interest in NSC is taxable, but the interesting thing about NSC is that the interest accruing annually is considered to be re-invested within the first 4 years and thus qualifies under section 80C for tax benefit.

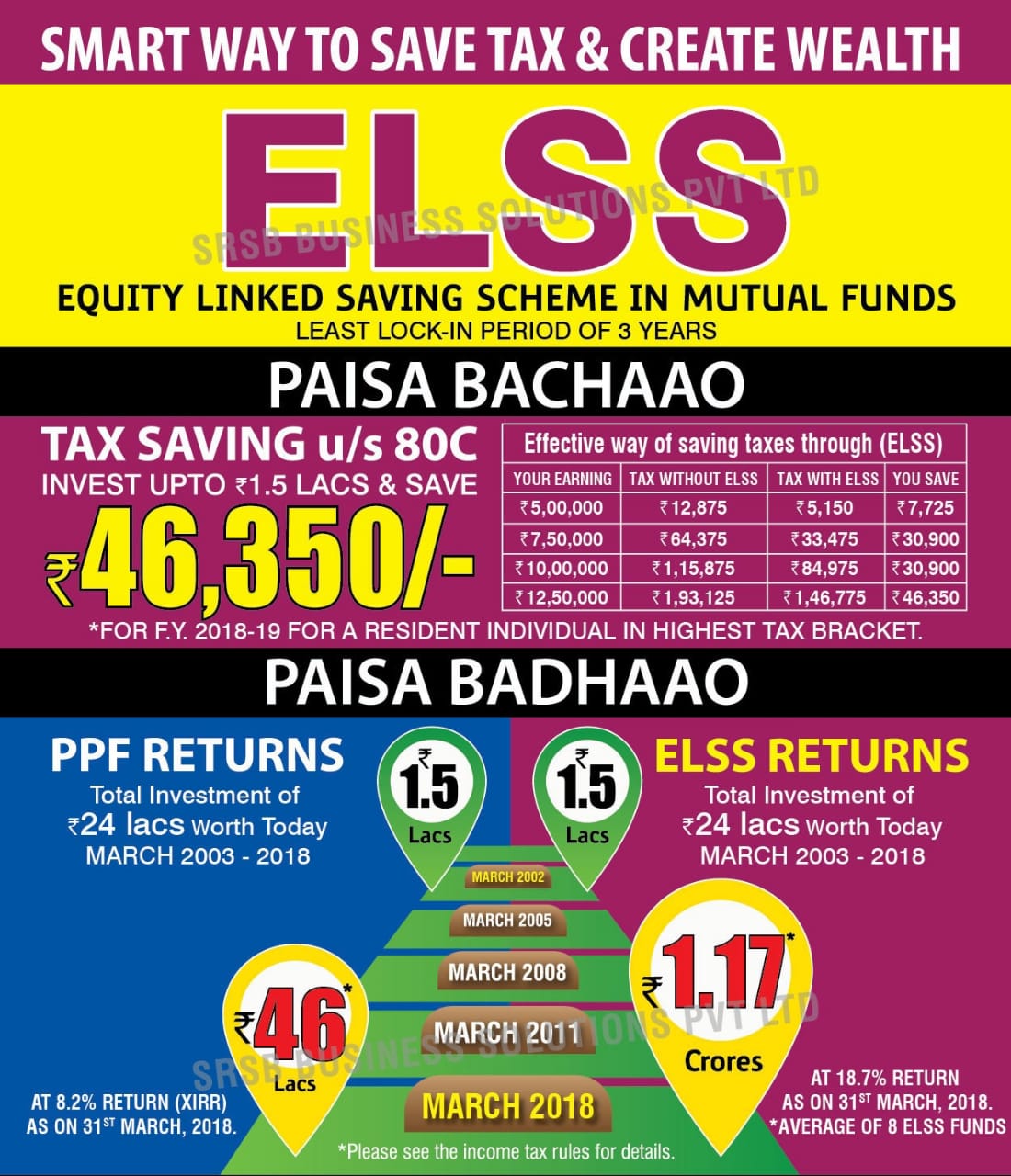

The best way to save taxes is by ELSS tools. While the SIP window has closed for taxpayers who would have had to show evidence of Sec 80C tax-saving investments by now, experts say that before the 31 March deadline, one can still put money into ELSS funds in 2-3 tranches.

It should be pointed out that not all ELSS funds bear the same risks. Some allocate more to small and mid-cap stocks, while others stick to big-cap stocks that are stable.

Select the one that best suits your appetite for danger. ELSS funds have a three-year lock-in, the shortest of all tax-saving options. For young taxpayers, ELSS is the perfect way to save income. With monthly SIPs, they can stagger their investments.

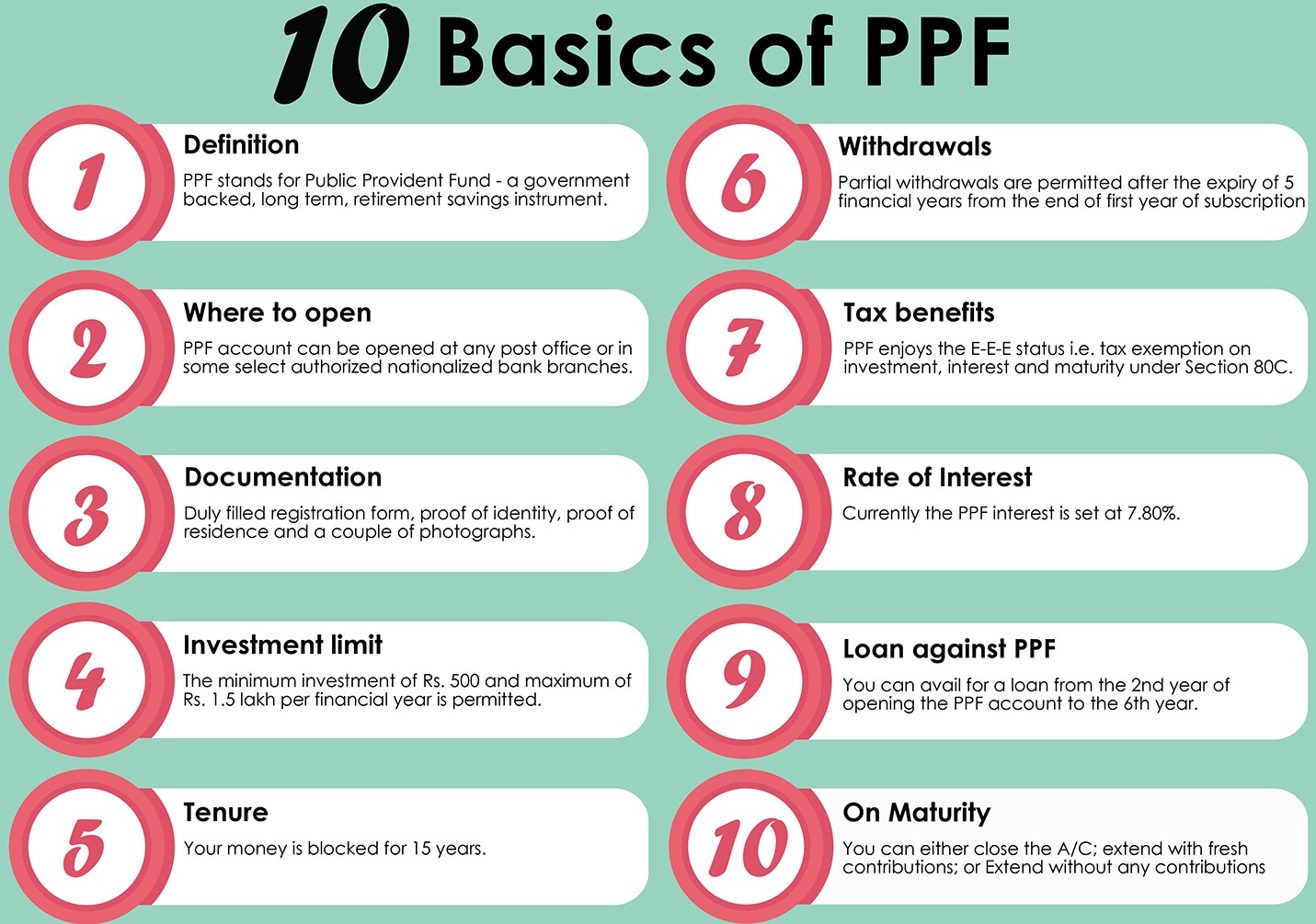

After a sustained increase in bond yields, PPF prices were hiked in October 2018. In the third quarter of 2018-19, although bond yields subsequently decreased, PPF rates remained unchanged.

Advisors claim PPF is a safe bet since the interest is tax-free, offering a distinct advantage over fixed deposits to the small savings scheme. FDs’ interest is entirely taxable, taking returns in the largest tax bracket down to just 5 percent. Advisers also caution against bingeing on the instruments of fixed income.

On protection, flexibility, and ease of investment, PPF scores high. In a post office or specified bank branches, an account may be opened. Opt for a bank that enables the account to be accessed online.

Tip: No tax benefit on principal repayment, only on interest.

Tip: This is in addition to the ₹1.5 lakh deduction under Section 80C.

Tip: Different from Section 80U (which is for taxpayers with disability themselves).

Note: Businesses claim this under Section 80GGB.

Tip: Useful for academics, inventors, researchers, and creative professionals.

Quick Recap Table:

| Section | Purpose | Deduction Limit |

| 80E | Education loan interest | No limit (interest only) |

| 80TTA / 80TTB | Savings/Deposit interest | ₹10,000 / ₹50,000 |

| 80DD | Maintenance of disabled dependent | ₹75,000 / ₹1,25,000 |

| 80GGC | Donation to political parties | 100% (non-cash) |

| 80RRB | Royalty/patent income | Up to ₹3,00,000 |

Term of Capital gains exemption is referred to as benefit provided by the government to taxpayers, easing the burden of paying tax on capital gains, The requirement to pay capital gains tax arises when a taxpayer sells an asset (other than personal property and stock used in the business) for a profit.

Popular blog:-

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}