Overview of the GST New Rule 86B

Page Contents

www.carajput.com; GST RETURN- GST Rule 86B

Under GST new Rule 86B-: Restriction on Input Tax credit Utilisation in Electronic Credit Ledger

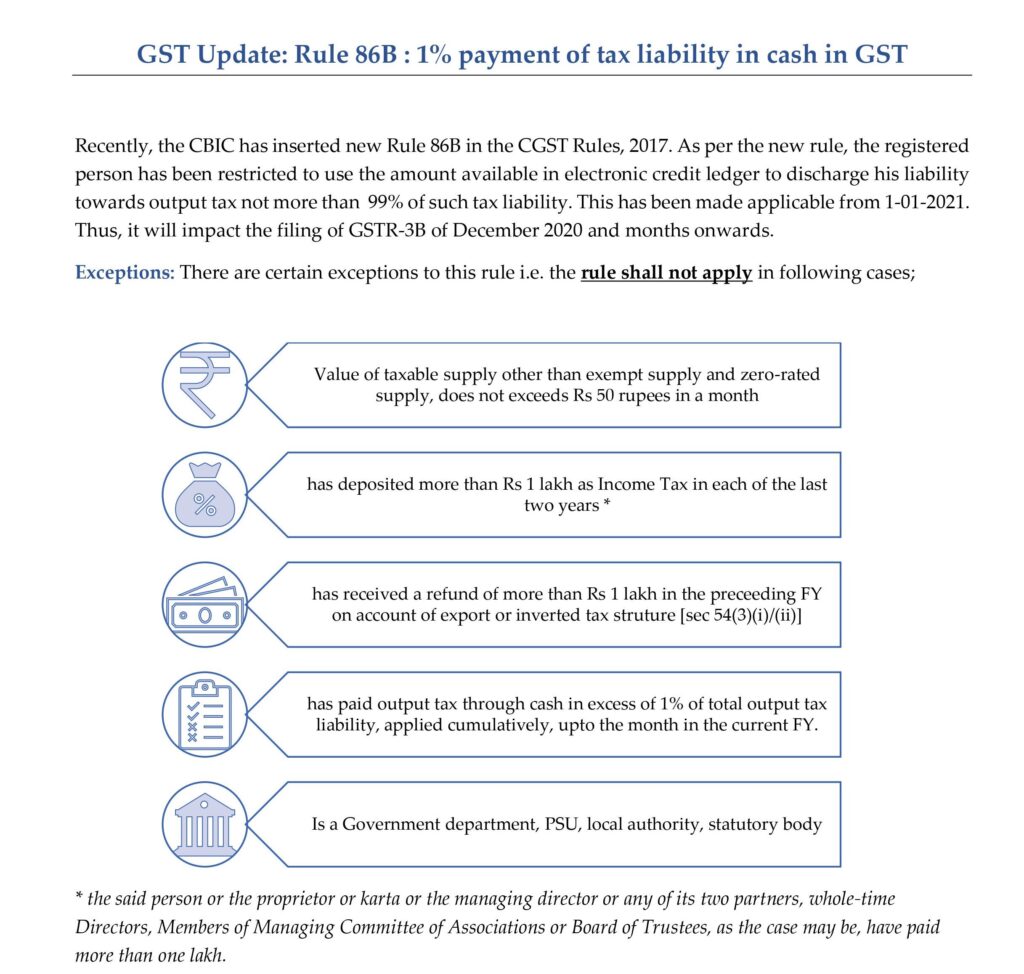

A new rule in CGST rules 2017 has been declared by the Central Government; rule 86B provides restrictions on the use of Input Tax Credit to release output liabilities. This regulation extends from 1 January 2021 onwards and has an overriding effect on other laws. It ensures that the registered individual cannot use the amount available in the credit ledger to pay the output tax liability in excess of 90% of that tax liability. If the amount of the taxable supply exceeds the exempted supply and the zero-rated supply, it exceeds 50 lakh rupees per month.

Prior to rule 86B, ITC utilization permitted

By avoiding the cascading impact of taxes, the ITC plays an important role in the GST. There have been several improvements in the order of use of ITC for various components such as CGST, SGST and IGST. However, to release the output tax liability, the ITC available in the electronic credit ledger can be fully utilized. The use of the ITC balance for payment of its production tax liability has been limited by new rule 86B.

Restrictions imposed according to rule 86B

Rule 86B restricts the use of the open ITC in the electronic credit ledger for the release of the liability for output tax. This rule has a negligible effect on all the other CGST laws.

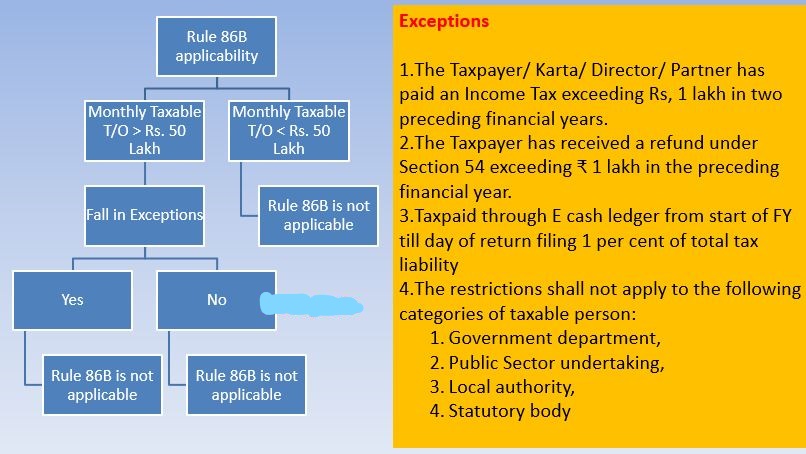

Applicability

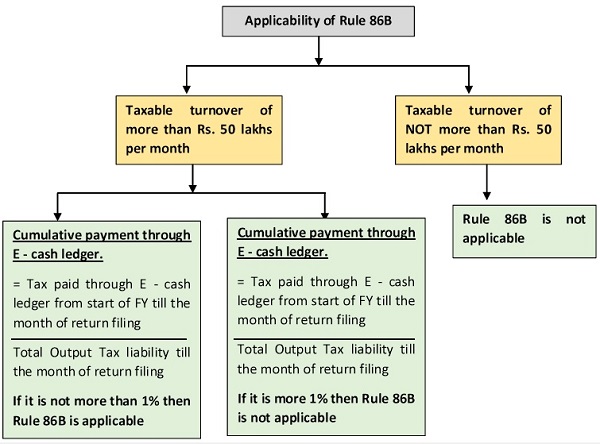

This rule extends to registered persons with a taxable supply value greater than Rs.50 lakh per month. Before filing each return, the limit has to be reviewed every month.

Imposed Restriction

On ITC, applicable registered individuals will not be responsible for more than 99% of the production tax liability. In other words, by using the input tax credit, more than % of the production tax liability cannot be released.

Exceptions to the law

- In cases where the individuals mentioned below have deposited more than Rs. 1 lakh rupees as an income tax under the Income-tax Act 1961, payment of income tax of more than one lakh rupees will not be applicable.

- The individual who is registered

- The Owner, Karta or managing partner of a registered individual or of a registered person

- Either of the two spouses, full-time directors, members of the associations’ executive committee, or the registered persons’ board of trustees, as the case may be.

- If, in the preceding financial year, registered persons received a refund sum of more than one lakh rupee than the unused ITC input tax credit refund for zero-rated supplies of products or services or Rule 86B, it would not be applicable.

- Applicability: This rule extends to registered persons with a taxable supply value greater than Rs.50 lakh per month. Before filing each return, the limit has to be reviewed every month.

- Imposed Restriction: If a registered person is concerned, then a cumulative amount of the total production tax liability by electronic cash register has been discharged up to that month within that financial year. Therefore, the taxpayer must keep track of whether his cumulative discharge of the tax liability for output tax through the electronic cash ledger is more than 1% up to the month of filing of the return when filing the return for each month.

- If one of the following is the registered individual under examination:

- Department of Government

- Undertaking in the public sector

- Local authority

- Statutory Authority

Impact of new 86B regulation

- After analyzing the restrictions and exemptions set out in Rule 86B above, it is clear that the rule referred to above applies only to large taxpayers.

- There will be no effect on micro and small enterprises, and it is specifically mentioned under this provision that this rule is intended to regulate the problem of fake invoices in order to use the input tax credit to discharge the liability.

- Without possessing any financial reputation, it restricts fraudsters from displaying high turnovers.

- The enforcement burden on taxpayers would be further increased by the limitations imposed by rule 86B.

- Having complied with the above restrictions and derogations introduced by Rule 86B, it is clear that the above-mentioned rule applies only to large taxpayers. There will be no impact on micro and small enterprises. The motto behind the implementation of this rule is to control the issue of counterfeit invoices for the use of counterfeit input tax credits to discharge the liability. Furthermore, it constrains fraudsters from having high turnover without financial credibility.

- In addition, CBIC has explained that 1% is to be calculated on the tax liability for the month and the turnover for the month in question.

- Although this rule has also started to bring real taxpayers under the purview of making it difficult for them, the government’s motto is to avoid false invoicing and ultimately reduce tax evasion.

CBIC has, however, explained that 1% of tax liability is often unveiled for which refund is not permitted. The new law includes numerous exceptions such as exporters, inverted tariff structure suppliers, and taxpayers whose footprint is in the database on income tax.

This New GST rule on ITC might be created disputes for Honest Taxpayers.

A new amendment & several changes have been introduced under the GST plan via the 14th GST amendment rules 2020. The blog focuses on the essential rule added with regard to the ITC that will be implemented on 1/01/2021.

This latest rule has been implemented in 86B which shows that at least 1 percent of their output GST liability in cash is the division of the assessee to mandate discharge. Fake people are seeking to discharge the Complete GST liability through an Income Tax credit so avoiding cash payments. The fraudster can be tracked via this limit. Which has been Founded by lawmakers just because of the increase in daily fake invoicing spam. In this way, it would ensure the verification of unfaithful acts and the disclosure of revenue inside the Govt’s safe.

As a consequence of this required obligation to release Goods & Services Tax liabilities of no less than 1 Percent it is more difficult through cash during the Covid -19 lockdown period, below are the mentioned compliances for these procurements, which provide a different viewpoint. The amount of the taxable supply (Excluding exempt & Zero-rated) is less than INR 50,00,000/- Per month. As a result, smaller assessees will not include in this assent. The assessee or principal officers of him, such as MD, Full-time Director, etc., possess INR 1,00,000/- as income tax benefit under the Income Tax Act, 1961, in each of the last two Financial Years.

The fund that is not used shall be reimbursed by the assessee for those funds that are more than INR 1,00,000/- in the Past FY in respect of Zero Rated Supplies furnished, except any payment of tax or inverse duty structure. A Goods & Services Tax liability via the cash is paid by the assessee of 1 Percent of the output tax liability that is steadily being added to the tax period in the current FY. The Assessee is a Govt. Dept, a PSU, Municipal authority/statutory authority.