WHAT IS FINANCIAL LITERACY & FINANCIAL FREEDOM ?

financial literacy, financial freedom, effects of financial illiteracy, invest your money for the long term, rule of 50/30/20, do we need to diversify our savings?

Read MoreWhile riding on a high-speed train through India, Europe, or Taiwan, a passenger may see massive wind turbines scattered throughout the countryside. Marveled by the landscape, the passenger may take a snapshot on her phone camera and send it to her family. Without realizing it, the passenger is likely to have benefitted from infrastructure projects that have been financed by a mechanism called “project finance.” The high-speed rail, the wind turbine, and the telecommunication towers are all large and complex infrastructure undertakings. Sometimes such projects are made possible by traditional financial methods; increasingly, however, infrastructure projects are financed by a mechanism that engages a multitude of participants including multilateral organizations, governments, regional banks, and private entities. In project finance, participants negotiate amongst themselves to spread risks associated with an undertaking, thereby increasing the chances for success in developing vital infrastructure projects for that country and its population.

Project finance is the preferred financing mechanism for large infrastructure projects that are essential for developing countries, emerging economies, and developed countries alike. This FAQ will define project finance and compare it to corporate finance, present project finance participants, and discuss the financing mechanism. It will also address the advantages and risks associated with project finance and provide insight into the future of project finance.

At its core, project finance is a method of financing where the lender accepts future revenues from a project as a guarantee on a loan. In contrast, traditional method of financing is where the borrower promises to transfer to the lender a physical or economic entity (collateral) in the case of default. In practice, most projects are financed by a combination of both traditional methods as well as by guarantee-backed loans. While the name suggests that project finance refers to raising capital by any means to pay for any project, the term refers to a narrow but increasingly more prevalent method of financing capital- and risk-intensive projects across a broad array of industries.

The twentieth century was marked by a reliance on the public sector for developing infrastructure projects. Historically, governments initiated infrastructure projects to develop or build essential facilities so that citizens and businesses could conduct various operations and experience economic growth. In the last two decades, however, there has been a shift in the model of development from the public sector to greater private sector participation. These hybrid public-private partnerships (“PPP”) have been instrumental in upgrading existing facilities and creating new infrastructure in various industries and in all parts of the world. The most common method of financing PPPs is “project finance.”

Source: Thomson Routers

Today, various sectors employ project finance, including power, transportation, oil and gas, leisure and property, telecommunications, petrochemicals, mining, industry, water and sewerage, waste and recycling, and agriculture and forestry. The chart above suggests that while project finance is most common in power and transportation projects, it extends to a broad range of industries. Project finance is an important tool for financing projects in developing and emerging economies, yet developed countries employ the mechanisms as actively as less developed countries. For example, in 2010 India had the most active project-finance market with over $52 billion worth of deals, stemming from 131 loans. Spain came in second with 67 loans (for a total of $174 billion) and Australia in third with 32 loans (worth $14.6 billion).

In traditional or corporate financing, the sponsoring company (the company building the project) typically procures capital by demonstrating to lenders that it has sufficient assets on its balance sheets. That is, in the case of default, the lender will be able to foreclose on the sponsor company’s assets, sell them, and use the proceeds to recover its investment. In project finance, the repayment of debt is not based on the assets reflected on the sponsoring company’s balance sheet, but on the revenues that the project will generate once it is completed.

The sponsoring company must consider several factors when determining whether to use a corporate or project finance structure. Such considerations include the amount of capital needed, the risks involved (political risks, currency risks, access to materials, environmental risks, etc.) and the identity of the participants (whether a government, multilateral institution, regional bank, bilateral institution, etc. will be involved). As the graph below demonstrates, corporate finance most often involves private investors who provide financing in return for ownership (equity) in a project company. The focus in project finance, however, is mostly on loans to the project company, with project revenues as the source of the return on the investment to lenders.

Project finance greatly minimizes risk to the sponsoring company, as compared to traditional corporate finance, because the lender relies only on the project revenue to repay the loan and cannot pursue the sponsoring company’s assets in the case of a default. However, a sponsoring company can only use project finance where it can demonstrate that revenue streams from the completed project will be sufficient to repay the loan. In fact, lenders will often require that the sponsoring company demonstrate that it has agreements in place that will generate the required revenue (called “off-take agreements”). For example, in the case of power projects, the sponsoring company often signs contracts with distributors where the distributors agree to purchase electricity generated by the project. Therefore, project finance is most suitable for a project where there is a predictable revenue stream to support debt repayment.

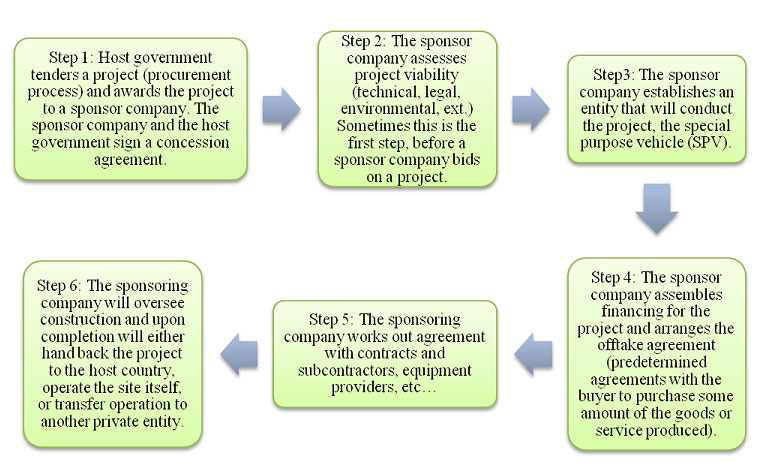

Project finance has many participants who participate at different stages of a project’s development and operation. Because of the complex structure of project finance, not all projects follow the same structure and not all of the participants described below partake in all projects. Since the goal of project finance is to build large infrastructure projects by allocating risks to the party most able to bear it, the following participants are usually involved in a project financed under a project finance model: the sponsor company, the special purpose vehicle, the host government, financial institutions (multilateral, regional development banks, bilateral, and commercial banks), contractors and builders, and infrastructure operators and off-take purchasers.

The Development Company: Every project must have a core entity responsible for organizing, developing, and ensuring that the project is operational. In project finance that entity is called the Special Purpose Vehicle (SPV). A Sponsor Company creates an SPV for the sole purpose of achieving the limited goals of construction and operation of a particular project.

(a) Sponsor Company. The Project Sponsor can be a company, a group of companies, a joint venture, or a subsidiary of another company that initiates a project. A project sponsor can become involved in a project in one of two ways: (1) when the host government solicits bids (goes through a procurement process) and selects the best candidate among the bidders; or (2) a company or group of companies may initiate a project on their own, with or without soliciting host government involvement. However, most projects have government involvement and backing.

A project sponsor has a limited but important role; it is the company or group of companies that either solicits bids or receives tender from a host government to construct a site. The project sponsor then creates a special purpose vehicle that will conduct all the business associated with the project on behalf of the project sponsor. At the project’s completion, the sponsoring company will receive the profits generated by the project.

While the project sponsor is the main equity owner of the SPV, the project sponsor does not carry liability in the case of default because, as mentioned earlier, future revenues of the project are the guarantee. Therefore, the project sponsor has ownership of a project without some of the risks that it would face in traditional finance. In return for a significant (and often majority) equity ownership stake in the SPV, the project sponsor invests a limited amount of its own money to win the procurement bid as well as to pay for early administrative costs.

(b) The Special Purpose Vehicle. A project sponsor creates a SPV for the purpose of constructing the project. There are various ownership structures for an SPV, which are linked to the type of financing that the SPV is likely to procure as well as the law of the host country. Most importantly, an SPV is the legal entity that contracts with other parties involved in the development process.

For example, in the United Arab Emirate’s Umm Al Nar Desalination Plan, the Sponsor Companies were a joint venture between a company that is wholly owned by Abu Dhabi Water and Electricity Authority (ADWEA), Tokyo Electric Power Company (TEPCO) and Mitsui. The joint venture created the Arabian Power Company (APC), which is the SPV. To ensure the success of the project, the joint venture companies provided the initial capital necessary to jump-start the project to the SPV. The investment was proportional to their share of ownership of the SPV, totaling 112 million British Pounds of the $2.1 billion dollar project.

The Host Government: Large infrastructure projects often require government involvement. As addressed above in the discussion on the role of the project sponsor, the government may decide to build a project, for example, a desalination plant or a power station, but will often lack the economic resources to construct the site. Moreover, a government may not want to assume construction risks or face political risks if the project does not have strong political support. In order to mitigate construction risks and to draw together the necessary capital, a government may procure a sponsor company to build the project on behalf of the government. In the above Umm Al Nar Desalination Plant example, Abu Dhabi Water and Electricity Authority is a government entity that solicited Tokyo Electric Power Company (TEPCO) and Mitsui, two private companies, to form a joint venture in order to secure all the additional funding.

It is also common for the government to be a guarantor, but not to have an equity stake in the SPV. The host government can be a guarantor by providing risk mitigation in the form of sovereign guarantees which includes repayment of debt in the case of political unrest, promises to make favorable legal reforms, setting favorable tariffs, and promises to pay back private debt in the case of default, among others. A common sovereign guarantee is when the government agrees to purchase all or part of the output of the product, sometimes at a set price. For example, in the Umm Al Nar Desalination project, Arabian Power Company, the SPV, signed a purchase agreement with Abu Dhabi Water and Electricity Authority whereby the latter agreed to purchase all the desalinated water produced by the site for a 23-year period. While this is a common off-take arrangement, given that many projects generate public consumer goods, the guarantee can expose the host government to substantial liability. In the case of the Pigbilao Project in India, for example, the government guaranteed to purchase all energy produced by the site. However, demand dropped during the Asian Financial Crisis and the government could not afford to continue to purchase all energy generated by the plant.

Financial Institutions: There are numerous financial institutions that may be involved in building a site financed by project finance. Furthermore, there is an even greater variety of capital support structures that a financial organization can provide for a project. Most projects engage some combination of multilateral organizations (for example, the International Finance Corporation), regional development banks (for example, the Islamic Development Bank), bilateral organizations (for example, the U.S. Ex-Im Bank), and commercial bank financial assistance. The form of support is as varied as the parties: low interest-rate loans, no interest-rate loans, market interest-rate loans, guarantees, political insurance (insurance against changes in authority or legislation), equity ownership, and technical and operational support. Generally, the role of financial institutions is three-fold. First, financial institutions provide loans with varying levels of interest rates depending on the economic situation in the host country and its creditworthiness. Second, some financial institutions, such as the World Bank or the European Bank for Reconstruction and Development, provide guarantees and political risk insurance, thereby providing assurance to other investors. Finally, financial intuitions may help provide guidance on how to manage the project or provide technical expertise.

To better understand the complexity and the ways in which financiers interact with each other, consider the following example. The CBK Power is a hydropower station in the Philippines that involved participation by multilateral organizations (“Senior Lenders” in the chart below) and a bilateral investment organization, the Japan Bank for International Cooperation (JBIC), to finance and guarantee the loan. Note that JBIC did not lend directly to the SPV (“Project Company” in the chart) but to the company who wanted to purchase equity from the original sponsor company, in this case to J-Power and Sumitomo Corporation. This demonstrates just one variation by which a sponsor company and the SPV can finance a project through project finance depending on the demands of a project. Because this project involved the continuation of an existing project with a shift in ownership, private financial institutions financed the equity acquisition. To enable the transaction, JBIC provided guarantees to private financial institutions in case the sponsoring companies default on their loan to purchase ownership of the SPV. In this case, JBIC is not a lender to the SPV, but a guarantor on a loan to purchase ownership of the SPV. JBIC and the private financial institutions are mezzanine lenders, and in the case of a default, they are paid back after senior lenders. Therefore, JBIC provided both financing and political risk coverage to the new sponsor companies, and repayment, as the chart below demonstrates, is limited to tariffs generated by the project.

Similar to the traditional finance model, a project finance model allows an entity to use equity or debt financing. Most entities in search of investment funds prefer debt financing to equity financing because they retain full control over the project and earn a greater return through the use of debt financing. Debt financing refers to funding a project with a loan, where the SPV takes out a loan and no other investors are involved. In contrast, equity financing requires the project sponsors of the SPV to either contribute cash needed for the project or sell ownership in the SPV to raise capital. In addition to maintaining full control, debt financing is attractive because project sponsors do not have to contribute extra capital to the project.

Equity: Often host governments and debt lenders will require that the entity building the project obtain some equity funding in order to demonstrate project viability in the market and to offset initial costs. There are a number of factors that influence the level of equity in the SPV that will be made available by the sponsoring companies via equity funding and how much of the construction costs the SPV will solicit in the form of loans. Those factors include how the project is organized, who the players are, what the particular risks are in that country, and what legal requirements there may be in the host country. Typically, equity comprises a smaller share compared to debt (although equity-to-debt ratios range from 5% to 50% in project finance).

Debt: There are two main types of debt: Mezzanine and Senior Debt.

(a) Mezzanine Debt: Mezzanine Debt is a special type of debt, which has priority over equity, but is subordinate to other types of loans. Recall the example above of the CBK hydropower station. The mezzanine debt lenders were providing capital in order for one project sponsoring company to purchase the existing project company. If the project fails, senior lenders who were lending to the SPV rather than to the new sponsor company will be paid off first. The important fact to bear in mind is that mezzanine debt refers to debt that is riskier, because there are other outstanding loans that have priority over the mezzanine loan in the case of a default.

(b) Senior Debt: As the name suggests, senior debt has seniority in the event of default. A lender may stipulate that it is a senior debt lender, as the World Bank does for example. This means that in the case of default, that lender will receive payment before other creditors of the project. There are several types of debt available to sponsoring companies:

Leasing: One other unique method of financing is lease financing where the SPV rents equipment relying on future revenue stream of the project to pay the lease. That is, the SPV does not make immediate payments on the leased equipment, but promises to pay for the equipment once the project begins to generate revenue. Because construction costs are significant, this sort of financing can play an important role in enabling a project to proceed. The company leasing the equipment has a security interest in the equipment and can repossess the equipment in the case of a default. In return for the financing, the SPV may be required to pay additional interest or pay a premium on the cost of renting the equipment.

One of the reasons that participants employ the project finance model as opposed to traditional finance is because infrastructure projects require large volumes of capital. With so many participants, risk can be allocated among the parties best able to bear it. Because project finance is a common financing mechanism for long-term, labor-intensive projects, risks are abundant and may surface at any one of the many stages in the project cycle. This next section will discuss the main risks inherent in project finance and how the various parties, in their agreements with each other, attempt to mitigate them.

Commercial Risks: In the larger scheme of commercial risks, there are two main types of financial risks: interest rate risk and currency risk. Like in traditional finance, changes to the interest rate may negatively affect the financier or the SPV, or both. Most projects are long-term so lenders charge floating rates (as opposed to predetermined, set rates) based on market conditions. Therefore, when interest rates rise, the costs of the project will increase and the SPV may find itself unable to meet its financial obligations. In order to mitigate this problem, when possible, it is best for the SPV to negotiate a either a fixed interest rate or a floating interest rate, but one that floats only within a fixed manageable range. Alternatively, the SPV may use interest-rate swaps to mitigate the risk that a floating rate will increase. The SPV may swap with another party, like a private bank, the floating interest rate for a fixed interest rate on the principal amount the SPV borrowed.

Currency risk is also a serious financial risk to project finance, and one that is not easily mitigated. Currency risk occurs when revenues are generated in one currency while debts must be repaid in a different currency. This is called currency mismatch. In project finance, financing is typically received in the currency in which the lender operates and the lender expects to receive payment in the same currency—e.g., a U.S. bank lends in dollars and expects to be repaid in dollars. However, because currency exchange rates fluctuate, an SPV may find itself unable to pay its lenders if the domestic currency suddenly and significantly drops in value. For example, fluctuations in exchange rates may make repayment difficult if an SPV generates revenue in the Thai baht, but must pay back in dollars. If the baht drops in value with respect to the dollar, then the SPV will need to come up with more baht to pay back the loan because one baht now pays back less debt then before the devaluation.

During the Asian Financial Crisis, many Asian countries’ currencies suffered significant depreciation; Indonesia’s Java Bali Power Grid project demonstrates the extreme effect of currency mismatch. The off-take purchaser (power purchaser in this case) bore the currency risk under the purchase agreement, and when the Indonesian rupiah fell 87% in 1996, the power purchaser’s rates to customers skyrocketed because of its obligations to pay for the debt in dollars. As a result, the power purchaser had to pay approximately 400% of the original price. Similar to interest rate swamps, the SPV may mitigate risks stemming from currency exchange-rate fluctuations by utilizing a currency swap, allowing the SPV to convert debt into a more stable currency. Also, a real exchange-rate liquidity (REX) facility may be used, which addresses the risk of a devaluation of the local currency. In the event of a specified devaluation, resulting in a cash flow shortfall, the facility provides liquidity to cover the debt payments.

Closely related to the currency mismatch are demand risks. Essentially, either through poor planning or because of some extraneous event like the Asian Financial Crisis, demand for the project-finance generated goods or service may drop, in which case the essential element of project finance—the revenue stream to pay back loans—is reduced. A drop in demand was the reason the Pigbilao Project failed in the Philippines. The project was well financed and completed on time, but when the Asian crisis hit in the 1990’s, demand for energy fell significantly. Napocor, the Philippines National Power Company, was the off-take purchaser and bore the demand risk. When demand fell and prices rose, Napocor feared political backlash and had to subsidize the price of energy. The best method to mitigate demand risks is for the parties to do extensive pre-construction forecasting of future demand. Additionally, the party bearing the demand risk may seek a guarantee from a third party like the World Bank, as detailed below.

Political Risks: Political risks take various forms, which include changes in a government’s authority, legislation, and budget. Sponsoring companies often overlook the possibility of a change of authority, yet a regime change or a change in power of a ruling party can influence the success of both the construction and operation of a project. Given the close relationship of the SPV and the host country in project finance, even the possibility of a change can be disruptive to the progress of a site. Government corruption can also seriously hinder a project.

A change in the political authority, either of a political system (like a change from autocracy to democracy) or a change of from one political party to another within a political system, may lead to changes in the host country’s position on a vital element of an agreement. Take for instance the Dabhol power project in India. The sponsoring companies negotiated a rushed agreement with the Indian government, which was anxious to have foreign investment in the region, forming the Dabhol Power Company (DPC). In 1995, Dabhol became a major campaign issue in the Maharashtra state election. The Congress Party lost control to a coalition party formed by Bharatiya Janata Party (BJP) and the ShivSena. The two parties won on a platform that advocated hostility to the sponsoring companies of the Dabhol Power Company. Once in power, the new government created the Munde Committee, which reviewed the Dabhol power project and determined that the Indian government rushed into an agreement with DPC, and that the agreement was too one-sided. As a result, the government ordered DPC to stop construction. After lengthy negotiations, the agreement with India was renegotiated. While the project did not ultimately fail because of the political change (it failed because of miscalculation for demand), the Dabhol power project demonstrates the extent to which a change in power can bring a project to a standstill.

Political risks are mitigated by political risk insurance. Private companies as well as multinational organizations (like MIGA, which has a special political insurance service) provide insurance in a traditional sense, in addition to issuing performance bonds that guarantee completion.

Legal Risks: Changes to the laws governing elements of agreement, status, or operations of the project can significantly affect the costs of an operation. Specifically, changes in import and export tariffs can increase costs by preventing access to cheap raw materials or by forcing the SPV to use inferior domestic inputs. A host government may want to achieve certain short-term economic or social goals by changing the tax code, which can purposefully or inadvertently affect the project structure. The rate at which host country taxes the SPV or other parties will significantly affect the financial benefits to participants. Finally, the host country can adopt laws that change the legal status of the SPV, or change the laws governing ownership of companies or real estate, which can have a catastrophic effect on the project. Legal risks are most often mitigated by guarantees (which are elaborated upon below) from one of the participants—most commonly the host government.

Construction, Operation, and Technical Risks: Construction, operation and technical risks are usually assessed during the first stages of the project in a “feasibility study” that carefully examines risks associated with putting up the project as well as the technical and environmental regulations that may impact the project. The main construction risk is that construction will be stopped or significantly delayed. Sometime construction is delayed because builders do not have access to materials, but it may also be intertwined with other risks, such a political risk that may halt construction.

In a power project, for example, the construction risk may be that the builders will have delay or problems having equipment shipped to the site. A technical risk may be access to a power grid for the distribution of power to customers. Because storing power can be very challenging, immediate access in proportion to demand is essential for a successful power project. A thorough feasibility study should examine construction risks as well as how power will be interconnected to the main power grid, technology compatibility issues, and how revenue will be calculated. In order to mitigate some of the risks, parties can draft legal agreements that specify the terms under which the SPV has access to the grid, and how the power generation site will connect to the grid. To mitigate construction risks, the SPV can negotiate for the builder rather than the SPV to bear that risk. Such agreements are instrumental for the success of a project, since access to the power grid is an essential component of generating revenue to repay loans. Another risk is that the host country could change technical requirements before the project is complete. For example, the laws on environmental protection may change or the national legislature may pass a new law that requires a higher density of steel for structures of a certain height, affecting the project’s compliance with building regulations.

A feasibility study evaluates environmental regulations and the effect of building a site at a particular location. In order to comply with national and international environmental laws, companies often conduct extensive environmental impact analyses. If an international or national environmental agency detects non-compliance, a project may be shut down, fined, or may face social and political backlash.

Mitigating Risk with Guarantees: As referenced above, one important method of mitigating commercial, political, legal and construction risks is for the SPV (the most common recipient) to acquire guarantees by the parties best able to bear the associated risk. Most commonly, large multilateral organizations like the World Bank, and regional development banks, like the Asian Development Bank, provide guarantees for worthy projects. However, any one of the participants can provide a guarantee on any one of the associated risks.

Guarantees are credit enhancement devices. For example, during the early stages of construction, the sponsor company may be the guarantor. Contractors usually guarantee project completion either by performance bonds or payment bonds (guarantees that subcontractors will be paid). Often, multilateral and bilateral organizations mitigate financial and political risks by issuing guarantees. In turn, the guarantors may purchase insurance in case they have to provide capital for a default under the guarantee agreement. Depending on the organization of the projects, the roles of other participants, and the nature of the agreement with the sponsor company or SPV, guarantees can take various forms. Typically, third-party guarantors like a multilateral organization or a regional bank do not sign unconditional guarantees, but rather limited or indirect guarantees. Often, these guarantees are in the form of “put options,” where the guarantor promises to pay for any liability of the obligor (the project company), but the project company must pay back the guarantor.

Without guarantees, some projects may never start. For example, in 2006, the International Development Bank (IDB), Multilateral Investment Guarantee Agency (MIGA), and Steadfast Insurance Company (SIC), a subsidiary of Zurich Financial Services Group, (that is in turn is insured by Oversees Private Insurance Corporation), contributed $250 million of guarantees to a $510 million gas pipeline that stretches 678 km approximately 15 miles off the coast of Nigeria to Ghana. Along the way, smaller pipelines that lead to intake locations in Benin and Togo connect to the pipeline.

As one of the largest private investments in West Africa, the West African Gas Pipeline (WAGP) could not have been possible without the guarantees by multilateral and bilateral organizations. Nigeria, Ghana, Benin and Togo are developing countries, so private investors entering the region face significant political risks. By providing complementary guarantees (there was no interest rate attached to the guarantee) to the government of Ghana, the International Development Association (IDA) guaranteed that if the Government of Ghana was unable to make payments on the gas under the off-take agreement, the IDA would satisfy the SPV’s debt repayment obligations to its financiers.

Project finance allows countries to build the infrastructure necessary to increase growth and development. It draws a greater volume of financing than under traditional schemes because risks are often spread among the various participants, and development organizations mitigate risks by providing political and commercial guarantees. Without project finance, many essential and life-enhancing projects may have never been constructed.

As a relatively new method of financing dating back to the 1970’s, project finance offers several important advantages as a financing mechanism. It is a non-recourse financing mechanism, meaning that in the case of default by the sponsor company, a borrower’s liability to the lender is limited to the assets of the special purpose vehicle rather than the company or companies that own the SPV. Therefore, the companies that own the project site do not have to fear that lenders will be able to go after the assets of the sponsor company if there is a default.

Large infrastructure projects are essential for developing and emerging economies. Therefore, multinational and regional organization, like the World Bank or the African Development Bank, whose goals are often poverty prevention and developing economic prosperity, are more willing to provide financing. Moreover, the financing is likely to be at a discounted interest rate. The guarantees provided by such organizations serve to attract more investors. A massive hydropower generation site, for example, is a very expensive endeavor. Despite the lucrative gain, many private companies shy away from such capital-intensive endeavors if there is no safety net, and governments are also unable to make the necessary funding available, given other demands on a nation’s resources. Given the participants and its organizational structure, project finance provides a safety net to private investors, enables host governments to attract investment, and develops needed infrastructure projects without exhausting host country reserves. Moreover, depending on the financing arrangement, host governments maintain control over the site if necessary.

Given that power projects require high amounts of capital, and because of the way projects are organized both financially and legally, the debt of the SPV is not reflected on the sponsor company’s balance sheet. This is called “off-balance sheet” accounting, where all debts are assigned to the SPV rather than the sponsoring company and the sponsoring company does not have to account for the large debt in its accounting books. This allows the sponsoring company’s credit rating to remain unaffected.

Other advantages of the project finance structure include debt leveraging, favorable financing terms, and access to capital. Debt leveraging refers to financing by debt (as explained above) as opposed to equity. This is an important advantage for the sponsor company because it does not have to reduce its ownership of the SPV, and therefore can keep more of the profits once they are generated. Because project finance typically involves guarantees, particularly by multilateral and regional banks like the African Development Bank or the Asian Development bank, the SPV often attracts more investors and receives lower interest rates because the risk of default is reduced. Project finance provides access to more capital than would be available to a private company or government on their own because governments would typically be limited to their internal financing and private companies usually cannot attract enough capital necessary for large infrastructure projects without additional guarantees.

Project finance is an increasingly widespread financial mechanism, which host governments and private investors are employing more frequently and in greater volumes as a method of financing infrastructure projects. While the most recent economic crisis has had a significant impact on the volume of capital available, project finance remains a valuable financing approach that offers significant advantages to participants. Furthermore, it is likely to continue to grow as the global economy recovers. The graphs below shows the growth trends for project finance. In the six years prior to 2009, there was a relatively steady increase in the volume of capital financed under the project finance model. While not all areas of the world experienced the same growth in volumes of capital, with Asia Pacific and Europe, Middle East and Africa (EMEA) benefiting most, total volumes nearly tripled from 2003 to 2008.

Source: Thomson Reuters

The graph suggests that capital in project finance will continue to increase, given the speed with which the volume of capital is returning to pre-recession levels. In 2006, at the high point of global economic stability, there were 541 project-financed projects for a total of $180 billion. In 2010, while still in the process of economic recovery, there were 587 project funded by $206 billion, despite the tightening of capital markets during that time.

There are several possible explanations for the continued growth and success of the project finance model. First, developing and emerging economiesare making significant strides to develop their economy, which often requires building infrastructure to effectively utilize available natural resources for domestic growth. For example, before the expansion of the West Africa Power Project, West-African nations were unable to take advantage of inexpensive regional reserves of natural gas. Second, technological improvements are reducing the risks associated with various projects that are best financed through the project finance model. For example, solar energy technology is becoming increasingly feasible and economically viable, so investors and developers are less wary to build such projects. Third, parties involved in project finance have over the last forty years developed the project finance mechanism in way that best mitigates risks, thereby insuring a greater likelihood of success. Fourth, many governments are privatizing certain industries, especially when existing infrastructure needs repair or refurbishing. In those cases, governments are likely to turn to the project finance model in order to maintain involvement and control while reducing capital contributions. Finally, commentators believe that project finance drives economic development in low-income countries. In many low-income countries like the ones in the West Africa Power Project, the projects and the positive subsequent effects on regional and national economic developments would not have been possible without project finance.

The area that seems to be growing most rapidly is power project financing for both power generation and transmission. There are several reasons that power projects dominate project finance. The primary reason is that governments are looking to build infrastructure that does not rely on oil. Additionally, many countries have other natural resources that can be converted into energy, and power project finance allows nations to build new massive infrastructures cost-effectively. For these reasons, power projects financed by project finance are not limited to developing and emerging economies, but have a presence in developed countries, particularly solar and turbine power generation in the United States and northern Europe. Power is just one industry where project finance is likely to have a growing impact in the future. As developing and emerging economies work to create the necessary infrastructure to improve the lives of their citizens, project finance will ensure future global growth and development.

Rajput Jain & Associates is a trusted name among the prime Project Finance Services providers. We raise finance and capital for existing and upcoming new business entities, who want to expand their field of operations. We offer different kinds of projects which include Funds for Trade finance, Long and Short Term Funds, Foreign Currency Loans and many others. Backed by huge clientele and clean track record in the field of Corporate Financing our firm is most reliable firm in the market.

We have tied up with some of the renowned Business Loan providers of India, offering loans at the most competitive interest rates. So, stop moving door to door in search of the cheapest business loans, you need to just contact us.

200+

550+

2009

700+

financial literacy, financial freedom, effects of financial illiteracy, invest your money for the long term, rule of 50/30/20, do we need to diversify our savings?

Read More

Top 10 Financial Services Companies in India, Ten kind of Financial Services, Best 10 Financial Services Companies in India, top Ten financial services companies in India, Top ...

Read More

Why we Should invest in NPS just for the tax benefits?, National Pension Scheme, compare National Pension Scheme & Public Provident Fund investments

Read MoreWe are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

All the information related to any client is considered confidential and never be disclosed to anyone.

Having years of experience in respective areas and backed by skilled and experienced workforce keep us ahead.

We believe in the building the good relationship with the clients that ensures the great impression.

If you are not happy with our services then you can request a refund within 30 days.

We provide 24*7 supports through phone, email and live chat.

You can pay online through EMIs, PayPal, net banking, debit card, credit card and more.

We are the exclusive member in India of the Association of International Tax Consultants, an association of independent professional firms represented throughout Europe, US, Canada, South Africa, Australia and Asia.

© 2016 Rajput Jain & Associates. All Rights Reserved | Sitemap