Page Contents

The Union Cabinet, chaired by the Prime Minister Shri Narendra Modi, has approved the proposal to introduce the Negotiable Instruments (Amendment) Bill, 2015 in Parliament.

The amendments are focused on clarifying jurisdiction related issues for filing cases of the offence committed under Section 138 the Negotiable Instruments Act,1881 (NI Act).

Section 138 of the NI Act deals with the offence pertaining to the dishonour of cheque for insufficiency, etc., of funds in the drawer’s account on which the cheque is drawn for the discharge of any legally enforceable debt or other liability.

Section 138 provides for penalties in case of dishonour of cheques due to insufficiency of funds in the account of the drawer of the cheque.

The main amendment included in this is the stipulation that the offence of rejection/return of cheque u/s 138 of NI Act will be enquired into and tried only by a Court within whose local jurisdiction the bank branch of the payee, where the payee presents the cheque for payment is situated.

The object of the NI Act is to encourage the usage of the cheque and enhance the credibility of the instrument so that normal business transactions and settlement of liabilities could be ensured.

The clarification of jurisdictional issues may be desirable from the equity point of view as this would be in the interests of the complainant and would also ensure a fair trial.

Clarity on the jurisdictional issues for trying cases of cheque bouncing would increase the credibility of the cheque as a financial instrument.

This would help trade and commerce in general and allow lending institutions, including banks, to continue to extend financing to the economy, without the apprehension of the loan default on account of bouncing of a cheque.

Action will be initiated to introduce the Negotiable instruments (Amendment) Bill, 2015 in Parliament in the second phase of the current Session of Parliament.

II Government Decides to Fix Interest Rates at 8.7% for General Provident Fund(GPF) and other Similar Funds Including Special Deposit Scheme, 1975(SDS,1975) for Non-Government Provident, Superannuation and Gratuity Funds for the Financial Year 2015-16

It was decided by the Government to link the interest rates of State PFs (General Provident Fund and other similar funds) including Special Deposit Scheme, 1975 (SDS, 1975) for Non-Government Provident, Superannuation and Gratuity Funds for the FY 2015-16 to Public Provident Fund (PPF) rates.

In pursuance of that decision, the Government has decided to fix the rates 8.7% per annum applicable to the following:-

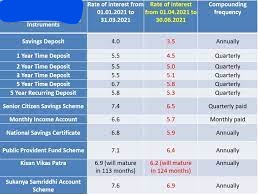

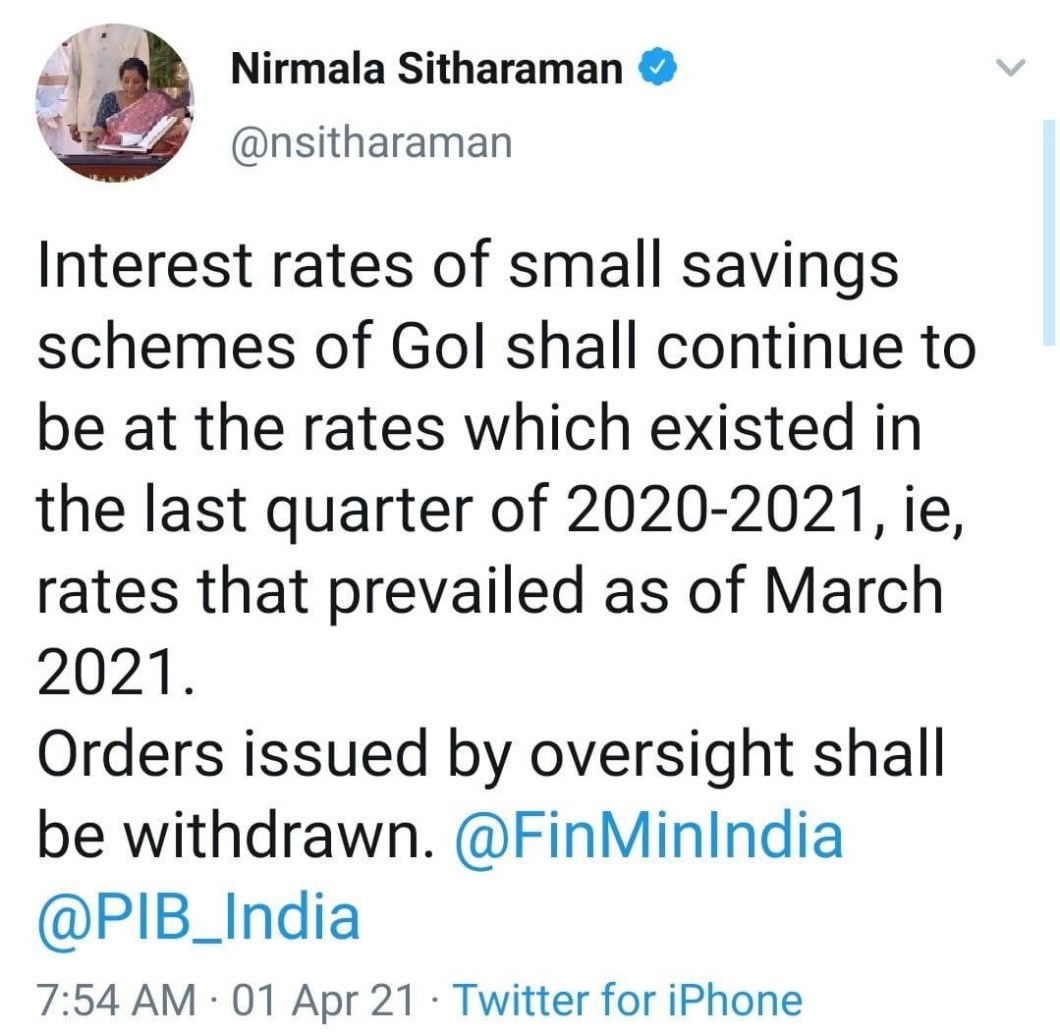

Recently, the Government had kept the interest rates for PPF and other Small Savings Schemes intact.

However, interest rates for 5 year Senior citizen Saving Scheme and Sukanya Samriddhi Account Scheme have been increased from 9.2 to 9.3% and 9.1 to 9.2% respectively. keeping in view the commitment of the Government towards the welfare of the girl child and the senior citizens.’

Contributions to the Employee Provident Fund (EPF) above INR 2,50,000/- per year will be kept separate basket and taxed in the same way as fixed deposits, without any double taxation.

Whatever contribution you make to the Provident Fund, what’s in exceeding INR 2,50,000/-, it will be in a different basket and the interest on that specific corpus will be taxable.

For query or help, contact: singh@carajput.com or call at 9555555480

Popular blog:-

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}